BE FINANCIALLY INDEPENDENT

Read more here on Route Mobile

Read more here on Burger King

Read more here on boAT

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Among Top 5 car makers, Kia Motors and Tata motors gain market share and other have lost. After quite some time, Maruti’s Market share dropped below 50% mark

Retail investors often take their investment decisions based on the share price instead of the fundamentals. They tend to buy what looks ‘cheap’ and get influenced by the news around a company. They often see a large fall in share price as an opportunity. However, such investments often end up becoming value traps. A huge price decline may not always be due to a temporary issue but also due to a permanent dent in the company’s prospects. Also, a sudden surge in the stock price attracts retail investors. They then invest in such a company, without paying much attention to its fundamentals. Curiously, the lower the ticket size of the share, the more interested retail investors become. All these are wrong reasons to buy a stock. A stock should be bought because the fundamentals of the underlying company are robust. Tracking the activity of promoters, FIIs and DIIs can be a useful input in determining this.

-source Valueresearchonline

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Bector Food Specialities IPO– Mrs. Bector’s Food is one of the leading companies in the premium and mid-premium biscuits segment and the premium bakery segment. Company is largest supplier of buns for QSR restaurants in India.

Business — Sells Biscuits, Bakery products, Frozen Products. And a contract Manufacturer for Oreo and Bournvita biscuits

Offer purpose — Offer for sale (540cr) including fresh issue of 40 cr. for expansion and general purposes

Key Service domains – Biscuits domestic 43% of total sales, 24% exports of total sales.

Key export regions are Africa and North America. Total 64 countries where export is done

Risks —

There are cases of non-compliance against certain legislations in the past by group company and some disciplinary actions as well

Highly competitive industry with company having only 1% market share. Margins can reman depressed for quite long time putting strain on cash flows

Low shelf life of certain products

Company do not have any long term supply agreements with any of their QSR customers is a strange thing and deals on day to day basis requirement for bns, bakery and frozen products

One of the lowest risk but having high business impact is focus on nutritional value of products which can hamper sales in future

Strength

A leader in biscuits and bakery segments in North India with well-diversified product portfolio.

Major food certifications i.e. BRC, USFDA, and FSSC.

Modern production process, Strong sales and distribution network.

Strategically located in proximity to target markets which minimizes freight and logistics related expense and time

Future

QSR is thriving industry and consumption food business will gain. QSR CAGR expected to grow >20% for next 4-5 yrs

Proxy play to QSR story, so should do well in coming years

Valuations

Profit making company but PAT going down from last three years

Focusing on growth in premium biscuits and bakery segment to improve margin having high competition

As compared to peers, valuations looks ok but needs consistent review

Should we apply?

People can subscribe looking at growth prospects

Listing day may see good gains. Recommended to sell if getting 10-30% gains on listing day

One can also hold long and review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Possible Listing with gain on cards

UTI AMC IPO crisp Summary — Listing with loss as shared

CAMS IPO crisp summary — Listing with 20% gains as shared

Angel Broking IPO crisp summary –Listing with loss as shared

Happiest Minds IPO crisp summary –Listing with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

If you have not read my earlier post , please go through What to do in stock market in early 2020. It’s important as you will be able to relate to this post in much better way after that!

Most of the investors I talk nowadays are not willing to invest in this supposedly overheated Indian stock market and its not about only December 2020, i can see the fear of crash looming in their talk from Sep2020. Most of them have cashed out from market in September 2020 due to Indian Chinese troop clashes and fear of US election results. What happened thereafter is more painful for such investors, Markets ran away further leaving them behind.

Also read : Invest in Stock market IF

We can broadly classify investors in Dec2020 in three kinds

So as you are reading this article, did you notice where do you belong?

Congratulations, if you are able to see yourself amongst one of the three kinds mentioned above

Question still remains same for everyone : What to do now? Should we buy, sell or keep holding? What’s next : Is it bull market or is crash near?

Let’s read further to understand more about it and see what strategies people can adopt

Thsi strategy is for people who

Advantage with these strategy is you may not lose capital if market goes down and may get a chance to re-enter at lower levels. Problem with this strategy is it is impossible for anyone to predict whether market has topped out or not. Will Market go further up and can give you a bigger chance to cash out? Will market come down and give you a chance to enter at lower levels. Nobody knows. Get away from people if they claim to know.

It is always better to leave last 10% on the table and cash out if our goals are near or we have debt to pay because when correction happens, it will not give you a chance to exit at your desired levels

You may need to decide a market point where you should re-enter

I will strongly advised against this. Problem with this strategy is most of us will be invested in 50 + stocks by taking tips from random sources and keeping most of the stocks which are in loss. So if market correction happens, we will not be having enough money to average down all stocks.

In case, you have idle money and have a itch to invest at these levels, in such cases adopt a simple strategy

Correct portfolio allocation and conviction in the chosen stocks is a must for investing at these levels

This strategy is for people

Under this strategy, adopt the simple course of action

What i am doing in this market? My answer is Case 3.

So that effectively means

I am not putting new money into the market

I am selling my existing less convincing or loss making positions

I am adding more of existing convincing positions

I am adding new stocks position partially and waiting for small correction in market to add more

I am re-organizing my portfolio for next cycle of market

I am keeping Cash levels close to 20% to handle market correction and adding more.

I am happy to ride with my 80% invested convincing positions

I would not recommend to sell out and sit if you have not borrowed money and are not facing immediate liquidity issues. But for sure remove dud stocks and put that money into other quality stocks as always

Overall, what I learnt from markets in my journey is very simple and easy to follow :

You can’t be 100% invested in market

You can’t be 100% sold out from market.

Whenever I tried to cash out in fear, I lost major gains in next cycle. Whenever I invested fully 100% in greed, I lost good amount of capital and recovery becomes difficult.

