Prince Pipes and Fitting makes polymer pipes and fittings in India that are used in plumbing, irrigation and soil, waste and rainwater (SWR) management

It has 7,200 stock keeping units (SKUs) and 1,500+ channel partners.

Company has strong cash flow from operations and business share in Q4FY21 has been 69% from construction

Company current strategy is to expand in south india and increase distribution network while keeping the margins(EBITDA,OPM), ROCE in similar range

Company has been able to make use of 3 drivers of margin expansion in FY21 : inventory gains, product mix change, superior pricing power: past 8 Quarters company has been aggressive in passing on price .

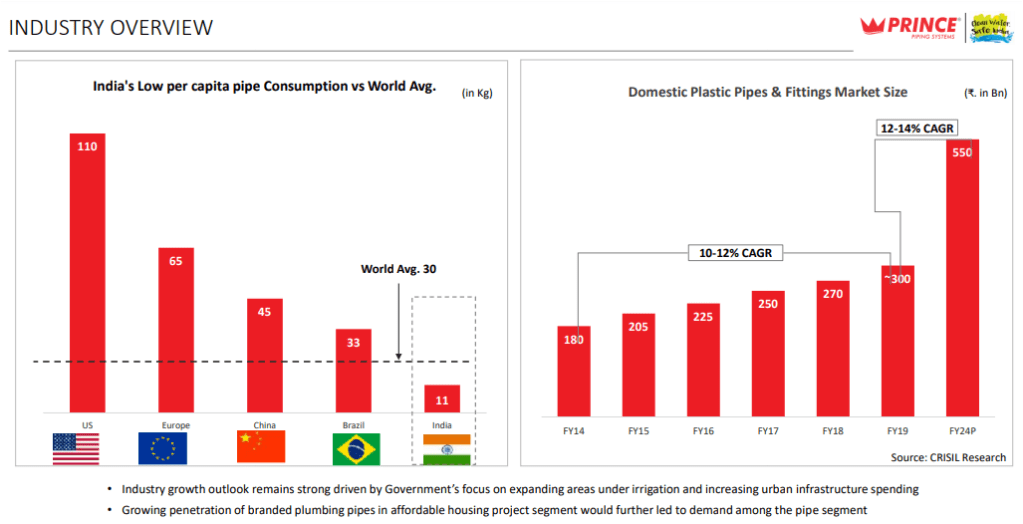

Growth triggers

Total installed capacity of approximately 259,000 tonnes per annum (TPA). This will increase by a further 51,000TPA once its Telangana plant is fully commissioned- that means almost 20% increase in capacity

Various Government initiatives like AMRUT scheme, which is aimed at providing basic services, such as WSS, and ensuring that every household has access to assured tap water supply and a sewerage connection. Jal Jeevan mission (Urban) focuses on providing water supply to 4,378 urban local bodies with 260 million household tap connections. Nal se Jal scheme is planned to offer piped water to every rural household by 2024 –all these schemes is helping industry to grow by 35%(estimated) in next 2-3 years

There is a visible structural shift from unorganized to organised players and Prince pipes has shown both volume and sales growth wile other major players have shown de-growth in FY21

PPF is gradually increasing its emphasis on high-margin business of CPVC and double-wall corrugated pipes (DWC).

Recent tie up with Lubrizol will help the company in getting its supplies secure and as well as will attract more distributors towards company

Expansion into South India with Telangana Plant and focus on east india in coming years may keep the growth rate intact

Data-driven pull against conventional push is the new sales strategy of the company for the retail segment. Business-to-business (B2B) remains an area of improvement where PPF sees ocean of opportunities. It has moved into technology driven plumber data to move into B2B business as well as for normal business

Risks

Raw Materials Prices: Raw materials (resin) are derived from crude oil and any increase in crude oil price can hurt margins in short term.

COVID Lock-downs: Second wave of COVID, many states have had to announce lock-downs, although this time plants were not completely shut but still first quarter at least, could be dampner.

Corporate Governance Issues: There have been allegations of inadequate disclosure in the IPO prospectus of PPF PPF did not disclose all litigations, claims and criminal proceedings against the promoters (although re-filed DHRP corrected anamolies but still some differences are claimed)

No moats and No barriers to entry in this business

Fake / duplicate products can hurt company business

Exit Strategy

COVID-19 third wave creating more havoc than 2nd wave can impact the company balance sheet in big way for construction and this should be on radar

Break up with Lubrizol will definitely hurt the company and we need to relook if such thing happens in future

Any negative change in Govt policy for water schemes can hurt the growth prospects and may warrant an exit

Discover more from ALPHA AFFAIRS

Subscribe to get the latest posts sent to your email.