The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Exxaro Tiles IPO-Incorporated in 2008, Exxaro Tiles is engaged in the manufacturing marketing activities of vitrified tiles.,

Business — The company manufactures Double Charge Vitrified Tiles (double layer pigment) and Glazed Vitrified Tiles made from ceramic materials i.e. clay, quartz, and feldspar. Its product portfolio consists of 1000+ different designs of tiles in 6 sizes. Topaz Series, Galaxy Series, and High Gloss Series are some of the well-established products of the company. It supplies its products to large infrastructure projects i.e. residential, educational, commercial, hotels, hospitals, government, builders or developers, religious institutions, etc.

Region of operation — Major cities in India and It also exports tiles to different countries across the globe i.e. Poland, Bosnia, USA, and others.

Offer purpose — The IPO is issuance of shares worth ₹161 crore for debt clearance and general corporate purposes.

Risks —

The tiles segment is highly competitive with established listed names in the market as well as a huge unorganized segment that is active in manufacturing tiles. The company provided security regarding loans from banks by creating a charge over its movable and immovable properties. The total outstanding amount payable by the company stands at Rs 142 crore as of FY21. It carries high trade receivables on its balance sheet, accounting for 94 per cent of its current assets and 24 per cent of its total assets. As the company plans to expand, this can increase the quantum of trade receivables and inventories

Strength

Variety of vitrified tiles design choices in different sizes.

Large dealer network with 2,000+ registered dealers.

Strong PAN India presence in 27 states of India.

International presence with export to 13+ countries across the globe.

One of the largest manufacturing plants of glazed vitrified tiles in India.

Future

Earnings have been growing well and with real estate boom talk, it may turn out to be good story. Overall company and its products don’t have any moat

Valuations

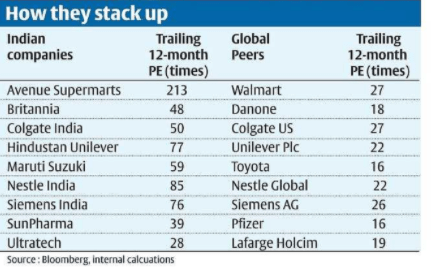

Valuations do look fully priced at the current earnings levels of FY21, the earnings have been growing also well.

Should we apply?

People can subscribe only for listing gains.

If holding, need to patient for medium to longer term

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.