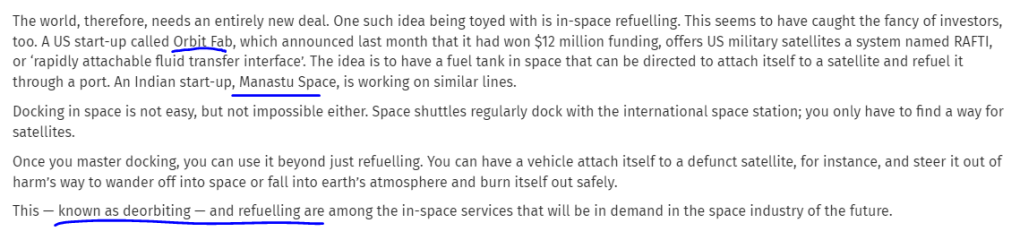

Space Startups

BE FINANCIALLY INDEPENDENT

With great pleasure and best wishes from all of you, we are delighted to launch

ALPHA Mentorship program

ALPHA LEARNERS

Art and Science of Investing

to make you Independent in stock markets

AVAIL EARLY BIRD OFFER till 25th April 2022

A PROGRAM TO MAKE YOU LEARN AND EARN

This is a unique live program for approx. 5 months (on weekends) Where one can learn necessary

Fundamental Qualitative concepts to understand the things which create wealth in long run–like how to evaluate management, how to evaluate certain corporate actions, how to understand direction of company

Fundamental Quantitative concepts to substantiate what we have seen qualitatively, understanding ratios and numbers like margins and numbers like EBITDA, PAT, OPM, Financial Ratio, Valuation ratios PE, PB, PS, EVEBITDA, ROE, ROCE, Debt, equity and many other deep ratios to understand whether stock at right price or not

Learn about cost of capital, working capital cycle, inventory turnover, asset turnover, interest coverage, pledging(good or bad)

Why Dividend is good or bad

How long we can hold a stock or when to leave the stock

Capex, Opex and how it impacts and when it impacts

Why certain high pe stocks keep on running and low pe stocks remain down

Red flags and green flags

Necessary Technical aspect to make our entry and exit better in stocks ,oscillators and indicators including RSI, MACD, STOC RSI, EMA, TEMA, DEMA, Trends, SL

Technical aspect and understanding of Price Volume action, candlestick patterns ( bullish, bearish, single, double, triple patterns)

Technical understanding of Targets from different patterns, How to look for patterns and when to look for which pattern

Resources to analyze faster to analyze more companies faster

Understand Contrarian, Cyclical, Value and Growth investing

Bucket and GRADE Framework

Business Moats understanding–how to categorize moats, what is real moat, what is fake moat

Exit Strategies in stocks

Reading Balances sheet in simple way to analyze results and issues to make quick exits or to do pyramiding after results

Reading Cash flows in simple way to understand where money is being moved in company

Reading Quarterly, half yearly, yearly results and interpreting them better

Tricks and Checklist for faster analysis of Annual Reports to help us all understand whether to deep dive or not

Conf-call understanding, Transcripts Concepts and Tricks to understand faster

Big money moves aspect to understand where money is moving

Concepts and tricks on various intricacies in stock market

Understanding about primary, secondary market

Also get a KNOWHOW on

Checklist for stocks to identify red flags faster

Checklist for deep dive into selected stocks

How to build Portfolio for Short term

How to build Portfolio for Long term

How to find Multi bagger stocks

How to avoid pitfalls in market

When to exit stocks

Concept of Futures and options

4 Bonus sessions (apart from Program content)

Mutual Funds

Financial planning

IPO and

Big money moves

3-4 months of teaching and mentoring

Can be extended based on queries, case studies1-2 months of handholding

To clear doubts, correction of mistakes, independent walking in markets

10+ Assignments

Based on actual events happening in markets during the course

Case studies

Based on future growth understanding and pitfalls to avoid

Quizzes

To help you assess yourself whether you are progressing or not during the programPresenting Stock idea by Learners to bridge the learning gap –this will be an approximate six month effort by all participants

This is a program YOU CAN NOT AFFORD TO MISS

LET THIS NEW YEAR 2022 be the start of your journey towards INDEPENDENCE IN STOCK MARKETS

