Alivira : Animal Health Award Winner

BE FINANCIALLY INDEPENDENT

The lore goes that in British India, the city of Delhi was infested with cobras, so the administration announced a cash reward for submission of dead cobras. What did this policy do?

People of Delhi started rearing cobras, killing them, and then taking them to the authorities to collect their cash rewards. Instead of reducing Delhi’s cobra population, the policy turned the city’s homes into cobra farms. The administration was spending more and

more money, and the cobra population was increasing.

No one knows if this story is true. But it has come to be known as the cobra effect to demonstrate how governments often create wrong incentives for people and make policies that result in worsening problems rather than solving them

Excerpt taken from Puja Mehra article in Wealth Insight

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Home First Finance IPO– 10 yr old company promoted by private equity funds.

Business — In the affordable housing segment in 11 states with 70 branches. 80% business from 4 states including 40% from Gujarat only

Offer purpose — Offer for sale (1153cr) including fresh issue of 265 cr. for expansion and general purposes

Key domains – Affordable housing finance for construction , loans for purchasing commercial property and loans against property to both salaried and small business owners/self-employed customers

Risks —

Consistently need to remain in limelight in highly competitive industry, Key financial metrics are not great as of now

With focus on middle class and recent Covid impact , NPA will always be struggle for few quarters

Strength

Focus on growing affordable housing category for middle income and low income category which is not serviced by many big banks

Company use technology to its advantage and do fast processing of loans

Average ticket size is 10 lacs approximately which makes it target highly growing category of loans

Future

Various government initiatives such as housing for all, amongst others are likely to offer exciting growth opportunities in the coming years.

Last three years CAGR is 60% plus although on smaller base shows future seems bright if it remains on track

Valuations

In almost all aspects except PE, Better listed options available

Should we apply?

People can avoid or subscribe only for listing gains

Recommended to sell if getting gains on listing day

One can wait to enter at low prices for investment purposes or choose peers for investment purpose during corrections

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

UTI AMC IPO crisp Summary — Listed with loss as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Angel Broking IPO crisp summary –Listed with loss as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Stove Kraft IPO– Almost 20 yr old company involved in manufacturing, marketing and exporting kitchen appliances

Business — Company is into manufacturing LPG gas stoves, induction cooktops, non-stick cookware, pressure cookers, chimneys etc

Offer purpose — Offer for sale (412cr) including fresh issue of 95 cr. for repayment of debt and general purposes

Key domains -Company have three different segments. Pigeon for Mass market, Gilma for Mid level and Balck and Decker at top level premium category

Risks —

Company has yet to show sustainable profits.

It is operating in field of established players like Prestige, Hawkins so with such intense competition, profits margins will always face heat.

Company has ongoing litigation and not efficient to recover money from retailers.

Company has been into unrelated segments like LED which can derail the focus on key categories

Customers may not remain loyal as switching to other brands is easy, so basically no moat

Strength

Company has two under-utilised plants which can be ramped up without any major capex

Company have different brands catering to different segments and have good reputation of its products

Company has multiple distribution channels including e-commerce

Future

Market is expected to grow at 11% CAGR in near future

Company existing capacity is not fully utilised and with growth of overall market, company has room to grow

There is a systematic shift happening towards usage of kitchen appliances

Valuations

Recently turned profitable company with low ROE and margins seeking almost equal valuations as leaders in their categories

Bullish market and IPO frenzy makes the valuations stretched leaving little room for improvement

Should we apply?

People can subscribe for long term only if they want to bet on growth potential

If applying, recommended to sell on getting gains on listing day

One can avoid for investment purposes presently as there are better listed option available in market

Also Read

Home First Finance IPO Crisp Summary

Burger King IPO crisp Summary — Listing with huge gains as shared

UTI AMC IPO crisp Summary — Listed with loss as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Angel Broking IPO crisp summary –Listed with loss as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Also Read : Indigo Paints IPO

Weekend HookUp: 22nd January, 2021

Gold from waste; Bitcoin Myths; Coffee; Founders to Funders

Gold from Waste: Antony waste Handling (Fortuneindia)

Bitcoin: Myths (ArkInvest)

Learning: Curious case of Coffee (LiveHistory)

Founders to Funders: Startups (Forbes)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer : This is not a BUY/SELL/HOLD recommendation. Only for educational purposes. Please consult your financial adviser for investment purposes

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

IRFC IPO– Incorporated in 1986 by the Ministry of Railways (MoR), the Government of India, Indian Railway Finance Corporation (IRFC) is a wholly-owned public-sector undertaking

Business — Its engaged in the activity of mobilising funds on behalf of the Indian Railways to finance its procurement of locomotives, passenger coaches, and wagons as well as to fund other railway infrastructure assets. Apart from providing finance to the MoR, IRFC has provided loans to Rail Vikas Nigam Limited (RVNL), which is wholly owned by the MoR.