Holding and adding to convincing positions seems simple but definitely a task which is not easy

So is this a bullish market — i dont know and neither i want to know as i am working on stock specific action

Will correction happen–The more we go away from March 2020 lockdowns, greater will be the chances of economic recovery and lesser are the chances of crash. Healthy Market correction (upto 15-20%) can still happen and can give a nice entry point. Not sure of whether it will happen next week, next month or next year or not at all!!

Whatever strategy finally you adopt. don’t be a blind follower

Read more on Blind follower here

Wishing you all the best and lots of luck

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In recent years, there is strong inclination see in investors for investing in US stocks. Of course there is a reasoning behind it. Let’s try to figure out WHY and HOW part of it

To understand this let’s understand the returns by DOW and BSE in last 10 years

US market consistently outperformed Indian market in last 10 years. Although there is no guarantee that it will happen in next 10 yrs again

So outperformance of US markets along with Indian currency depreciation widens this performance gap further and this makes a strong case for investments in foreign stocks

Buying foreign stocks allows investors to

As a thumb rule for starters, a 5% to 10% exposure to foreign stocks for conservative investors, and up to 10-25% for aggressive investors seems ok

Individual investors can invest up to $250,000 every year overseas under the RBI’s Liberalised Remittance Scheme. After opening an overseas brokerage account, investors will be needed to fund it by remitting money from his/her bank account

Now let us understand the 2nd part of it

Open a low-cost international broking account and invest in low-cost international exchange-tradedfunds

Let’s also understand the precaution or risks to be taken care of

When you invest in the US stock market, , please be aware of taxation part

Dividends will be taxed in the US at a flat rate of 25%. Due to Double Taxation Avoidance Agreement (DTAA), taxpayers can offset income tax already paid in the US (Foreign Tax Credit)

Disclaimer : The article is written to provide information and make investors aware of potential avenues of investment. Please don’t treat this as an investment advice. There could be change in tax laws from time to time and one should track it before investing. Past performance of any index returns can not and should not be taken as reference for future performance. Percentage allocation for each investor can vary and its best to consult to one ‘s own financial advisor before making investment decisions. We don’t have any mutual agreement with the sources or apps shared for investment and we dont gain/loss from your action in this regard

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 29th November, 2020

Cycling; Optimism; Electric Vehicles; Investing and Learning

Cycling: Benefits (Cycling weekly)

Optimism: Good things taken too far (CollaborativeFund)

Learning: Bargain Hunter’s Dilemma (Ritholtz)

Electric Vehicles: Big bet but is it enough (Fortuneindia)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Burger King IPO– Company is 2nd largest burger chain in India, started operation in 2014 and fastest international brand to have 200 QSR outlets in Inda

Plan is to target 700 outlets in next 5-6 years.

Offer purpose — Offer for sale (360cr) plus fresh issue of 450 cr. To open new stores and pay some part of loan

Key Service domains – 2nd largest burger chain after McDonald

Risks —

Loss making company as of now. Loss of 119+ cr in six months of current FY21, loss of 76 cr in last year FY20

Offer on food tech apps may harm the business wrt competitors plus McDonald, Jubilant food will definitely try to defend the market share

Fast expansion may lead to more losses in coming years but its a double edged sword and can lead to gains as well

Strength

Post COVID –company will have lean structure and business should have good unit economics

Also because of urban developments and more money in hands to spend, culture of eating in QSR will support the company

Fast expansion can help the company in increasing mkt share

Future

QSR is thriving industry and consumption food business will gain. QSR CAGR expected to grow >20% for next 4-5 yrs

Sustainability looks good, McDonald, Dominos, Subway, KFC have already survived and adapted

Valuations

Loss making company and PE is negative

Last 3 Yr Revenue CAGR at 53.4%; Total Debt as of Sep 2020 at 195 Cr

As compared to peers , valuations are reasonable in terms of mcap/sales or mcap/ebitda

Should we apply?

People can subscribe looking at growth prospects

Listing day may see good gains. Recommended to hold long

If available on listing day around 50-70 Rs, one should add more from 3-5 yrs perspective for possibly good gains

Also Read

UTI AMC IPO crisp Summary — Listing with loss as shared

CAMS IPO crisp summary — Listing with 20% gains as shared

Angel Broking IPO crisp summary –Listing with loss as shared

Happiest Minds IPO crisp summary –Listing with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Look at the sectors showing positive growth as compared to Oct2019

Coal

Electricity

Fertlisisers

Cement

Economy looks on recovery mode like a pendulum which swings in extremes. Although technically India enters into a recession with two quarters of negative growth but optimistically this can change by Mar2021. Only caveat here is fresh set of lockdowns

On the other hand, crude oil, refinery products and natural gas may remain suppressed as world moves to Work form home (medium term trend)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 22nd November, 2020

<p class="has-text-align-justify" value="<amp-fit-text layout="fixed-height" min-font-size="6" max-font-size="72" height="80">Cycling; Flying; Investing and LearningCycling; Flying; Investing and LearningCycling: Cycling shorts (Velocrush)

Investing: How to invest abroad (Morningstar)

Flying: How spicejet is re-learning to fly (Forbes)

Learning: How to take smart notes (Janav)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Covid -19 has an impact on consumer durables to such an extent that demand outsrips supply and many SKU have waiting periods.

Interestingly Dishwashers demand is so high that it outstrips last few years combined sales already. Listed Companies like Whirlpool, Siemens,, Voltas, IFB can be beneficiary and Voltas and IFB stocks have run up in recent past already

This is a trend which will not stop and will have a contagious effect in Indian Society where word of mouth helps a lot in buying decision.