ACT NOW for your Independence

CONTACT us

AVAIL EARLY BIRD OFFER till 15th April 2022

FEEDBACK By Ongoing ALPHA LEARNERS

ACT NOW for your Independence

FEEDBACK By Ongoing ALPHA LEARNERS

CONTACT us

Number of batches and batch size is very very limited considering live classes

Major part of this initiative will go towards orphan children education and food

Do make use of this opportunity and be part of bigger initiative

Connect with us to help genuine needy children

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The group’s major acquisitions for retail expansion include Hamleys, Justdial, Milkbasket, Zivame, Portico, Netmeds, Urban Ladder, Dunzo, Shri Kannan Departmental Store, Jaisuryas and Kalanikethan. Recently, it partnered with 7-Eleven, the iconic global retail chain, to start its operations in India. A big deal, which is pending, is the acquisition of Future Group companies for ₹24,700 crore.

Full article here on Fortune

Disclaimer – Below Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Supriya Lifescience Limited got incorporated in the year 2008 and became one of the key Indian manufacturers and the supplier of APIs.

Business —

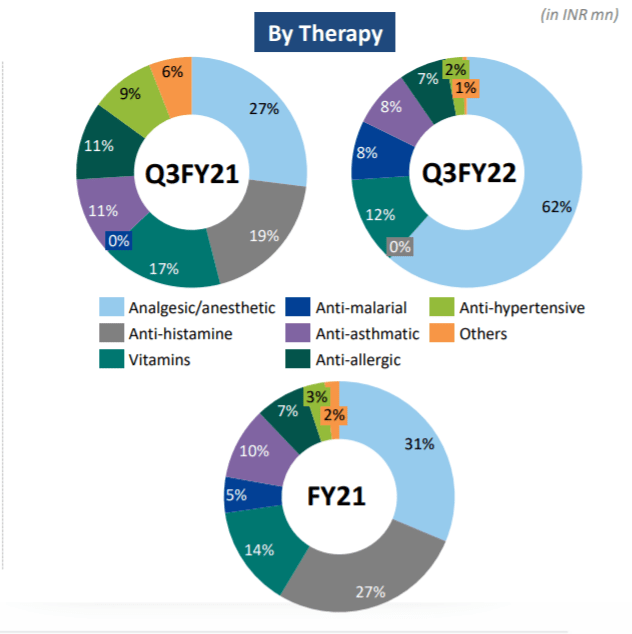

Supriya sells 38 API focused on the diverse therapeutic segments, along with being the largest exporter of Chlorphenamine Maleate, Salbutamol Sulphate, Ketamine Hydrochloride and Esketamine from India.

Supriya Lifescience is a pioneer in segments like antihistamine, analgesic, anesthetic, vitamin and anti-asthmetic and anti-allergic.

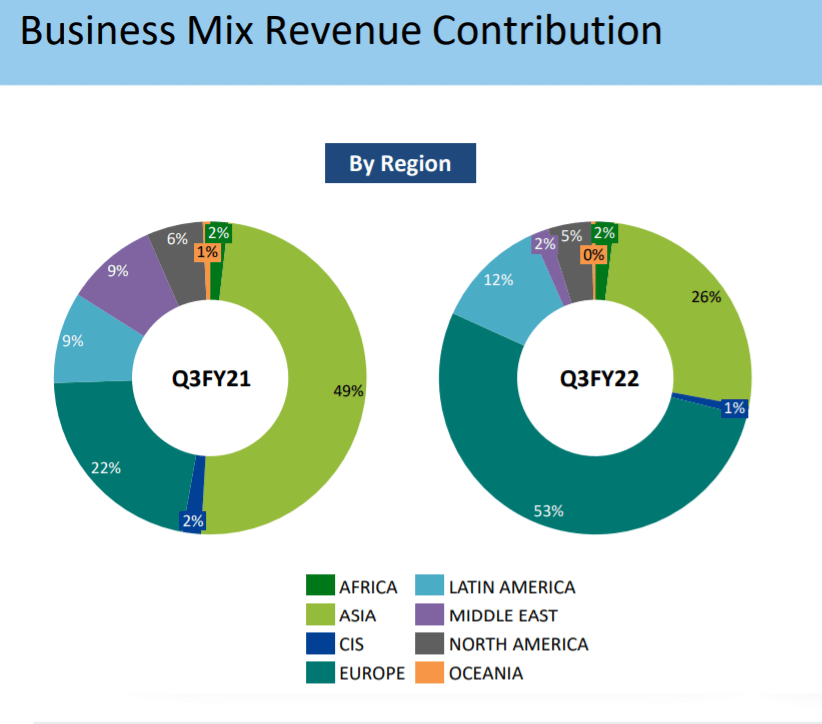

Region of operation—

Company is focused on regulated markets and company is more export oriented with 77% revenues coming from exports