Offer purpose — Offer for sale (4600cr) including fresh issue of 3100 cr. for expansion and general purposes,1500 cr will flow to Goverment

Key Service domains – NBFC -Infrastructure finance to MoR

Risks —

Low RoE, lending to government entities at the fixed spread,

and risk of equity dilution from OFS in subsequent years

Strength

Zero NPAs, Lowest Borrowing cost (AAA rated), high operationally managed entity

Strategic role in financing growth of Indian Railways with regular demand for loans which is favorable for its asset growth.

Competitive cost of borrowings: Because IRFC belongs to GoI, and lends to GoI owned entities, the cost of borrowing is very low for IRFC.

Consistent financial performance and cost-plus model: IRFC charges a fixed interest rate for sourcing loans for MoR. It gets fixed spread in the range of 0.3% to 0.4% above its cost of borrowings.

Future

IRFC is strategically important to the MoR as it raises around 25-35% of the total funding requirement (plan outlay) of the Ministry.

It is growing at good rate but ROE can’t be expanded much.

Could be a consistent dividend player

Valuations

Profit making company with stable below par ROE

AUM growth (3yr CAGR>20%) coming at 1x H1FY21 P/BV, Valuations are underpriced to reasonable range of P/B ~1

Should we apply?

People can subscribe looking at mid term to long term prospects

Avoid if one is averse to PSU or looking at big gains

Stellar gains at IPO may not be visible due to large IPO size

One can wait to enter at low prices for investment purposes for dividend play as well

Also Read

Indigo Paints IPO crisp Summary — Apply or not

Burger King IPO crisp Summary — Listing with huge gains as shared

UTI AMC IPO crisp Summary — Listed with loss as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Angel Broking IPO crisp summary –Listed with loss as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Indigo Paints IPO– Among top 5 in Decorative Paint Industry in India with growing over 40% CAGR in terms of sales since inception.

Business — In the Decorative paints industry with high share of differentiated products with high barriers of entry,

~28% business comes from differentiated products

Offer purpose — Offer for sale (1169cr) including fresh issue of 300 cr. for expansion and general purposes

Key Service domains – Repainting constitutes >70% demand and Tier 2, Tier 3, Tier 4 regions are major targets for company

Risks —

Consistently need to spend on Ads to remain in limelight. Currently they spend 12-13% of revenue on ad spends as compared to 3-5% for other big players

As they are expanding to big cities, competition from other 4 large players will pose serious challenge as retail outlets space is limited

Strength

Paint Industry has relatively high entry barriers and need a technologically advanced Manufacturing and distribution network

Company provides low discount on gross sales due to differentiated products

Have low operating expenses as compared to peers and high margins which sustain higher ad spends

Manufacturing locations are close to raw materials keeping costs low

Future

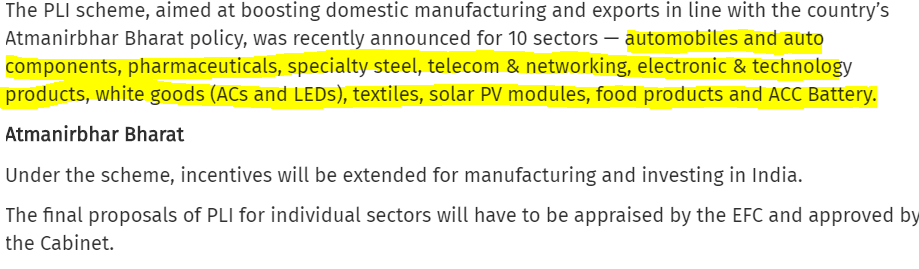

Various government initiatives such as housing for all, smart-cities, industrial corridors and Atmanirbhar Bharat amongst others are likely to offer exciting growth opportunities in the coming years.

As per capita income increases in India, re-painting cycles will be shortened possibly to 5-6 years. Also that will help people to upgrade to premium paints

GST, COVID-19 has shifted the paint market towards organised one and that will help this company in coming years

Valuations

Profit making company with improving ROE, ROCE but seeking very high valuations in IPO (~140X PE)

Asian Paints At 9X Capacity, 500 bps higher margin at 32X Higher Sales than Indigo currently trades at 70X FY22e

Should we apply?