So premium items like dishwashers may become a common sight in coming days in many Indian households. Look for this trend to unfold in medium term

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

FMEG segment already growing –from earlier posts some indicators showing this already

Despite Fall in revenue in other segments in 1st half FY21

Q2 FY21 results fo SBI cards are out and does not look great on few fronts although long term story seems intact as of now

Few snaps from SBI recent investor presentation where we can see the lagging part from company as compared to previous year FY20

SBI Cards : Declining portfolio growth, SBI Cards : Increasing NPA , SBI Cards : Declining PAT

Looks better to wait for right entry price : NOT a RECOMMENDATION

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Equitas Small Finance Bank– Equitas Small Finance Bank is the leader among SFBs in terms of the distribution network (With a network of 991 banking outlets across 17 states and union territories in India). Further, it is the second-largest SFB in India in terms of assets under management (AUM) and total deposits in FY19.

Offer purpose — Fresh issue of 280 cr to boost tier 1 capital plus 237 cr offer for sale

Service domains – The SFB’s product offerings include small business loans, housing loans, agriculture loans, vehicle loans and microfinance loans. On the liability side, it offers current accounts, salary accounts, savings accounts and term deposits to its customers. Besides, Equitas SFB also offers a range of third-party products, including insurance, FASTag for toll plazas and mutual fund products.

Strength –

A well-diversified asset portfolio

Large presence- It is a leader among SFBs in terms of the distribution network.

Risks —

Lower return ratio as compared to peers.

Asset Quality is poorer due to loss in vehicle finance segment. Provision coverage ratio is less

Stock will remain in overhang as promoter stake needs to be diluted to 40% in coming years

Fierce competition and concentration of customers in articular region

Future

Small finance banks are expected to grow 25% annually over next few years and IPO is priced at lower valuation compared to peers factoring lower asset quality and provisioning

Large presence and distribution network will help the bank to grow

Valuations

Seems reasonable

Should we apply?

People can avoid to subscribe

Better peers available in same segment for long term growth prospects

Listing day may see not any gains . Recommended to sell on listing day if any gains available

Also Read

UTI AMC IPO crisp Summary –Listed below IPO price

CAMS IPO crisp summary — Listing with gains

Angel Broking IPO crisp summary –Listing Below

Happiest Minds IPO crisp summary –Listing with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Likhitha Infra– (approx 32 yr old company) is an Oil Gas Pipeline Infrastructure provider in India. Focused on laying pipeline networks, Operation and maintenance of city gas distribution companies in India

Offer purpose — 61 crores to meet working capital requirement

Key Service domains – Cross country pipelines, City gas distributions including CNG stations, Operation and maintenance

Clients -Established players from Oil and Gas industry

Risks —

Major revenue from few clients may deprive the company from pricing power

Inherent risks due to long term nature of projects

Future

CGD is increasing in India and company is at right place for its business to grow with

Strong client base, Efficient business model

Strong project execution capabilities , Diversified geographical presence in India

Valuations

Seems attractive

Should we apply?

People can subscribe for long term growth prospects

Listing day may see gains . Recommended to hold and buy more if listed at IPO price +/-10%

Also Read

CAMS IPO crisp summary — Listing Awaited

Angel Broking IPO crisp summary –Listing Awaited

Happiest Minds IPO crisp summary –Listing with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Mazagon Dock– Defense PSU which supplies warships, submarines and destroyers to Indian Navy and Coast Guard.

Offer purpose — Divestment by Govt. of India

Key Service domains – Warship building, Refit and repairs, Export

Clients -Indian Govt.

Revenues from Key Services–95%+ for building warships, submarines

Risks —

Sole dependence of Ministry of defence budget which is not increasing rapidly in recent years especially for Navy

Weak growth prospects and volatile profits

Long gestation period for the orders and revenue

Future

Company wants to tap repair and export orders but not successful yet with only 2% orders of outstanding book

Dominant Player in warship building industry with huge order book

Refit and repairs constitute 3.5% of revenue and company wants to increase it to 15-20% in coming years

Valuations

Seems reasonable and lower than other listed entities like Garden Reach and cochin shipyard

Should we apply?

People can avoid to subscribe due to weak growth prospects

Listing day may not see any gains . Recommended to book profits if any on listing day

Long term investing only when growth drivers are clear

Also Read

CAMS IPO crisp summary — Listing Awaited

Angel Broking IPO crisp summary –Listing Awaited

Happiest Minds IPO crisp summary –Listing with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

UTI -In top 10 AMC , manages mutual funds, PMS, NPS, AIF and offshore funds

Offer purpose — Offer of sale by existing stakeholders

Key Service domains -Managing domestic mutual funds, PMS, alternate investment funds, retirement unds and offshore funds

Clients -Postal and retiree PMS and NPS services. High concentration in B30 markets segment

Revenues from Key Services–Domestic Mutual funds AUM. PMS and NPS income constitute only 3% although with higher AUM

Risks —

SEBI policy like change in total expense ratio, re-categorization of various schemes, upfront commissions in the past led to lower incomes. Future policy changes can also pose a risk

Large portion (almost 75%) of UTI AMC assets under management in 6-7 active funds, so large scale redemption can be cause of worry

Falling Market share and fall of revenue from operation in last two years is overhang

Financials are on weak foot with ROE mostly 11-13% on an average

Future

Increasing awareness among people about equity investments and growing popularity of Mutual funds can boost revenues

Increasing concentration in B30 Markets segment can boost revenues where they can charge higher TER

Valuations

Optically cheaper valuation as compared to HDFC AMC and NIPPON AMC

Should we apply?

Good chances of allotment.

While valuation, business seems to be in right place but financials are only one thing which leads to– Avoid for IPO subscription

Listing day may see -10% to +10% gains . Recommended to book profits if any on listing day.

Wait and watch policy is best for long term investment in UTI AMC

Also Read

Mazagon Dock IPO crisp summary

CAMS IPO crisp summary –Listing Awaited

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Angel Broking – the fourth largest broking firm in India as per active client accounts on NSE. The company provides its services through online and digital platforms on the back of a network of more than 11,000 sub-brokers as on June 30, 2020.