END USER INDUSTRIES — Kind of evergreen and growing industries in coming decade

Moats —

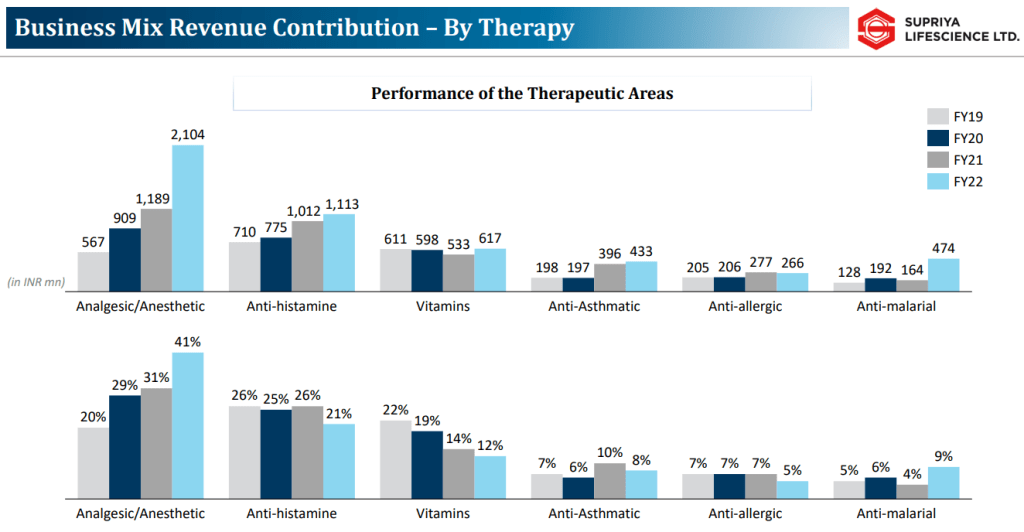

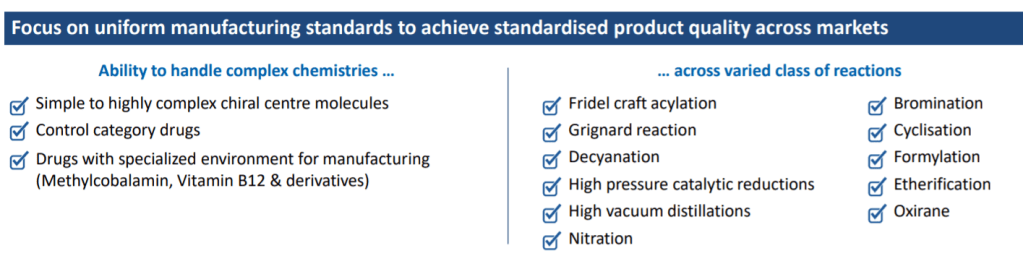

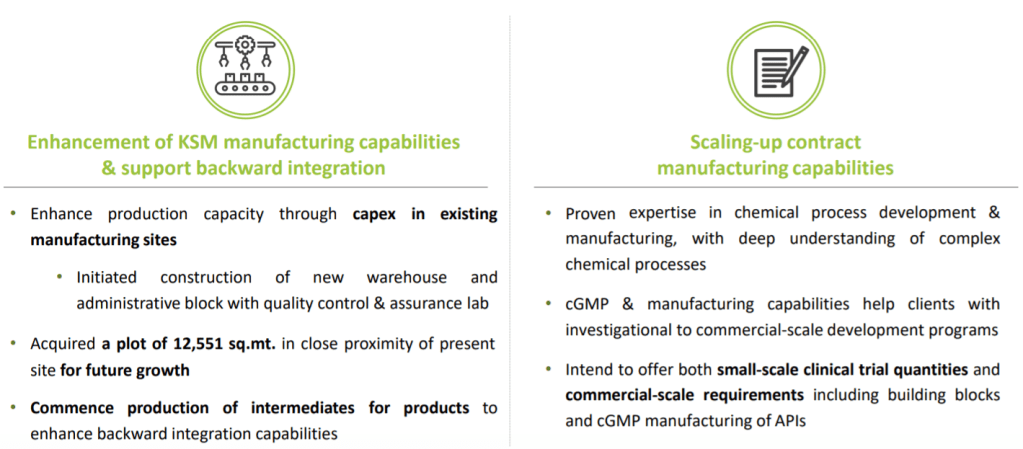

Backward integrated business model with well established presence in the API manufacturing, with focus on high value products with limited competition. Backward integration of top 12 products generating 67% of revenues thus de-risking many issues on supplies, pricing

Niche product basket of 38 APIs across diverse therapeutic segments

Advanced manufacturing and research and development capabilities with ability to handle complex chemistries across varied chain of reactions

Strengths

Pioneer in segments like antihistamine, analgesic, anesthetic, vitamin and anti-asthmetic and anti-allergic and clear leader in top three products having more than 50% share

Diversified export profile –Exports to 86 countries

