The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Likhitha Infra– (approx 32 yr old company) is an Oil Gas Pipeline Infrastructure provider in India. Focused on laying pipeline networks, Operation and maintenance of city gas distribution companies in India

Offer purpose — 61 crores to meet working capital requirement

Key Service domains – Cross country pipelines, City gas distributions including CNG stations, Operation and maintenance

Clients -Established players from Oil and Gas industry

Risks —

Major revenue from few clients may deprive the company from pricing power

Inherent risks due to long term nature of projects

Future

CGD is increasing in India and company is at right place for its business to grow with Strong client base, Efficient business model Strong project execution capabilities , Diversified geographical presence in India

Valuations

Seems attractive

Should we apply?

People can subscribe for long term growth prospects

Listing day may see gains . Recommended to hold and buy more if listed at IPO price +/-10%

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

UTI -In top 10 AMC , manages mutual funds, PMS, NPS, AIF and offshore funds

Offer purpose — Offer of sale by existing stakeholders

Key Service domains -Managing domestic mutual funds, PMS, alternate investment funds, retirement unds and offshore funds

Clients -Postal and retiree PMS and NPS services. High concentration in B30 markets segment

Revenues from Key Services–Domestic Mutual funds AUM. PMS and NPS income constitute only 3% although with higher AUM

Risks —

SEBI policy like change in total expense ratio, re-categorization of various schemes, upfront commissions in the past led to lower incomes. Future policy changes can also pose a risk

Large portion (almost 75%) of UTI AMC assets under management in 6-7 active funds, so large scale redemption can be cause of worry

Falling Market share and fall of revenue from operation in last two years is overhang

Financials are on weak foot with ROE mostly 11-13% on an average

Future

Increasing awareness among people about equity investments and growing popularity of Mutual funds can boost revenues

Increasing concentration in B30 Markets segment can boost revenues where they can charge higher TER

Valuations

Optically cheaper valuation as compared to HDFC AMC and NIPPON AMC

Should we apply?

Good chances of allotment.

While valuation, business seems to be in right place but financials are only one thing which leads to– Avoid for IPO subscription

Listing day may see -10% to +10% gains . Recommended to book profits if any on listing day.

Wait and watch policy is best for long term investment in UTI AMC

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Angel Broking – the fourth largest broking firm in India as per active client accounts on NSE. The company provides its services through online and digital platforms on the back of a network of more than 11,000 sub-brokers as on June 30, 2020.

Offer purpose — 600cr offer for sale + fresh issue. 40% will be used for working capital requirement by company

Key Service domains – provides broking and advisory services, margin funding , loans against shares and financial products distribution to its clients.

Clients -80% from tier 2 and tier 3 cities

Revenues from Key Services–75% from broking. 10% from Margin funding

Risks —

The company’s main revenue source is the broking business, and company has not diversified into wealth management kind of services

Intense competition in broking business

Extensive supervision and regulation by various regulatory bodies that may cause fluctuation in earnings e.g. recently SEBI margin trading rule

Future

Flat fee-based model, a developing derivatives market, the use of modern technology, lower penetration of mutual funds and shares and debentures in household savings and customer acquisition through digital medium enable the company to scale up its business easily.

Digital acquisition of customers will save cost

Valuations

Little on higher side.

Should we apply?

Moderate chances of allotment due to small size.

People can avoid to subscribe

Listing day may see see moderate gains . Recommended to book profits if any on listing day

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Chemcon– is a manufacturer of specialized chemicals, such as HMDS (Hexamethyl Disilazane) and CMIC (Chloromethyl Isopropyl Carbonate) and is market leader in both products. This are predominantly used in the pharmaceuticals industry, and inorganic bromides, namely Calcium Bromide, Zinc Bromide and Sodium Bromide, which are used as completion fluids in the oilfields industry

Offer purpose — 318cr Complete offer for sale by promoters

Key Service domains – Pharmaceuticals and oilfields industry

Clients -Hetero Labs Limited, Laurus Labs Limited, Aurobindo Pharma Limited, Sanjay Chemicals (India) Private Limited, and the key customers of Oilwell Completion Chemicals include Shree Radha Overseas, Water Systems Specialty Chemical DMCC, Universal Drilling Fluids and CC Gran Limited Liability Company.