Offer purpose — 600cr offer for sale + fresh issue. 40% will be used for working capital requirement by company

Key Service domains – provides broking and advisory services, margin funding , loans against shares and financial products distribution to its clients.

Clients -80% from tier 2 and tier 3 cities

Revenues from Key Services–75% from broking. 10% from Margin funding

Risks —

The company’s main revenue source is the broking business, and company has not diversified into wealth management kind of services

Intense competition in broking business

Extensive supervision and regulation by various regulatory bodies that may cause fluctuation in earnings e.g. recently SEBI margin trading rule

Future

Flat fee-based model, a developing derivatives market, the use of modern technology, lower penetration of mutual funds and shares and debentures in household savings and customer acquisition through digital medium enable the company to scale up its business easily.

Digital acquisition of customers will save cost

Valuations

Little on higher side.

Should we apply?

Moderate chances of allotment due to small size.

People can avoid to subscribe

Listing day may see see moderate gains . Recommended to book profits if any on listing day

Also Read

Happiest Minds IPO crisp summary –Listing with substantial gains

Route Mobile IPO crisp Summary — Listing with substantial gains

Rossari biotech IPO detailed summary –Listed with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Chemcon– is a manufacturer of specialized chemicals, such as HMDS (Hexamethyl Disilazane) and CMIC (Chloromethyl Isopropyl Carbonate) and is market leader in both products. This are predominantly used in the pharmaceuticals industry, and inorganic bromides, namely Calcium Bromide, Zinc Bromide and Sodium Bromide, which are used as completion fluids in the oilfields industry

Offer purpose — 318cr Complete offer for sale by promoters

Key Service domains – Pharmaceuticals and oilfields industry

Clients -Hetero Labs Limited, Laurus Labs Limited, Aurobindo Pharma Limited, Sanjay Chemicals (India) Private Limited, and the key customers of Oilwell Completion Chemicals include Shree Radha Overseas, Water Systems Specialty Chemical DMCC, Universal Drilling Fluids and CC Gran Limited Liability Company.

Revenues from Key Clients— 67%

Revenues from Key regions–32% exports

Risks —

Limited product range

Significant portion from few customers

Promoters past is the biggest risk. There are cases of non-compliance and criminal proceedings

Future

Company has grown revenues and profits and partially supported by ban of chemicals in China to support environmental policies

Due to specialty chemicals and market leader, company stands at good point to gain

Valuations

Reasonable considering peers in India in specialty chemicals. Fundamentals seems promising as of now

Should we apply?

Less chances of allotment due to small size. People who understand chemical business well can take the risk of applying

Less risk taking people can avoid

Listing day may see see moderate gains . Recommended to book profits if any on listing day

Keep an eye on promoter walk the talk scenario if holding for long

Also Read

Happiest Minds IPO crisp summary –Listing with substantial gains

Route Mobile IPO crisp Summary — Listing with substantial gains

Rossari biotech IPO detailed summary –Listed with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

CAMS– almost two decades of experience –is a technology-driven financial infrastructure and services provider to mutual funds and other financial institutions. Aggregate market share of approximately 70% based on mutual fund average assets under management (“AAUM”) managed by their clients and serviced by us

Offer purpose — 2258cr Complete offer for sale by promoters

Key Service domains – Mutual funds, AIF business, KYC registration, Insurance services business

Clients -SBI Mutual Fund, HDFC Mutual Fund, ICICI Prudential Mutual Fund, and Aditya Birla Sun Life Mutual Fund are serviced by CAMS

Revenues from Key Business— 85% ( mutual funds)

Risks —

Huge dependency on Mutual fund business with major revenue from it (more than 85%)

Significant disruptions in information technology systems can cause it a loss

Slow revenue growth in past few years

Risk of Regulators.

Pricing power can be a hurdle to grow earnings

Future

Long term growth seems reasonable and demand seems to increase in coming years with Indian Mutual fund industry set to grow

Almost all Major mutual funds are clients

Valuations

Expensive but considering almost duopoly, it can undergo time correction

Should we apply?

High chances of allotment. Less Risk taking people can avoid

Listing day can see (-8%) to 20% . Recommended to book profits if any on listing day

3+ year holding can give good returns even from this price if things workout well

Also Read

Happiest Minds IPO crisp summary –Listing with substantial gains

Route Mobile IPO crisp Summary — Listing with substantial gains

Rossari biotech IPO detailed summary –Listed with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

After a meltdown in Q4 in markets, there was an anticipation of meltdown which never happened. Is current market correction on the way to meltdown? Which stocks to buy/ which to leave? Questions galore!! Lets revisit some of the stocks which have decent set of results in Q1 of FY21

Also go through decent set of results in Q4 FY20

Don’t treat this post as a basis of investment. There are lot more factors to decide where a company will go in coming quarters. Discuss with your financial advisors before taking any position in stocks

Disclaimer : I may be fully biased while treating a company result as decent or bad

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Route Mobile– almost 16 yr old company –technology service provider specializing in communication services to enterprises. Acts as communication platform as a service

Offer purpose — 360cr as offer for sale by promoters and 240 cr as fresh issue. so 40% will flow to company to reduce loans, acquire companies etc

Key Service domains – Messaging services and Call center services

Clients -ICICI Bank, State Bank of India, Skype, Emirates Airlines, Bank of Maharashtra, WeChat, OSN and Viber.

Revenues from Key regions — 82% from exports, 12% from India,

Revenues from clients— Largest client 15% , 64% from top 10 clients

Risks —

Greater dependency on 3rd parties mobile network operations,Rely on 3rd party technology systems and infrastructure

Major revenues from limited client. So high concentration risk, although total clients 2500+.

Risk of potential claims resulting from the client’s misuse of its platform to send unauthorized text messages in violation of TRAI regulations.