Global clientele with long standing relationships on the back of consistent product quality & reliability of supply

Diversified therapeutic categories

USFDA, EUDQ, EUGMP, NMPA, CEP grants and approvals in place

Experienced senior management team and qualified operational personnel with new generation started in company already

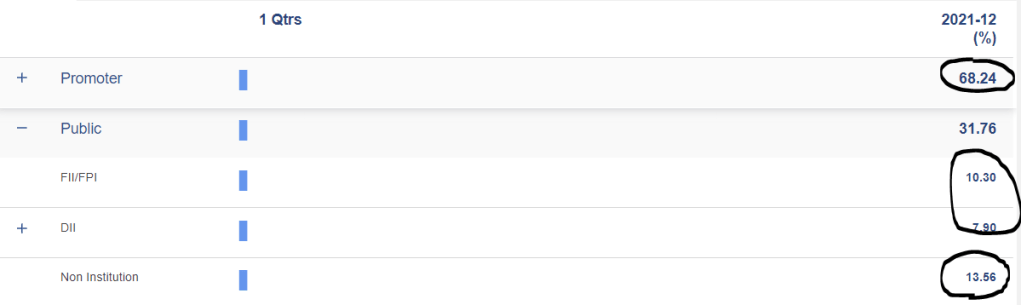

Shareholding

Promoter has sufficient skin in game with holding ~68% and other prominent players in DII/FII holding 18% more leaving only 13-14% to general public

Some triggers and updates from recent Q3Fy22 Concall

Getting portfolio derisked and adding more categories which are complementing existing therapies

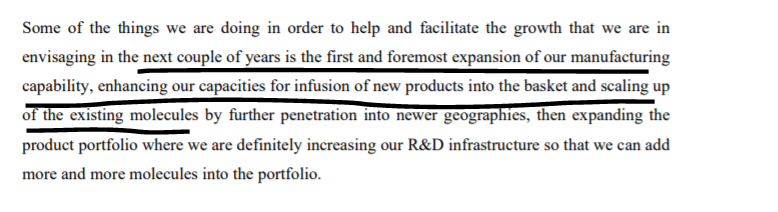

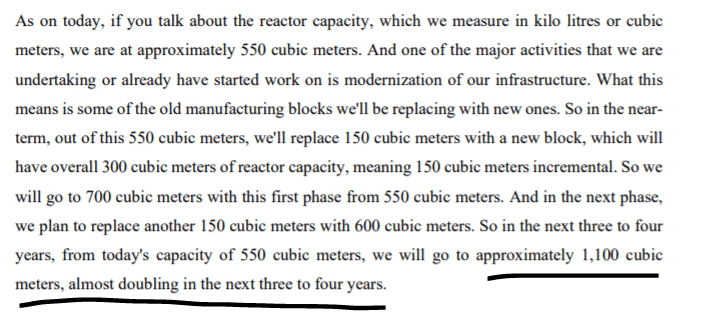

Expansion of manufacturing capability and capacity, scaling of existing molecules and addition of new products