Revenues from Key Clients— 67%

Revenues from Key regions–32% exports

Risks —

Limited product range

Significant portion from few customers

Promoters past is the biggest risk. There are cases of non-compliance and criminal proceedings

Future

Company has grown revenues and profits and partially supported by ban of chemicals in China to support environmental policies

Due to specialty chemicals and market leader, company stands at good point to gain

Valuations

Reasonable considering peers in India in specialty chemicals. Fundamentals seems promising as of now

Should we apply?

Less chances of allotment due to small size. People who understand chemical business well can take the risk of applying

Less risk taking people can avoid

Listing day may see see moderate gains . Recommended to book profits if any on listing day

Keep an eye on promoter walk the talk scenario if holding for long

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

CAMS– almost two decades of experience –is a technology-driven financial infrastructure and services provider to mutual funds and other financial institutions. Aggregate market share of approximately 70% based on mutual fund average assets under management (“AAUM”) managed by their clients and serviced by us

Offer purpose — 2258cr Complete offer for sale by promoters

Key Service domains – Mutual funds, AIF business, KYC registration, Insurance services business

Clients -SBI Mutual Fund, HDFC Mutual Fund, ICICI Prudential Mutual Fund, and Aditya Birla Sun Life Mutual Fund are serviced by CAMS

Revenues from Key Business— 85% ( mutual funds)

Risks —

Huge dependency on Mutual fund business with major revenue from it (more than 85%)

Significant disruptions in information technology systems can cause it a loss

Slow revenue growth in past few years

Risk of Regulators.

Pricing power can be a hurdle to grow earnings

Future

Long term growth seems reasonable and demand seems to increase in coming years with Indian Mutual fund industry set to grow

Almost all Major mutual funds are clients

Valuations

Expensive but considering almost duopoly, it can undergo time correction

Should we apply?

High chances of allotment. Less Risk taking people can avoid

Listing day can see (-8%) to 20% . Recommended to book profits if any on listing day

3+ year holding can give good returns even from this price if things workout well

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

After a meltdown in Q4 in markets, there was an anticipation of meltdown which never happened. Is current market correction on the way to meltdown? Which stocks to buy/ which to leave? Questions galore!! Lets revisit some of the stocks which have decent set of results in Q1 of FY21

Don’t treat this post as a basis of investment. There are lot more factors to decide where a company will go in coming quarters. Discuss with your financial advisors before taking any position in stocks

Disclaimer : I may be fully biased while treating a company result as decent or bad

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Multicap Funds — most diversified equity mutual funds that can put money in stocks across market capitalization.

Sebi new direction for multicap funds– Allocate minimum 25% each in large, mid and small cap by Feb 2021

Purpose : Recently these funds have been found to invested heavily towards large caps and Regulator’s move aimed at reducing risk of concentration in large-cap stocks and making market broad based. This way these funds can be truly labelled as Multi-cap

One quick estimate from a Quantum fund manager shows that 40% of entire MF industry equity investment is concentrated in top 6 large cap stocks thereby posing a huge concentration risk.

Why multicap loaded towards these large caps — to beat the benchmar index which has heavily loaded in these large caps

What all these changes can lead to

Multi cap fund managers to diversify and find opportunities in small and mid cap segment

Selling in Large cap stocks and some of mid cap stocks

Reshuffling of multicap funds portfolios multiple times for diversification and hence estimate is 25K cr will move into mid cap and small cap

Liquidity issues while investing in small caps –some of these small caps will become mid caps just by so much money coming into them and leading into ASM framework or mid caps becoming small caps because of selling pressure

Recategorisation of multicap funds into Large cap MF or Large and Mid cap mutual funds

Merging of few MF schemes into another in same fund house

Will small cap and mid cap stocks rally because of this?Should we buy more small cap and mid cap stocks?