People can subscribe looking at IPO frenzy and possible listing gains only

Recommended to sell if getting 10-30% gains on listing day

One can wait to enter at low prices for investment purposes and review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

UTI AMC IPO crisp Summary — Listed with loss as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Angel Broking IPO crisp summary –Listed with loss as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

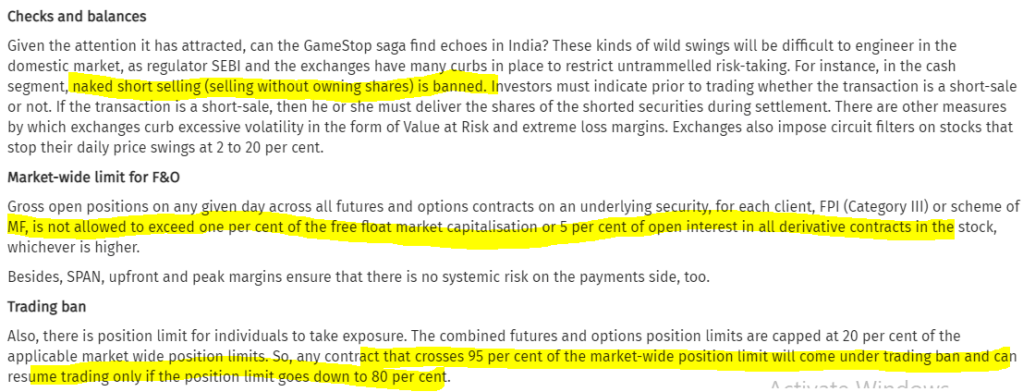

A Decision which can have far reaching consequences for NSE, BSE, CDSL, NSDL

Out of these BSE and CDSL are listed on stock exchanges

More Details and discussion paper attached here ( from SEBI)

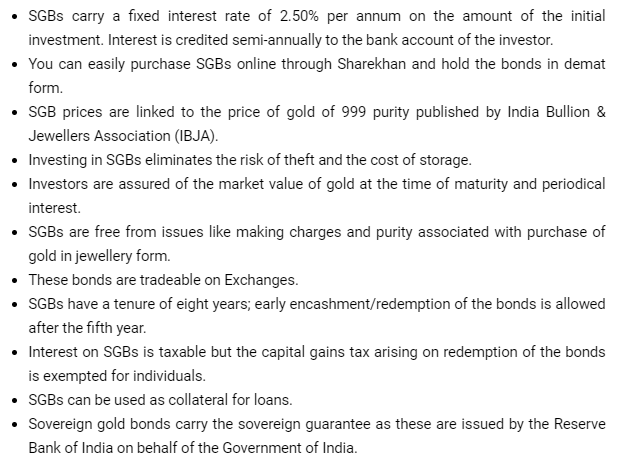

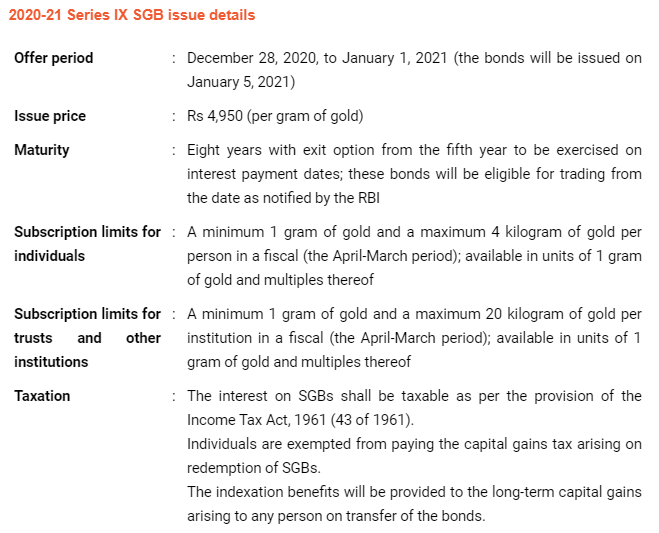

SGBs are government securities denominated in grams of gold.

These are substitutes for holding physical gold.

SGBs are issued by the central bank on behalf of the Government of India.

Investors have to pay the issue price in cash and the bonds are redeemed in cash on maturity.

There are many reasons for buying gold.

The yellow metal acts as a hedge against inflation.

It is a relatively stable investment compared to equities.

It is a good diversification strategy.