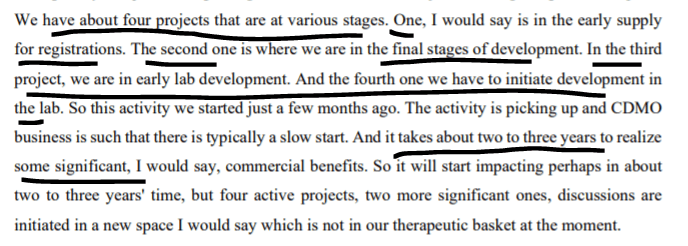

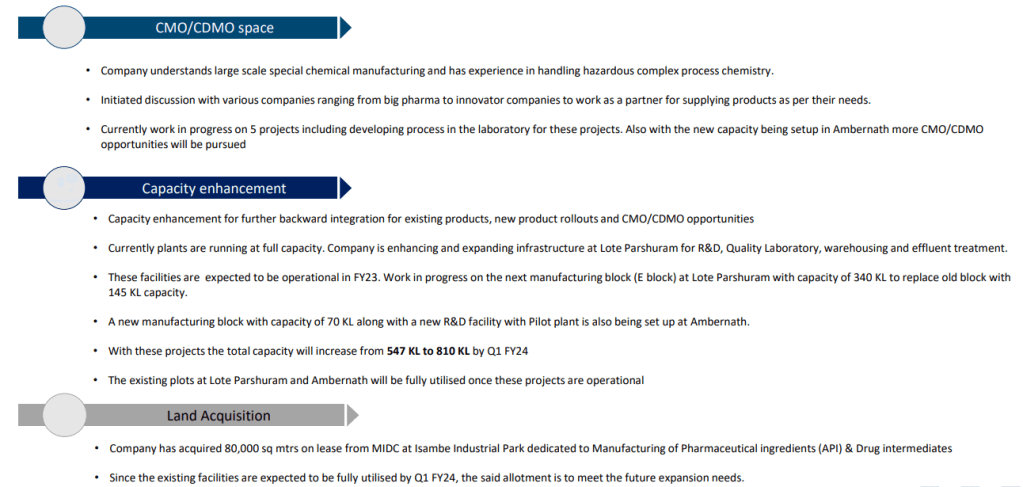

Entering CDMO space

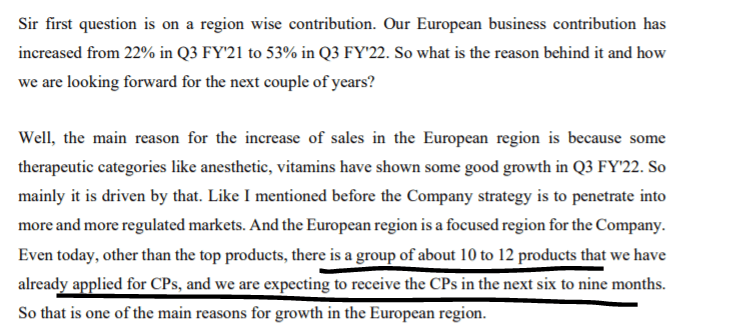

Growth in European region

Q4FY22 inputs from company

Company earnings are quarter dependent with some quarters showing better growth than other quarters, it will take company few years to balance this up and down quarters with new products filling up

Export oriented risks ( freight risks, currency risks, geographical risks)