Future

May gain from clients consistent need to serve more customers with limited resources

Billable transaction increasing at good rate and most companies pay it in advance

Long term growth seems reasonable and demand seems to increase in coming years

Valuations

Similar to peers in India and less than globally listed peers

Should we apply

High chances of over subscription and less allotment

Possible gains on Listing day can be seen but caution is advised to book profits if any

2+ year holding can give substantial gains if things workout well

Also Read

Happiest Minds IPO crisp summary –heavily subscribed

Rossari biotech IPO detailed summary –It came out with flying colors

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Happiest minds– approx 9 Yr old company in IT digital services with cloud infrastructure, SaaS, cyber security

Key Service domains – Product engineering services ( approx 50% of revenues), Infrastructure management and security services ( approx 20% revenues), digital business solutions (approx 26%)

Customers — Software development services for independent vendors like Amazon web services, Intel, IBM, Microsoft, Salesforce

Revenues from Key regions — 77% from US, 12% from India, 11% from UK approximately

Revenues from industry — Edutech, hitech and BFSI approx 50% of revenues

Risks —

Promoter have 29% shares pledged as of now

Company wrote of accumulated losses last year

Case for discriminatory employment

Future

May gain from WFH culture in coming years

May gain from cloud related digital services and cyber security services

Valuations – Lower than Mindtree and NIIT,

Should we apply

If you already have something related to digital IT services in your portfolio, you can avoid.

High chances of over subscription and less allotment

Possible gains on Listing day can be seen but caution is advised to book profits if any

Long term growth seems reasonable

Last one Rossari biotech IPO with prediction of 20% gains and good to hold for long term –It came out with flying colors

ROSSARI BIOTECH IPO : Quick analysis

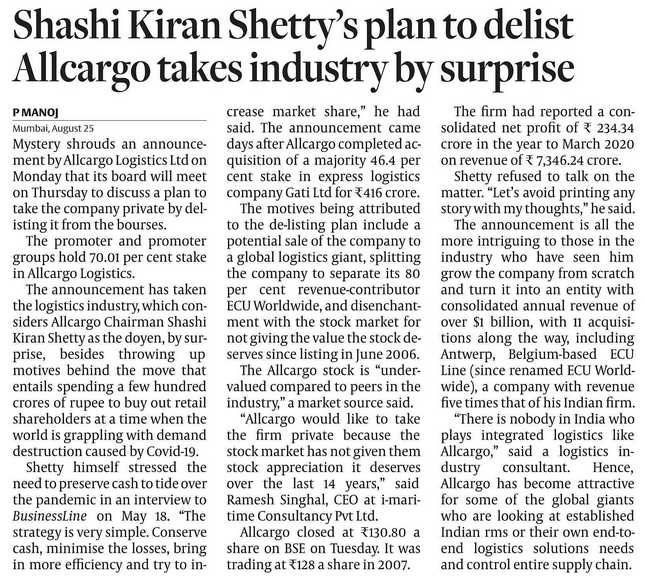

There are few companies who have announced plan to delist from Indian bourses. Most of these companies are either planning to sell their holding to global players or promoters want to take private control citing the markets not giving right valuations to their company stock prices.

Prominent names inlcude

Vedanta

Adani Power

Hexaware

and latest in the list is

All cargo logistics

This is different from delisting due to other reasons like Sancia Global Infraprojects Limited and Delma Infrastructure Limited where no trading happened for six months and these companies were planned to be removed from BSE exchange some time back

Recently 4 shocks shook the garment industry –highlighted few points from an article in Hindu business line — Read the full article to have better understanding

1. Shortage of import of raw materials from China which hit countries which are dependent on import

2. Cancelled order or delay in payment from brands

3. Lockdown by administartion

4 Dull demand and slow recovery due to macroeconomic trends

This all will contract the industry by 20-30% despite an opportunity to make masks and other related stuff

Also read : https://alpha-affairs.com/2020/08/19/yes-bank-path-to-recovery/

Also read : https://alpha-affairs.com/2020/08/19/one-more-blow-to-hospitality-industry/

Also see — https://alpha-affairs.com/2020/07/28/need-of-the-hour-efficiency-digitalisation/

A Must read on MOATS — https://alpha-affairs.com/portfolio/book-summary-the-little-book-that-builds-wealth-by-pat-dorsey/

6 months back, this was shared by company as the way forward. How much they achieved might have been reflecting now in its stock price.

What will happen in next 6 months can be judged from last 6 months!!

Three common ratios ( D/E), (Debt Service Coverage ratio) and (Interest service coverage ratio) represented in annual report and discussed at various places in quarterly results of many companies.

These numbers, if not given, can also be calculated if few details are looked into the report carefully

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Claim is “no serious adverse effects seen” which is positive

Only segment which shows growth is IT Services Business , shows a trend where money is moving, Other segment impacted least is POWER segment but margin are too low

Company is using the IPO proceeds for payment of earlier debt (~45%), Expansion (~35%) and other corporate purposes(~20%)

Company operates in three different segments and different countries thereby offering diversified products portfolio

Company providing customized solutions to specific industrial and production requirements of our customers primarily in the FMCG, apparel, poultry and animal feed industries through our diversified product portfolio comprising home, personal care & performance chemicals; textile specialty chemicals; and animal health and nutrition products. We operate in India as well as in 17 foreign countries including Vietnam, Bangladesh and Mauritius.

Largest manufacture of textile chemicals and leading manufacturer of acrylic chemicals

Company enjoy relationships in excess of five years with 12 out of their top 15 customers. Maintaining strong relationships with their key customers is, therefore, essential to their business strategy and to the growth of their business

Experienced Promoters with strong management team having domain knowledge

Good financial performance in past few years

The specialty chemicals industry is driven by both domestic consumption and exports. Home and personal care chemicals, water chemicals, construction chemicals, etc. are areas where specialty chemicals find applications. Exports are on the rise as India is becoming a central manufacturing hub for such chemicals. Tightening of environmental norms (eg. REACH regulations) in developed countries and the slowdown of China are contributing to the growth of exports.