It can be purchased easily

Read more for these IPO before listing on their business, strength, risks Bector Food , Happiest minds, Route mobile, Rossari biotech, Burger king

Weekend HookUp: 18th December, 2020

Parenting; Startups; Electric Vehicles; Learning Kindle

Parenting: Raising Intelligent kids with resilient brains (CNBC)

Startups: Agritech Startups (Forbes)

Kindle: How it is like it is (TechCrunch)

Electric Vehicles: Solid state battery (Nikkie Asia)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Read more here on Route Mobile

Read more here on Burger King

Read more here on boAT

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Among Top 5 car makers, Kia Motors and Tata motors gain market share and other have lost. After quite some time, Maruti’s Market share dropped below 50% mark

Retail investors often take their investment decisions based on the share price instead of the fundamentals. They tend to buy what looks ‘cheap’ and get influenced by the news around a company. They often see a large fall in share price as an opportunity. However, such investments often end up becoming value traps. A huge price decline may not always be due to a temporary issue but also due to a permanent dent in the company’s prospects. Also, a sudden surge in the stock price attracts retail investors. They then invest in such a company, without paying much attention to its fundamentals. Curiously, the lower the ticket size of the share, the more interested retail investors become. All these are wrong reasons to buy a stock. A stock should be bought because the fundamentals of the underlying company are robust. Tracking the activity of promoters, FIIs and DIIs can be a useful input in determining this.

-source Valueresearchonline

TEXT HERE FOR EASY reading

On 5/29/13 (my birthday!), I filed to incorporate Palo Alto Delivery Inc., later renamed DoorDash Inc.

It's mostly not my story to tell. But I'll share a bit today about how it started.

My goal is to give aspiring entrepreneurs a window into one founding story.

You'll hear people say the team was obviously impressive, or they had conviction in the vision, but we were not special, it was not a hot space, and no one thought it made sense at first. Starting from the belief that we had to "earn every inch," as Tony often said, was integral.

Tony and I had discussed ideas for awhile without much progress. During our second year in b school, we wanted to build something. I met Stanley in a class and asked if he wanted to work together. He brought in Andy, and the four of us met up.

We came together without an idea, but a shared desire to build something we'd be proud of, and a common interest in serving small businesses.

We went door to door and asked business owners to tell us about their work. The most useful question, for me, was "tell me everything you've done since getting here today."

We tried a few things. One of them was a short marketing attribution survey placed on ipads at retail point of sale. We realized that a surprising % of people would answer 1 question while waiting for their card to process. It was a nice-to-have, not obviously compelling.

Delivery first came up at a macaroon shop. We were wrapping up an interview when we overheard the manager turn down a delivery order. If there was a lightbulb moment, this was it – why couldn't businesses send things across town, on-demand? There should be an on-demand Fedex!

Then we found that restaurants had a more acute pain point. Most didn't deliver, and the few that did HATED doing it. It made no sense for a restaurant to have its own delivery people when they could have 5 orders one day, 20 the next – a pooled resource would obviously be better

So we thought we could build "delivery as a service." Businesses would feed us their orders and we'd deliver them. With our pooled service, all the restaurants in the 'burbs could now deliver!

But immediately we saw it'd be hard to get restaurants to change their behavior.

The most important hypothesis, for this to work, was that excess consumer demand existed. We'd also have to prove out the labor economics for delivery, and that restaurants would be open to delivery. But consumer demand was clearly the driver that would convince restaurants.

So we tested just the consumer part first. We made a static html page at http://paloaltodelivery.com with a google voice number and a few PDF menus from local restaurants, offering delivery for $6. We launched a small adwords campaign to see if anyone was searching for it.

Hours later, Tony and I were driving home when we got the first order. I grabbed a notebook and wrote down what the guy wanted from a local Thai restaurant. We placed a takeout order, drove to the restaurant, bought the food, took it to the customer and charged him with Square.

We kept the experiment going. We sent the link to some Stanford students. We were open a few hours per day, around dinner, and we took turns answering the phone and driving to deliver. We used Find My Friends to see each others' locations and dispatched orders via text.

We quickly had trouble keeping up. I remember running out of class to answer the phone more than a few times. We started hiring others to help us deliver, from craigslist, flyers, and by ordering pizza and hiring that driver on the spot.

I'd start my day by taking out cash from the bank. I'd go to multiple Safeways and buy the max allowed number of Green Dot cash cards, give them to drivers to pay for food, then I'd dispatch and drive, collecting the cards at the end of the day and pay drivers in cash.

We probably took "do things that don't scale" too far. It was absurd. But there was a major upside to doing so many orders ourselves: we understand the details:

The best alley parking spot for each restaurant, which expeditor at Orens Hummus forgets the hot sauce, how to deliver to large apartment complexes, what happens when you lose cell signal in Los Altos, how a hangry parent looks at you when her order is late … every detail.

We knew the unit economics weren't terrible because somehow as we were doing this, the bank account wasn't going down. (It was still running out of my personal account. What an irony that while at Stanford b school we didn't know the first thing about starting a business)

Soon, the conversation with restaurants totally changed. "I see you here all the time — why are you buying so much food? How can we work together?"

Our first restaurant partner showed us how they receive orders from GrubHub via fax and asked us to do the same. I was excited to have a programmatic way to send orders, and then noticed one more thing — GrubHub took a huge commission!