Risks associated with pharma companies on USFDA etc. kind of approvals

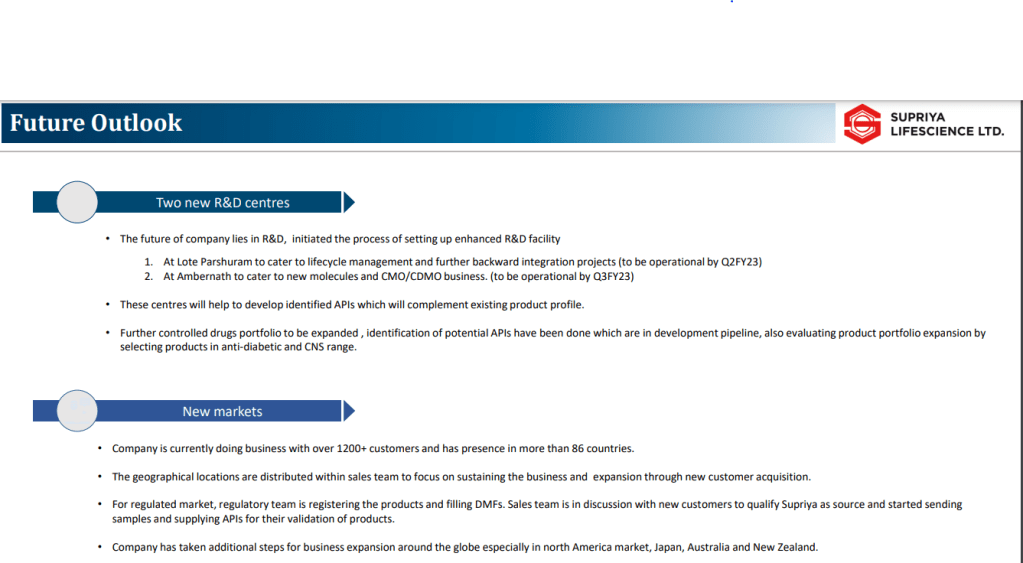

Any delay in CMO, CDMO projects ramp up which is expected by Q2FY24 (Aug-Sep 2023)

Any delay in ramping up Amber Nath facility (expected Dec2022)

Any sell off by FII/DII can lead to quick price erosion

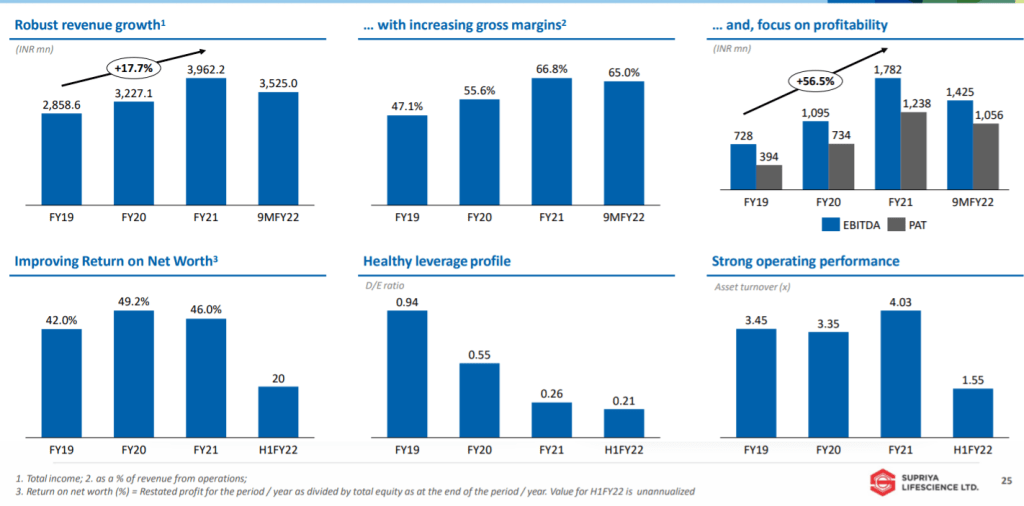

Company is showing Good revenue growth with increasing Gross margins and reducing Debt to equity profile

Current valuation look to factor in immediate growth for 1-2 quarters but if we keep our horizon long and vision as shared by company, then valuations seems reasonable (estimated PE of 16-19 Q1FY23E with CMP 386). Increasing capacity utilization and profitability can lead to rerating of company

Your strategy can be different than mine. Your selection of company might be different than mine. So lets not be a BLIND FOLLOWER

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Below Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