Company is expanding its capacity by 20% to cater to growth in coming years.

Company is currently setting up another manufacturing facility at Dahej in Gujarat with a proposed installed capacity of 132,500MTPA which will enjoy proximity to the deep-water, multi-cargo port of Dahej. The proposed state-of-the-art facility will be well-equipped with advanced technologies and will be commissioned in Fiscal 2021

In order to remain competitive, Company must develop, test and manufacture new products and company has set-up a dedicated R&D centre at our Silvassa Manufacturing Facility and another one in Mumbai.

Growing consumption of environmentally friendly products: Rise of environmentally friendly specialty chemicals in India.

Growth in Household and I&I Cleaners market:The global household cleaners market is anticipated to reach USD 40.38 billion by 2025, growing at a CAGR of 4.4% from 2018 to 2023. The industrial and institutional cleaners market is expected to grow at a CAGR of ~6% during the forecast period. The growth of cleaners market will have direct implication on growth of home care chemicals market indicating a similar growth trajectory for the market

High population and growing need for hygiene:India is a thriving economy holding tremendous opportunities for cleaning chemicals companies. The country is second most populated country in the world. It is growing fast and the pace of urbanization is simply an unbelievable one. With these trends the country isalso facing a number of challenges. The incidence of infections is also increasing, paving way for the rise of homecare ingredients industry. The rapid urbanization is coupled with fast commercialization and millions of business establishments look for homecare products to meet their cleaning and hygiene requirements

Growing per Capita Consumption of Meat Products with High Demand for Animal Protein will drive the demand for Feed Additives, Especially Amino Acids

Strong Growth in the Livestock Feed Industry in developing regions with emerging demand forAquaculture feed will fuel the demand for Feed Ingredients

Rising Demand for Premium Pet Food will drive the Demand for Highly Specialized Ingredients

Some graphs from DHRP shows the potential and opportunity size for company

There is already a kind of downturn in the textile industry. Company significant sales comes from this sales channel. Company might be unable to increase or effectively manage the sales in short term in this category

There could be loss of any major institutional customers in our TSC and HPPC product categories or a reduction in their demand for our products due to COVID or unforseen circumstances. Significant portion of revenue also comes from this TSC and HPPC category. Revenue from top 5 customers itself is close to 35%

Company does not have any long term agreement with most of their customers and any impact in demand from customers will have a direct impact on revenues

Company has high dependence on sole manufacturing unit at Silvassa and Any disturbance, slowdown or shutdown of the Silvassa Manufacturing Facility can have a direct impact on revenue

Failure to develop new molecules in timely manner or failure to identify changing trends can seriously restrict the company growth

Company has high capital working requirement

Increase in the cost of raw materials as a percentage of revenue. Company largest expense is cost of raw materials. Primary raw materials are acrylic acid, surfactants and silicone oil. Cost of materials consumed represented 62.43%, 68.81%, 65.73% and 65.86%of company revenue from operations for the six months ended September 30, 2019 and in Fiscals 2019, 2018 and 2017, respectively. Company do not have long term agreements with any of their raw material suppliers and company acquire such raw materials pursuant to purchase orders from suppliers as a result of which, Company needs to forecast supply and demand and cause supply-demand mismatch

Further, the price of product is generally fixed at the time the purchase order is issued to company by customer and therefore company may not be able to pass on an increase in raw material to its customers. It shows that company does not have the pricing power

Technical risk -Failure to comply with the quality standards and technical specifications prescribed by institutional customers

Split/ Consolidation of equity shares in the last one year means IPO shares are with FV of 2Rs. So one should think that company is asking 5*425 Rs =2125Rs for IPO shares of FV 10 Rs

Company has also issues shares to other institutional investors @ same price which is normally uncommon but good part is it places retails investor on par with earlier institutional investors

Specialty chemical industry is going to be more competitive leading to further consolidation of market

Company Balance sheet looks good and Debt is in control.

Company presents a nice opportunity in growing field of chemicals and world moving away from China can really open the door for many companies growth. Rossari Biotech seems to be in the right place. With lot of competition in industry, growth may come in phases. Opportunity size available to grow

For investors IPO seems almost fully priced at the moment (FV 2 Rs and PE 31) if they are looking for short term gains. Depending upon market conditions on listing day, investors may get -10% to 20% gains.

Long term Investors can subscribe for 2-3 lots and hold. Look for Quarterly progress and add more or move to better opportunities available that time.

Please consult your financial advisor before applying in the IPO. Stock investments are risky in nature and may lead to capital loss

Enjoy investing!!

References

Most of the details gave been taken from Company DRHP.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Investor presentation here

Also Read : https://alpha-affairs.com/2020/07/05/automotive-key-mega-trends/

This is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There could be lot of things which which can have impact on share price and might be missed here due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

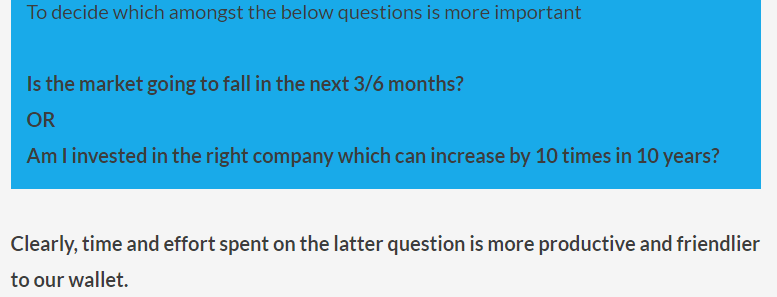

So instead of worrying about market fall or rise, decide on whether the companies invested are sound and safe and can increase your wealth in right proportions

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 21 June, 2020

Cycling; Running; Investing and Travel

Cycling: Trek Emonda review 2021 : Faster everywhere climbing (Cycling)

Investing: PE Ratio User Manual (EIPNY)

Running: Hamstrings strain and workout (ST)

Travel: Katmai Preserve (National Geographic)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

This is in series of posts where you can find the SWOT of a listed company along with factors to watch out for in coming quarters.