GrubHub didn't even do the deliveries, they just forward orders, so if we were doing both, surely we could generate a similar commission.

That restaurant delivery was such a large opportunity was counterintuitive even to us. There were many (crummy) local services around. But at this point the latent demand for restaurant delivery was slapping us in the face.

A few months in, we explicitly decided to reset our lives, move in together, and devote 24/7 to building DoorDash. After YC, we made the same commitment again. A business like this doesn't get built without sacrifice. I can only imagine what it's been like to do this for 6 years.

Our friends were like “oh interesting” in a way that we knew actually meant “this is weird why are you delivering food.” But it's fun to have discovered a secret. We had more than enough evidence to endure being misunderstood for awhile.

There was another startup that launched the same week in the same town with the same model. They spread lies about us to restaurants and tried to poach our drivers. They met our eventual seed investors before we did.

We ignored them. We stayed focused on delighting customers, merchants, and drivers. That company is long dead.

We were maniacal about growth – 10% weekly. We wrote down on a whiteboard the number of orders we needed per day to hit that target, and the result at the end of the day. We made a simple order counter that we could obsessively check from our phones while we were out driving.

One of our most memorable lessons from YC was "do all the things." We came with a list of 20 ideas for how to grow, and asked the YC partners which to prioritize. I think it was @paultoo who said something like "How would I know? Do all the things."

There was no shortcut. We had to do everything, fast and well, and double down on what worked. (Later I'll write down how this became a simple growth framework I've used since)

We did everything to grow — from standing on the street talking up strangers, going to a birthing convention to figure out how to reach new parents, competing on who could hang more door hanger flyers in a day… most of it didn't work but some did.

We worked out of a few houses, and at one point had about 15 people working from a two bedroom apartment. We liked the cozy vibe, especially since we were there all of our waking hours, and some of us slept there.

When one of our first employees arrived for her first day, Tony was sleeping on the floor of the apartment. I tried to quickly deflate and hide the air mattress while he distracted her out front. We wanted to seem like a real company. I'm sure we did not.

I'll stop for now and make a couple points. (there is no climax, sorry, this is just a tiny window into the very beginning)

We would never have come up with this idea in a conference room on a whiteboard. We needed to be with customers trying things out, learning until we found a set of insights that were obvious only in retrospect.

The idea of a prototype is not mutually exclusive from pursuing product excellence. We rapidly found insights, and then built a business on them, with a clear definition of quality for our customers and relentless pursuit of it.

We never slapped the Uber model onto delivery. We solved our problem from first principles. I won’t explain it but we were able to be far more efficient than our competitors even before our series A, just from smartly solving for an on-demand model with three sides.

The qualities that make DoorDash effective at execution are outlined in the S-1, under "how we operate." It's a great distillation of the culture.

https://www.sec.gov/Archives/edgar/data/1792789/000119312520292381/d752207ds1.htm

Even today, I can recognize people who worked at DoorDash by their intensity. Founders like @ryanbroderick and @therealmikechen are carrying it forward and building more great companies. I'm sure more will follow.

Originally tweeted by Evan Charles Moore (@evancharles) on December 10, 2020.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Bector Food Specialities IPO– Mrs. Bector’s Food is one of the leading companies in the premium and mid-premium biscuits segment and the premium bakery segment. Company is largest supplier of buns for QSR restaurants in India.

Business — Sells Biscuits, Bakery products, Frozen Products. And a contract Manufacturer for Oreo and Bournvita biscuits

Offer purpose — Offer for sale (540cr) including fresh issue of 40 cr. for expansion and general purposes

Key Service domains – Biscuits domestic 43% of total sales, 24% exports of total sales.

Key export regions are Africa and North America. Total 64 countries where export is done

Risks —

There are cases of non-compliance against certain legislations in the past by group company and some disciplinary actions as well

Highly competitive industry with company having only 1% market share. Margins can reman depressed for quite long time putting strain on cash flows

Low shelf life of certain products

Company do not have any long term supply agreements with any of their QSR customers is a strange thing and deals on day to day basis requirement for bns, bakery and frozen products

One of the lowest risk but having high business impact is focus on nutritional value of products which can hamper sales in future

Strength

A leader in biscuits and bakery segments in North India with well-diversified product portfolio.

Major food certifications i.e. BRC, USFDA, and FSSC.

Modern production process, Strong sales and distribution network.

Strategically located in proximity to target markets which minimizes freight and logistics related expense and time

Future

QSR is thriving industry and consumption food business will gain. QSR CAGR expected to grow >20% for next 4-5 yrs

Proxy play to QSR story, so should do well in coming years

Valuations

Profit making company but PAT going down from last three years

Focusing on growth in premium biscuits and bakery segment to improve margin having high competition

As compared to peers, valuations looks ok but needs consistent review

Should we apply?