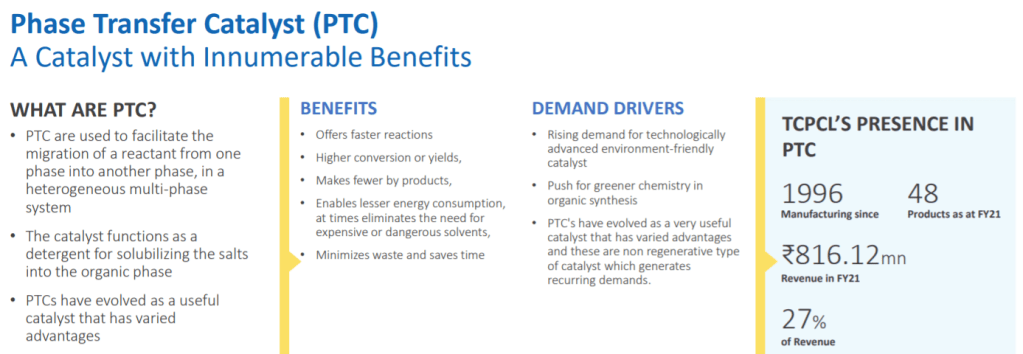

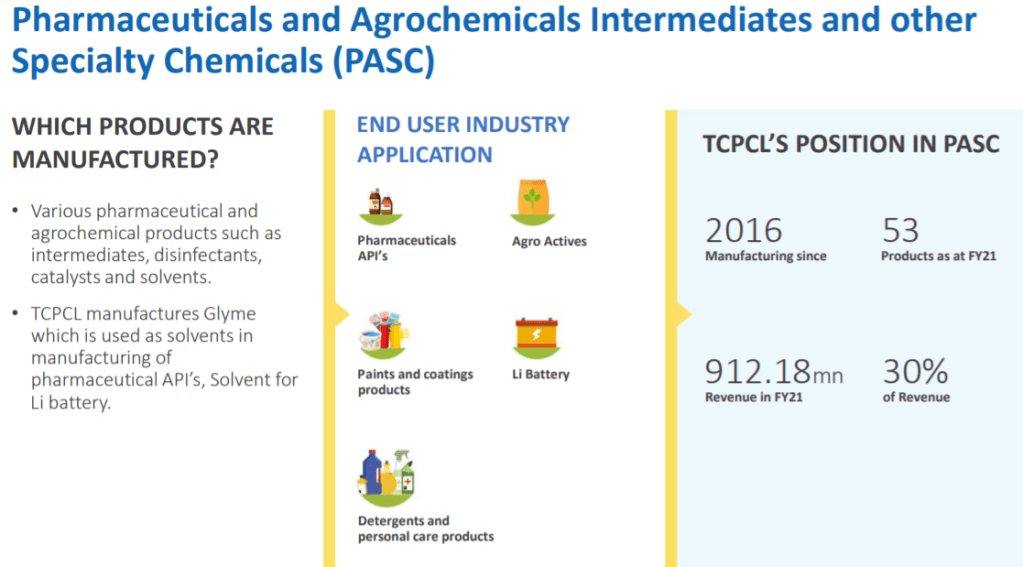

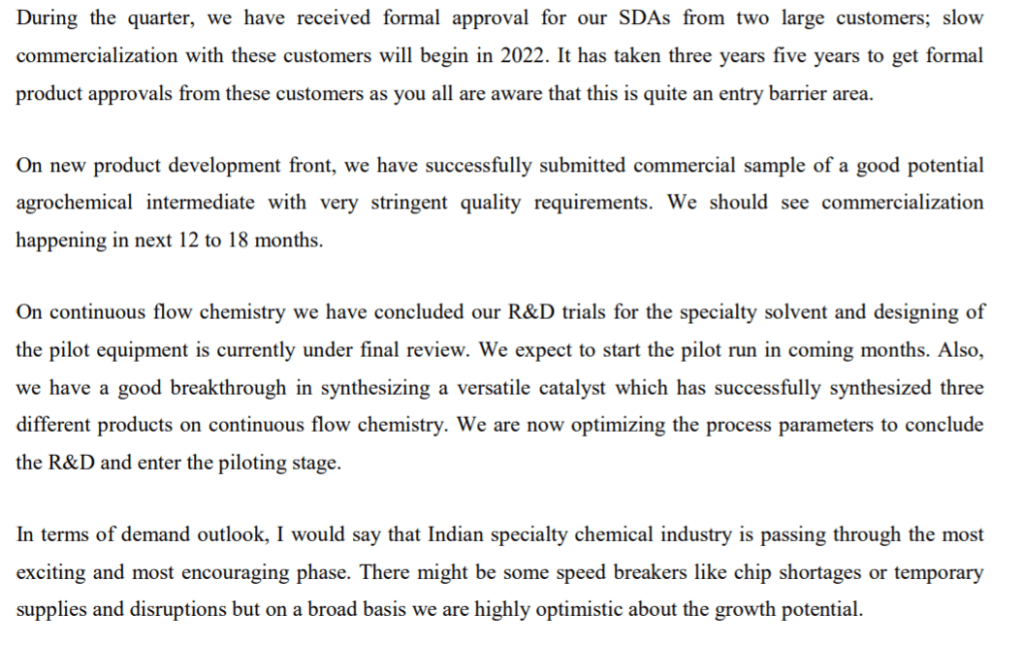

Incorporated in 1996, Tatva Chintan Pharma Chem Limited is a specialty chemicals manufacturing company. It is engaged in the manufacture of structure directing agents (SDAs), phase transfer catalysts (PTCs), electrolyte salts for super capacitor batteries and pharmaceutical & agrochemical intermediates & other specialty chemicals (PASC).