SWOT means

S – Strength of a company

W- Weakness of a company

O- Opportunities available for a company

T – Threats for a company

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Also Read – SWOT- Parag Milk Foods

Also Read – SWOT- SBI CARDS

Also Read – New to Stock Market : Part 1 : As Investor or Trader?

Also Read – Invest in stock markets only if

Investing is buying right stocks with right allocation at right price at opportune time with exit strategy in place Experience counts!!

Lets invest!!

Join our Equity booster plan at very nominal fees get in touch https://wa.me/919740311223?text=interestedinequityboosterplan

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 13 June, 2020

Daily habits which drains you; Naturals icecream; Leadership and Megatrends; Photography

Daily Habits: 10 Daily habits that drain your energy (Deeph)

Naturals: Ice-cream and summer of COVID-19 (BQ)

Leadership: Mega-trends and leadership : value investing (Youtube)

Photography: Free Software a photographer inside you needs (Lights)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 06 June, 2020

Flexible EMI repayment; PVR losses; How to disagree; What we can do to help while volunteering; Kerala’s Rubber Man

MOVIES: PVR Our losses are mounting (Forbes)

Finance: Flexible EMI repayment options may burn hole (Mint)

Leadership: How to disagree respectfully(Magneticspeaking)

Volunteering, Activism: What we can do to help : First Steps in activism (Medium)

Rubberman: JJ Murphy Kerala’s rubber man (LHI)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Please note that I had hold positions in DMART stock in past and exited and may hold in future as well. I may be fully biased in the below opinion. Please don’t take it as investment advice. Its just sharing of what i observed and reader is advised to do due diligence before acting on opinion

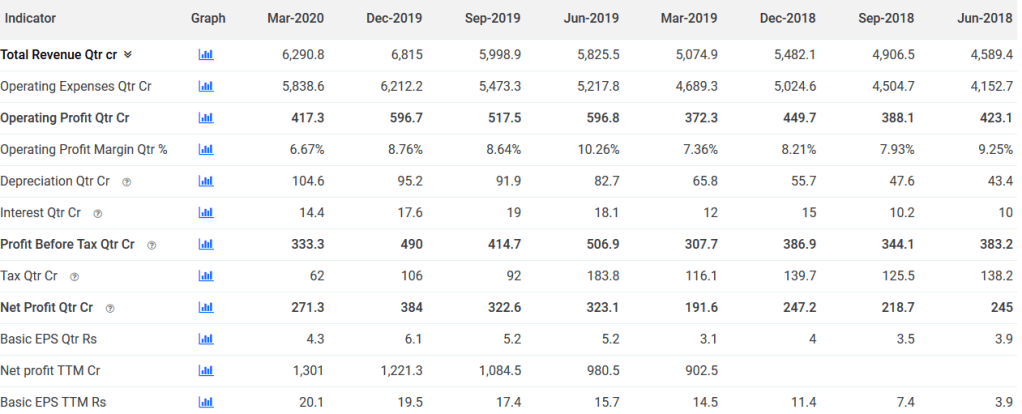

Dmart is a stock which i am tracking from IPO days. Could not get IPO allocation but I entered into it at very late stage and also exited without making much gains. The Reasons are aplenty but as we see it is also a stock which has defied gravity in valuations. Here i am trying to find the correlation with the results announced for Q4 and full FY19-20 with what i have observed a month back and shared to people on twitter. .

This what i observed and shared a month back on 22nd April 2020

Almost 50% stores closed for a month, open stores only selling essential items like grocery which have low margin, other things like clothes, utensils (high margin business) is closed because of less staff operating. Open stores have less footfall, there is limit as well on items that can be taken out while on the other side they need to keep store open for longer time –our area 24 hrs open, instead of normal 10am-9pm ..so more operating costs. Plus operating expenses are rising because of social distancing, sanitation of trolleys, infrared thermometers, sanitizes to people when they enter the store , Electricity expenses, Getting worker to work at night shift may increase salary allowance. More people in line has forced DMart to put up tents outdoors. So less revenues, more expenses, profit will take a plunge in coming time. And now enters JIO deal. A bigger challenge for dmart to retain customers. May force them towards home delivery with shrinking margins My view at that time was to exit DMART and re-enter later.

What happened to DMART price. From the point i exited, it went from 2150 to 2380 in last one month

Sounds familiar!!

You sell a stock, it goes high

You buy a stock, it goes low

Amazing isn’t it!!!

But here the pain is less, atleast till now, as i was waiting for Q4 results to take a fresh call .

So how was DMART results on 23rd May 2020?

First glance at results shows solid performance with approx 24% increase in YOY revenues, 29 % yoy growth in EBITDA and 60% rise in EPS YOY. Looks like i missed the bus by selling my position and already stock by approx 10%.

Still i decided to delve deeper into results and compared Q-O-Q numbers (Q4vs Q3 of FY19-20). I saw a decline in Revenue as well as EBITDA and only 8 days were the stores closed in Q4. Why did the Q4 numbers so weak? I thought actual impact should be visible in Q1 FY21 but here Q4 revenue decline is not making much sense? It is beyond my imagination that only 8 days has caused such havoc in Q4 numbers. I was not able to solve the puzzle for quite some time. Could not get any clue and I was re-reading the results & commentary again and again.

I pulled out numbers for past 8 quarters and there you go!! It confirms that Q4 is a historically weak quarter. But here the decline from Q3 to Q4 was 30% approx while in the past years the decline from Q3 to Q4 profits were limited to 20%. Somehow what i observed a month back starts making some sense . 8 days of lockdown did have an impact and its clearly visible in Q4 numbers.