People can subscribe looking at growth prospects

Listing day may see good gains. Recommended to sell if getting 10-30% gains on listing day

One can also hold long and review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Possible Listing with gain on cards

UTI AMC IPO crisp Summary — Listing with loss as shared

CAMS IPO crisp summary — Listing with 20% gains as shared

Angel Broking IPO crisp summary –Listing with loss as shared

Happiest Minds IPO crisp summary –Listing with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Implementation of production-linked incentive (PLI) schemes worth up to ₹1.45 lakh crore for 10 key sectors announced recently by the government is likely soon.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

If you have not read my earlier post , please go through What to do in stock market in early 2020. It’s important as you will be able to relate to this post in much better way after that!

Most of the investors I talk nowadays are not willing to invest in this supposedly overheated Indian stock market and its not about only December 2020, i can see the fear of crash looming in their talk from Sep2020. Most of them have cashed out from market in September 2020 due to Indian Chinese troop clashes and fear of US election results. What happened thereafter is more painful for such investors, Markets ran away further leaving them behind.

Also read : Invest in Stock market IF

We can broadly classify investors in Dec2020 in three kinds

So as you are reading this article, did you notice where do you belong?

Congratulations, if you are able to see yourself amongst one of the three kinds mentioned above

Question still remains same for everyone : What to do now? Should we buy, sell or keep holding? What’s next : Is it bull market or is crash near?

Let’s read further to understand more about it and see what strategies people can adopt

Thsi strategy is for people who

Advantage with these strategy is you may not lose capital if market goes down and may get a chance to re-enter at lower levels. Problem with this strategy is it is impossible for anyone to predict whether market has topped out or not. Will Market go further up and can give you a bigger chance to cash out? Will market come down and give you a chance to enter at lower levels. Nobody knows. Get away from people if they claim to know.

It is always better to leave last 10% on the table and cash out if our goals are near or we have debt to pay because when correction happens, it will not give you a chance to exit at your desired levels

You may need to decide a market point where you should re-enter

I will strongly advised against this. Problem with this strategy is most of us will be invested in 50 + stocks by taking tips from random sources and keeping most of the stocks which are in loss. So if market correction happens, we will not be having enough money to average down all stocks.

In case, you have idle money and have a itch to invest at these levels, in such cases adopt a simple strategy

Correct portfolio allocation and conviction in the chosen stocks is a must for investing at these levels

This strategy is for people

Under this strategy, adopt the simple course of action

What i am doing in this market? My answer is Case 3.

So that effectively means

I am not putting new money into the market

I am selling my existing less convincing or loss making positions

I am adding more of existing convincing positions

I am adding new stocks position partially and waiting for small correction in market to add more

I am re-organizing my portfolio for next cycle of market

I am keeping Cash levels close to 20% to handle market correction and adding more.

I am happy to ride with my 80% invested convincing positions

I would not recommend to sell out and sit if you have not borrowed money and are not facing immediate liquidity issues. But for sure remove dud stocks and put that money into other quality stocks as always

Overall, what I learnt from markets in my journey is very simple and easy to follow :

You can’t be 100% invested in market

You can’t be 100% sold out from market.

Whenever I tried to cash out in fear, I lost major gains in next cycle. Whenever I invested fully 100% in greed, I lost good amount of capital and recovery becomes difficult.

Holding and adding to convincing positions seems simple but definitely a task which is not easy

So is this a bullish market — i dont know and neither i want to know as i am working on stock specific action

Will correction happen–The more we go away from March 2020 lockdowns, greater will be the chances of economic recovery and lesser are the chances of crash. Healthy Market correction (upto 15-20%) can still happen and can give a nice entry point. Not sure of whether it will happen next week, next month or next year or not at all!!

Whatever strategy finally you adopt. don’t be a blind follower

Read more on Blind follower here

Wishing you all the best and lots of luck

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

In recent years, there is strong inclination see in investors for investing in US stocks. Of course there is a reasoning behind it. Let’s try to figure out WHY and HOW part of it

To understand this let’s understand the returns by DOW and BSE in last 10 years

US market consistently outperformed Indian market in last 10 years. Although there is no guarantee that it will happen in next 10 yrs again

So outperformance of US markets along with Indian currency depreciation widens this performance gap further and this makes a strong case for investments in foreign stocks

Buying foreign stocks allows investors to

As a thumb rule for starters, a 5% to 10% exposure to foreign stocks for conservative investors, and up to 10-25% for aggressive investors seems ok