Initial euphoria may drive this rally but retail people should understand the possibilities before putting their hard earned money

AMFI will release a list of Large , mid and small cap on Dec 2020 that will for the basis for this categorization.

Funds can merge into anther fund

Funds can contest this regulation

There could be a crash around the corner because of valuations racing ahead of economy data in many stock counters. So the list of mid and small caps can be entirely different if market correction happens before Dec2020

So any wrong move without due diligence can lead a retail investor into proud owner of junk stocks.

Best way is to own the business what you understand and have conviction. Other things will fall in place for you

Should we sell Multicap funds or buy them?

Stay invested in multi cap funds although one should not be having more than one or two of such category of funds.

Any such funds which will be recategorised as large cap funds will not change your returns much

Any such funds who will reshuffle their portfolio can go through short term pain but returns can be better in long run

Will this regulation stay? and is it good?

I see it as a good regulation because it helps in removing the concentration risk in few stocks from MF industry and as years progresses, this industry is bound to grow by leaps and bounds. This kind of framework helps in longer run although its a big pain in shorter run. It also helps few fund managers to showcase their skills for which we are spending 2-3% of expense ratio. Otherwise we are better off with Index ETF MF with lowest expense ratio if fund managers skills are absent and don’t make any difference to my returns

Happy investing!!

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Route Mobile– almost 16 yr old company –technology service provider specializing in communication services to enterprises. Acts as communication platform as a service

Offer purpose — 360cr as offer for sale by promoters and 240 cr as fresh issue. so 40% will flow to company to reduce loans, acquire companies etc

Key Service domains – Messaging services and Call center services

Clients -ICICI Bank, State Bank of India, Skype, Emirates Airlines, Bank of Maharashtra, WeChat, OSN and Viber.

Revenues from Key regions — 82% from exports, 12% from India,

Revenues from clients— Largest client 15% , 64% from top 10 clients

Risks —

Greater dependency on 3rd parties mobile network operations,Rely on 3rd party technology systems and infrastructure

Major revenues from limited client. So high concentration risk, although total clients 2500+.

Risk of potential claims resulting from the client’s misuse of its platform to send unauthorized text messages in violation of TRAI regulations.

Future

May gain from clients consistent need to serve more customers with limited resources

Billable transaction increasing at good rate and most companies pay it in advance

Long term growth seems reasonable and demand seems to increase in coming years

Valuations

Similar to peers in India and less than globally listed peers

Should we apply

High chances of over subscription and less allotment

Possible gains on Listing day can be seen but caution is advised to book profits if any

2+ year holding can give substantial gains if things workout well

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

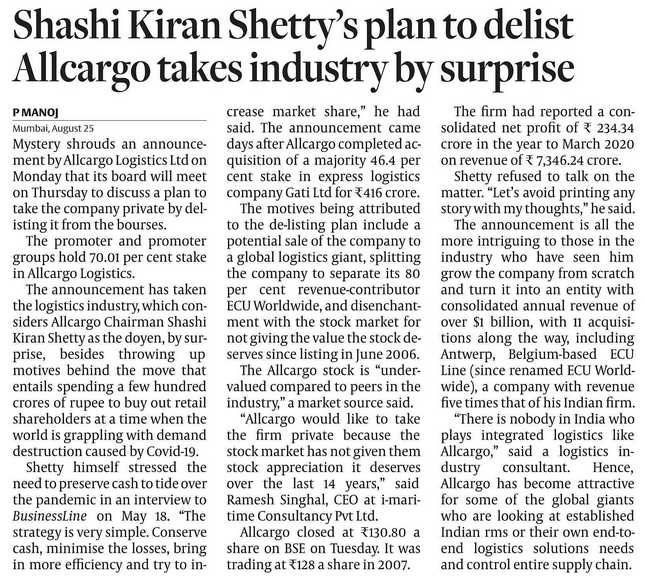

There are few companies who have announced plan to delist from Indian bourses. Most of these companies are either planning to sell their holding to global players or promoters want to take private control citing the markets not giving right valuations to their company stock prices.