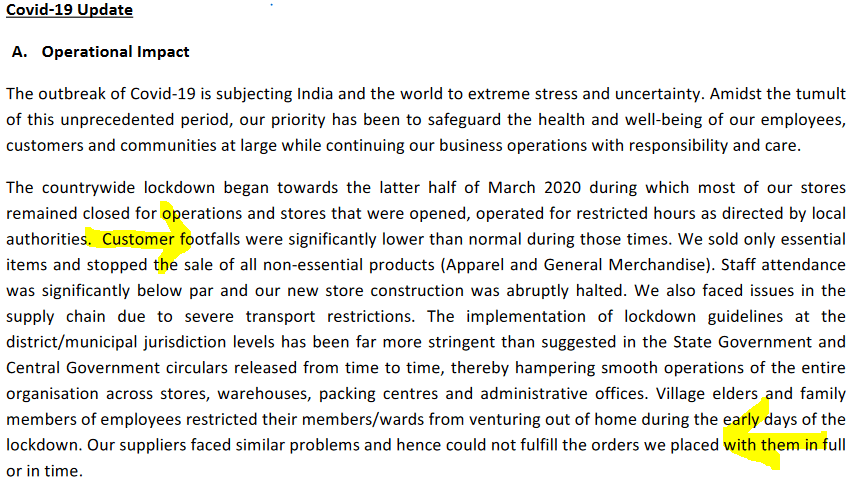

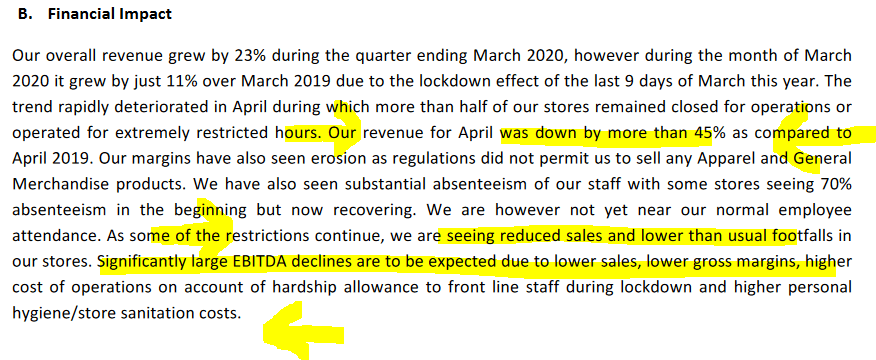

I reached to Management commentary and in section Covid-19 update, Management very clearly reflected on the lock-down observations and its impact on business. I am highlighting the paras below for your readings.

Reading the paragraphs gave me a sense of relief that missing such bus last month might not be not painful in long run. It also highlight the fact that while the results may look better at first glance but they are more than mere numbers and why one should go deeper to understand the results.

Entry of JIO MART along with COVID-19 lockdown may be a lethal combination for DMART. We need to see how the company performs in coming days and will NEWTON’s gravity will finally pull the stock down or not at all.

I don’t yet know whether i may get a chance to board the bus again or not as stocks prices can remain irrational longer than one’s patience!! I am also skeptical as of now whether bus should be boarded at all. I may be totally wrong as i see there are people who are predicting or rather speculating that all is well with company and stock price is on way to 3200!!! Its better to wait and watch from sidelines although I would be really surprised if the DMART stock reaches 3000 levels before retreating back to 2000 or 1900 levels. But Stock markets can really make you go crazy at times.

Please share your opinion on what you think about DMART stock price

We will revisit this post possibly after Q1 results again and learn more from markets.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Interesting to see how many from solid and good results will move to Average and bad results category after Q1 FY21 results. Those who survive in good or solid category even after Q1’FY21 should be worth researching more to invest

Don’t treat this post as a basis of investment. There are lot more factors to decide where a company will go in coming quarters. Discuss with your mentors or financial advisors before taking any position in stocks

Recently there is lot of debate among seasoned investors whether one should buy ITC or not. There seems to be two groups and one will win and brag about it for sure!! Watch out

One group heavily invested from past few years and increasingly purchasing shares recently and in the process justifying their decision that good companies come back strongly

Other group is constantly pushing the value bar towards low and in the process strengthening the bear cartel for ITC.

Time will tell which group survives and thrives but for our readers i compiled few amazing threads on same. Read and let us know which camp do you support? and why?

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Reliance Industries have shared the Q4 Results of FY19-20 as well as FY19-20 full year results. Company also proposed a rights issue @ 1257 Rs.

Should an investor subscribe to it or not depends upon the holding price of investors current holdings

Below snap shows potential scenarios whether investor can benefit or not

As we can see, only two types of investors can benefit

There is third type of investor who has bought Reliance shares in near past (scenario 1) in anticipation of Rights issue and dividend, actually they don’t have much to gain in current scenario until reliance shares moves up. So they should wait to subscribe based on cutoff date for Right issue and also check Reliance share price that time.

For rest of the investors its either negative or neutral.

Above example shows potential scenarios. Please do your due diligence before making investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Banking and finance sector is the worst performer in recent months and there are high chances that it will continue to do so. There could be multiple reasons for same including defaults in payments and slow credit growth

Below is the list of Public and private sector banks with NIM, Net NPA %and Gross NPA% as of 17th April 2020. It may help you to make an investment decision more prudently. Don’t forget to consult your financial adviser before doing so.

Given a choice based on this data, the below banks seems better than other banks on certain criteria.

![]() Be aware that these NPA numbers has a high probability of increase in next two quarters.

Be aware that these NPA numbers has a high probability of increase in next two quarters.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Looking at HDFC Bank Q4 confcall transcript analyses. One key point was discretionary spending on cards is effecting total spending. This do not bode well for companies like SBI cards where not only spending goes down but it will hit the profit as well due to late payment and increase of NPA in certain cases.

Also Read : SWOT analysis : SBI Cards

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.