Individual investors can invest up to $250,000 every year overseas under the RBI’s Liberalised Remittance Scheme. After opening an overseas brokerage account, investors will be needed to fund it by remitting money from his/her bank account

Now let us understand the 2nd part of it

Open a low-cost international broking account and invest in low-cost international exchange-tradedfunds

Let’s also understand the precaution or risks to be taken care of

When you invest in the US stock market, , please be aware of taxation part

Dividends will be taxed in the US at a flat rate of 25%. Due to Double Taxation Avoidance Agreement (DTAA), taxpayers can offset income tax already paid in the US (Foreign Tax Credit)

Disclaimer : The article is written to provide information and make investors aware of potential avenues of investment. Please don’t treat this as an investment advice. There could be change in tax laws from time to time and one should track it before investing. Past performance of any index returns can not and should not be taken as reference for future performance. Percentage allocation for each investor can vary and its best to consult to one ‘s own financial advisor before making investment decisions. We don’t have any mutual agreement with the sources or apps shared for investment and we dont gain/loss from your action in this regard

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 29th November, 2020

Cycling; Optimism; Electric Vehicles; Investing and Learning

Cycling: Benefits (Cycling weekly)

Optimism: Good things taken too far (CollaborativeFund)

Learning: Bargain Hunter’s Dilemma (Ritholtz)

Electric Vehicles: Big bet but is it enough (Fortuneindia)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Burger King IPO– Company is 2nd largest burger chain in India, started operation in 2014 and fastest international brand to have 200 QSR outlets in Inda

Plan is to target 700 outlets in next 5-6 years.

Offer purpose — Offer for sale (360cr) plus fresh issue of 450 cr. To open new stores and pay some part of loan

Key Service domains – 2nd largest burger chain after McDonald

Risks —

Loss making company as of now. Loss of 119+ cr in six months of current FY21, loss of 76 cr in last year FY20

Offer on food tech apps may harm the business wrt competitors plus McDonald, Jubilant food will definitely try to defend the market share

Fast expansion may lead to more losses in coming years but its a double edged sword and can lead to gains as well

Strength

Post COVID –company will have lean structure and business should have good unit economics

Also because of urban developments and more money in hands to spend, culture of eating in QSR will support the company

Fast expansion can help the company in increasing mkt share

Future

QSR is thriving industry and consumption food business will gain. QSR CAGR expected to grow >20% for next 4-5 yrs

Sustainability looks good, McDonald, Dominos, Subway, KFC have already survived and adapted

Valuations

Loss making company and PE is negative

Last 3 Yr Revenue CAGR at 53.4%; Total Debt as of Sep 2020 at 195 Cr

As compared to peers , valuations are reasonable in terms of mcap/sales or mcap/ebitda

Should we apply?

People can subscribe looking at growth prospects

Listing day may see good gains. Recommended to hold long

If available on listing day around 50-70 Rs, one should add more from 3-5 yrs perspective for possibly good gains

Also Read

UTI AMC IPO crisp Summary — Listing with loss as shared

CAMS IPO crisp summary — Listing with 20% gains as shared

Angel Broking IPO crisp summary –Listing with loss as shared

Happiest Minds IPO crisp summary –Listing with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Look at the sectors showing positive growth as compared to Oct2019

Coal

Electricity

Fertlisisers

Cement

Economy looks on recovery mode like a pendulum which swings in extremes. Although technically India enters into a recession with two quarters of negative growth but optimistically this can change by Mar2021. Only caveat here is fresh set of lockdowns

On the other hand, crude oil, refinery products and natural gas may remain suppressed as world moves to Work form home (medium term trend)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Weekend HookUp: 22nd November, 2020

<p class="has-text-align-justify" value="<amp-fit-text layout="fixed-height" min-font-size="6" max-font-size="72" height="80">Cycling; Flying; Investing and LearningCycling; Flying; Investing and LearningCycling: Cycling shorts (Velocrush)

Investing: How to invest abroad (Morningstar)

Flying: How spicejet is re-learning to fly (Forbes)

Learning: How to take smart notes (Janav)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Stocks bought by prominent MF in Oct2020

Two indicators showing more recovery in economy

Actual test lies in Dec 2020 collections

Covid -19 has an impact on consumer durables to such an extent that demand outsrips supply and many SKU have waiting periods.

Interestingly Dishwashers demand is so high that it outstrips last few years combined sales already. Listed Companies like Whirlpool, Siemens,, Voltas, IFB can be beneficiary and Voltas and IFB stocks have run up in recent past already

This is a trend which will not stop and will have a contagious effect in Indian Society where word of mouth helps a lot in buying decision.

So premium items like dishwashers may become a common sight in coming days in many Indian households. Look for this trend to unfold in medium term

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Nobel prize winning economist John Nash created the pay off matric for prisoner’s dilemma.