Prominent names inlcude

Vedanta

Adani Power

Hexaware

and latest in the list is

All cargo logistics

Business line

This is different from delisting due to other reasons like Sancia Global Infraprojects Limited and Delma Infrastructure Limited where no trading happened for six months and these companies were planned to be removed from BSE exchange some time back

Recently 4 shocks shook the garment industry –highlighted few points from an article in Hindu business line — Read the full article to have better understanding

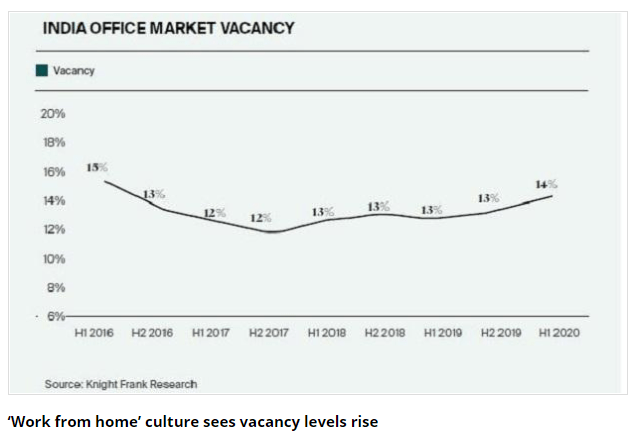

Looking at Knight Frank report and few article here and here , it seems best to wait for a quarter or half year to get the best deal out of real estate.

Real estate sales for residential units at low and office units vacancy at high

It is so easy to get caught in anxious or little overwhelming situation if one is riding the bicycle after a long number of years. This anxiety become more if one has not rode the geared bicycle before. Most of us have done cycling in childhood and possibly we might have done some stunts with it as well. It is one of the best remembered gifts from parents in our younger days and we had cycled for reasons which are quite different than our primary goal (fitness) nowadays. I see the same brightness in kids for cycle that was once we had. Surprisingly that charm has not gone away when as a adult we want to start cycling again. To make it easier to start cycling again, the very first thing i can tell you is to forget the rules. Here I listed few cycling tips, which i believe may help you to get back to cycling without losing the big picture.

Start Riding and Having Fun

Fitness should be part of your life and not something you do for a month or a year. You shouldn’t be the one who’s cycling for a month after buying and then dozing off. So forget the rules, forget the gears, terrains, matching helmets, jersey. The Whole idea to get fall in love with cyclingagainand enjoy. So until you have fun riding cycle, you will not be able to reap fitness benefits and will lose interest soon. More Focus on building habits and Less focus on results or outcome.

Adjust Saddle Height and have some basic maintenance tools handy

Saddle height should be adjusted in such a way that so that you don’t suffer knee pain or injury. Knee should be slightly bend while riding. Get the fix done by a professional if you are unsure. A small video youtube can help.

Some basic maintenance tools like puncture kit, small pump should be handy with you on long ride distances even if you don’t know how to fix your cycle. You may get help of fellow cyclists but you need to have basic kit available with you.

Single gear Cycle. Don’t stress out! Multi-Gear Cycle. Good!

It really Does not matter if you have a single geared cycle as a starter. Idea is not to stress out. It is fine to start with single gear cycle and spend as less you can in starting phase. Soon you will figure out the best bicycle for you. NO point buying a road bike when you found out later that hybrid is the best serving your purpose or the commute bike is what you need instead of mountain bike

If you have basic 1*6 or 3*7 geared cycle, you are good to go bit further distance wise and if you have higher geared cycle, nothing like it. But it can be complicated initially for starters on higher geared cycle. So what one needs to take care is to keep the front derailleur on the 2nd gear(middle gear) and keep changing the back gears as per ride, terrain. This will help to avoid crossing chaining . Within no time, one will be able to adjust the front gears and back gears combination.

Change gears while pedalling:

Remember the best way to change gears is while one is pedalling non stop. This way the chain easily moves from one cog to another. While changing the gear, dont put pressure on the pedal as this could lead to the snapping of chain in extreme scenario.

Build up the ride distance gradually:

Start with a 3km or 5km or 10km ride in first few days and never be in a hurry to ride more distances.. Gradually build up the ride distances. Ride slowly for first 2 km or so and then settle into a rhythm and enjoy the ride.

Join a cycling group and learn from experienced people :

Join a local cycling group in your neighbour hood. Make new friends and start riding with similar mindset people. You will get to know a lot about nutrition, bike maintenance, bike, terrains, routes. What to do and what not to. On your first ride, make a plan to ride in second part of pack but don’t get lost. Have a proper planning in place before you start to ride in a group and long distances.

Always remember to refuel and hydrate yourself

Dont start empty stomach for long distances. If the ride is over an hour then plan to take an energy bar or something handy to eat. A bottle of water may not be sufficient for long distances. Plan to hydrate on the way. Keeping a small electron bottle with you to restore lost electrolytes

Have a Consistent Approach & build habit

Consistency is the key

Having a weekly routine or a scheduled regime will help you to be consistent. Make it a point to cycle every weekend and soon you will be scaling new heights

Only showing up daily will work wonders in the starting phase and as you progress, you can create a routine.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

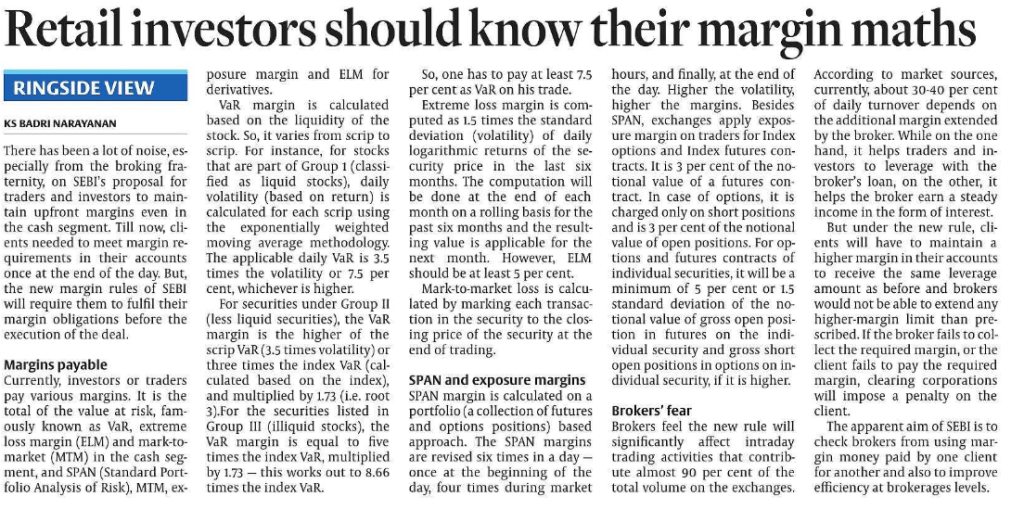

A move which seems bad for both retailer and broker in its first look!!! But devil lies in details. Its a move which will help everyone

SEBI aim is to check rampant usage of margin money paid by one client for another. The whole exercise looks to protect retail investors and in my view its a very good move for long term. This move i believe will limit the number of people leaving markets forever with losses as it may reduce the risk a retail investor can take with his money.

Brokers need to get this point that in long term their operations become efficient and their survival improves because investors will increase.

Retail investor has to understand that limiting margin will help them to take calculated risks and improve their chances of profit

BOGUS people will be filtered out. That’s the expected bonus

Source : Hindu Business Line

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Three common ratios ( D/E), (Debt Service Coverage ratio) and (Interest service coverage ratio) represented in annual report and discussed at various places in quarterly results of many companies.