Focusing on Nash equilibrium is important for best desirable outcomes

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

I belong to segment of people who believe that investing in IPO should be avoided unless you understand the company and its future well and also understand the price for which its being offered in IPO. And due to very less information on such companies, chances of going wrong are high.

But 2020 is different. Looking at some prominent IPO which have come in last 12 months, one must have made good money on listing, although holding might have been more painful for many investors

Listing Gains are 30% on an average, which is really good for year 2020 while despite being these stocks tanking after listing gains, diligent people might still be sitting on 10-12% gains for a year ( may be more if compounded annually calculation brought into picture)

Other notable point is most of these IPO are of smaller size relatively leading to oversubscription and listing gains.

Also read : https://alpha-affairs.com/category/ipo/

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

FMEG segment already growing –from earlier posts some indicators showing this already

Despite Fall in revenue in other segments in 1st half FY21

Q2 FY21 results fo SBI cards are out and does not look great on few fronts although long term story seems intact as of now

Few snaps from SBI recent investor presentation where we can see the lagging part from company as compared to previous year FY20

SBI Cards : Declining portfolio growth, SBI Cards : Increasing NPA , SBI Cards : Declining PAT

Looks better to wait for right entry price : NOT a RECOMMENDATION

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

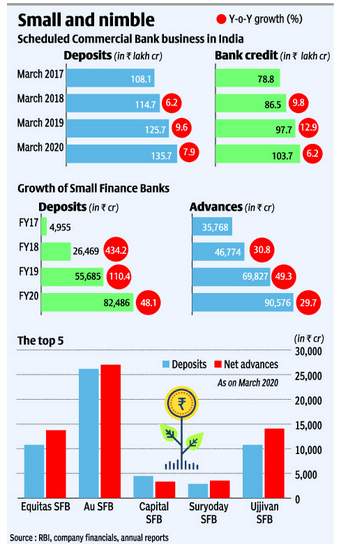

Equitas Small Finance Bank– Equitas Small Finance Bank is the leader among SFBs in terms of the distribution network (With a network of 991 banking outlets across 17 states and union territories in India). Further, it is the second-largest SFB in India in terms of assets under management (AUM) and total deposits in FY19.

Offer purpose — Fresh issue of 280 cr to boost tier 1 capital plus 237 cr offer for sale

Service domains – The SFB’s product offerings include small business loans, housing loans, agriculture loans, vehicle loans and microfinance loans. On the liability side, it offers current accounts, salary accounts, savings accounts and term deposits to its customers. Besides, Equitas SFB also offers a range of third-party products, including insurance, FASTag for toll plazas and mutual fund products.

Strength –

A well-diversified asset portfolio

Large presence- It is a leader among SFBs in terms of the distribution network.

Risks —

Lower return ratio as compared to peers.

Asset Quality is poorer due to loss in vehicle finance segment. Provision coverage ratio is less

Stock will remain in overhang as promoter stake needs to be diluted to 40% in coming years

Fierce competition and concentration of customers in articular region

Future

Small finance banks are expected to grow 25% annually over next few years and IPO is priced at lower valuation compared to peers factoring lower asset quality and provisioning

Large presence and distribution network will help the bank to grow

Valuations

Seems reasonable

Should we apply?

People can avoid to subscribe

Better peers available in same segment for long term growth prospects

Listing day may see not any gains . Recommended to sell on listing day if any gains available

Also Read

UTI AMC IPO crisp Summary –Listed below IPO price

CAMS IPO crisp summary — Listing with gains

Angel Broking IPO crisp summary –Listing Below

Happiest Minds IPO crisp summary –Listing with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Source : Hindu Business Line

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Likhitha Infra– (approx 32 yr old company) is an Oil Gas Pipeline Infrastructure provider in India. Focused on laying pipeline networks, Operation and maintenance of city gas distribution companies in India

Offer purpose — 61 crores to meet working capital requirement

Key Service domains – Cross country pipelines, City gas distributions including CNG stations, Operation and maintenance

Clients -Established players from Oil and Gas industry

Risks —

Major revenue from few clients may deprive the company from pricing power

Inherent risks due to long term nature of projects

Future

CGD is increasing in India and company is at right place for its business to grow with

Strong client base, Efficient business model

Strong project execution capabilities , Diversified geographical presence in India

Valuations

Seems attractive

Should we apply?

People can subscribe for long term growth prospects

Listing day may see gains . Recommended to hold and buy more if listed at IPO price +/-10%

Also Read

CAMS IPO crisp summary — Listing Awaited

Angel Broking IPO crisp summary –Listing Awaited

Happiest Minds IPO crisp summary –Listing with substantial gains

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.