These numbers, if not given, can also be calculated if few details are looked into the report carefully

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

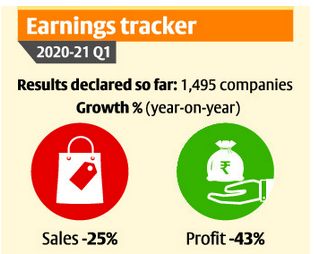

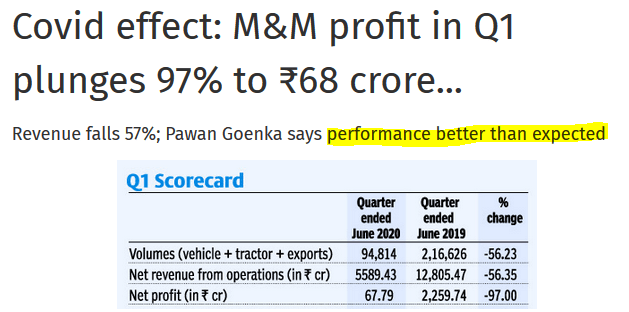

Earnings will remain depressed for a quarter more seeing the outlook and impact

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Only segment which shows growth is IT Services Business , shows a trend where money is moving, Other segment impacted least is POWER segment but margin are too low

Company is using the IPO proceeds for payment of earlier debt (~45%), Expansion (~35%) and other corporate purposes(~20%)

Strength

Company operates in three different segments and different countries thereby offering diversified products portfolio

Company providing customized solutions to specific industrial and production requirements of our customers primarily in the FMCG, apparel, poultry and animal feed industries through our diversified product portfolio comprising home, personal care & performance chemicals; textile specialty chemicals; and animal health and nutrition products. We operate in India as well as in 17 foreign countries including Vietnam, Bangladesh and Mauritius.

Largest manufacture of textile chemicals and leading manufacturer of acrylic chemicals

Company enjoy relationships in excess of five years with 12 out of their top 15 customers. Maintaining strong relationships with their key customers is, therefore, essential to their business strategy and to the growth of their business

Experienced Promoters with strong management team having domain knowledge

Good financial performance in past few years

Opportunities

The specialty chemicals industry is driven by both domestic consumption and exports. Home and personal care chemicals, water chemicals, construction chemicals, etc. are areas where specialty chemicals find applications. Exports are on the rise as India is becoming a central manufacturing hub for such chemicals. Tightening of environmental norms (eg. REACH regulations) in developed countries and the slowdown of China are contributing to the growth of exports.

Company is expanding its capacity by 20% to cater to growth in coming years.

Company is currently setting up another manufacturing facility at Dahej in Gujarat with a proposed installed capacity of 132,500MTPA which will enjoy proximity to the deep-water, multi-cargo port of Dahej. The proposed state-of-the-art facility will be well-equipped with advanced technologies and will be commissioned in Fiscal 2021

In order to remain competitive, Company must develop, test and manufacture new products and company has set-up a dedicated R&D centre at our Silvassa Manufacturing Facility and another one in Mumbai.

Growing consumption of environmentally friendly products: Rise of environmentally friendly specialty chemicals in India.

Growth in Household and I&I Cleaners market:The global household cleaners market is anticipated to reach USD 40.38 billion by 2025, growing at a CAGR of 4.4% from 2018 to 2023. The industrial and institutional cleaners market is expected to grow at a CAGR of ~6% during the forecast period. The growth of cleaners market will have direct implication on growth of home care chemicals market indicating a similar growth trajectory for the market

High population and growing need for hygiene:India is a thriving economy holding tremendous opportunities for cleaning chemicals companies. The country is second most populated country in the world. It is growing fast and the pace of urbanization is simply an unbelievable one. With these trends the country isalso facing a number of challenges. The incidence of infections is also increasing, paving way for the rise of homecare ingredients industry. The rapid urbanization is coupled with fast commercialization and millions of business establishments look for homecare products to meet their cleaning and hygiene requirements

Growing per Capita Consumption of Meat Products with High Demand for Animal Protein will drive the demand for Feed Additives, Especially Amino Acids

Strong Growth in the Livestock Feed Industry in developing regions with emerging demand forAquaculture feed will fuel the demand for Feed Ingredients

Rising Demand for Premium Pet Food will drive the Demand for Highly Specialized Ingredients

Some graphs from DHRP shows the potential and opportunity size for company

Global specialty chemical market

Indian specialty chemical market

Risks

There is already a kind of downturn in the textile industry. Company significant sales comes from this sales channel. Company might be unable to increase or effectively manage the sales in short term in this category

There could be loss of any major institutional customers in our TSC and HPPC product categories or a reduction in their demand for our products due to COVID or unforseen circumstances. Significant portion of revenue also comes from this TSC and HPPC category. Revenue from top 5 customers itself is close to 35%

Company does not have any long term agreement with most of their customers and any impact in demand from customers will have a direct impact on revenues

Company has high dependence on sole manufacturing unit at Silvassa and Any disturbance, slowdown or shutdown of the Silvassa Manufacturing Facility can have a direct impact on revenue

Failure to develop new molecules in timely manner or failure to identify changing trends can seriously restrict the company growth

Company has high capital working requirement

Increase in the cost of raw materials as a percentage of revenue. Company largest expense is cost of raw materials. Primary raw materials are acrylic acid, surfactants and silicone oil. Cost of materials consumed represented 62.43%, 68.81%, 65.73% and 65.86%of company revenue from operations for the six months ended September 30, 2019 and in Fiscals 2019, 2018 and 2017, respectively. Company do not have long term agreements with any of their raw material suppliers and company acquire such raw materials pursuant to purchase orders from suppliers as a result of which, Company needs to forecast supply and demand and cause supply-demand mismatch

Further, the price of product is generally fixed at the time the purchase order is issued to company by customer and therefore company may not be able to pass on an increase in raw material to its customers. It shows that company does not have the pricing power

Technical risk -Failure to comply with the quality standards and technical specifications prescribed by institutional customers

Important point to note

Split/ Consolidation of equity shares in the last one year means IPO shares are with FV of 2Rs. So one should think that company is asking 5*425 Rs =2125Rs for IPO shares of FV 10 Rs

Company has also issues shares to other institutional investors @ same price which is normally uncommon but good part is it places retails investor on par with earlier institutional investors

Peers in different segments and Comparison

Specialty chemical industry is going to be more competitive leading to further consolidation of market

Financial snap

Company Balance sheet looks good and Debt is in control.

Final conclusion

Company presents a nice opportunity in growing field of chemicals and world moving away from China can really open the door for many companies growth. Rossari Biotech seems to be in the right place. With lot of competition in industry, growth may come in phases. Opportunity size available to grow

For investors IPO seems almost fully priced at the moment (FV 2 Rs and PE 31) if they are looking for short term gains. Depending upon market conditions on listing day, investors may get -10% to 20% gains.

Long term Investors can subscribe for 2-3 lots and hold. Look for Quarterly progress and add more or move to better opportunities available that time.

Please consult your financial advisor before applying in the IPO. Stock investments are risky in nature and may lead to capital loss

Enjoy investing!!

References

Most of the details gave been taken from Company DRHP.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Failure does not exist. Only thing you are a failure on Monday when you don’t learn and progress from it on Tuesday and day after!!

You will not regret watching this

Failure is figment of imagination

Winner do not make excuses

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

This is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There could be lot of things which which can have impact on share price and might be missed here due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Article says that one will have miniscule impact on long term basis and major impact on liquid or overnight funds

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

So instead of worrying about market fall or rise, decide on whether the companies invested are sound and safe and can increase your wealth in right proportions

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Your initial due diligence might get you into a position but your maintenance due diligence is what will make you the big money and save you from big losses. Don't rely on yesterdays analysis. Companies are always evolving in good and bad ways. Know what you own at all times.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

This is in series of posts where you can find the SWOT of a listed company along with factors to watch out for in coming quarters.

SWOT means

S – Strength of a company

W- Weakness of a company

O- Opportunities available for a company

T – Threats for a company

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Ten thumb rules on fitness 1. Strength is the FOUNDATION that enhances all forms of training. Give 60% of training to strength training 2. Only thing that makes u fat is eating in calorie surplus. Rest all is marketing.Simple chijon ki Value nahin, so it’s made complicated.

Leadership: Mega-trends and leadership : value investing (Youtube)

Photography: Free Software a photographer inside you needs (Lights)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.