Business —

One of the leading producers with entire range of PTCs in India and one of the key producers across the globe

2nd largest manufacturer of SDAs for Zeolites globally and the largest commercial supplier in India

TCPCL is the largest producer of Glymes in India and third largest in the world.

Largest producer of electrolyte salts for super capacitor batteries in India

END USER INDUSTRIES — Growing industries in coming decade

Moats —

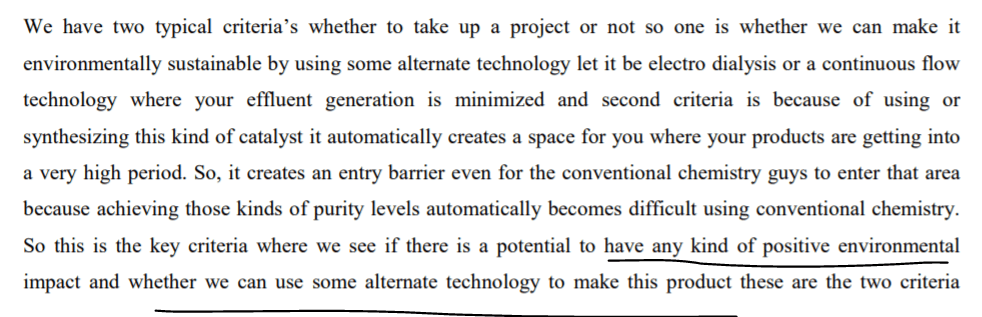

TCPCL is one of the few companies globally that uses Electrolysis process in organic synthesis. Advanced chemistries in process and for commercial development, manufacture and approvals, it takes 1-6 years for new players to enter this field.

In many of the segments, it is amongst top five players

Strengths

Considering the wide range of applications of our products, TCPCL can cater to customers across wide spectrum of Chemical Industries

which ensures a sustainable business model.

Diversified product portfolio has helped accelerate growth and in innovating and thus retain both new and existing customers

Diversified esteemed clientele

Necessary certifications in place : ISO 9001:2015 ISO 14001:2015 BS OHSAS 18001:2007

Advantages of Electrolyses

Region of operation

The company exports most of its products to over 25 countries, including the US, China, Germany, Japan, South Africa and the UK.

It reduced % revenue dependency on top 10 customers from 60% to 47%

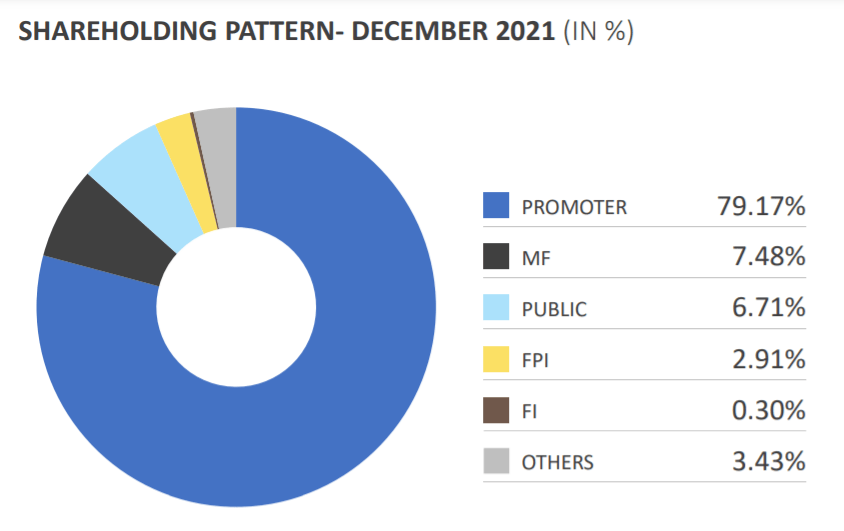

Shareholding

Promoter has sufficient skin in game with holding ~79% and other prominent players holding 10% more

Some triggers and updates from recent Q3Fy22 Concall

Getting approvals from two large customers

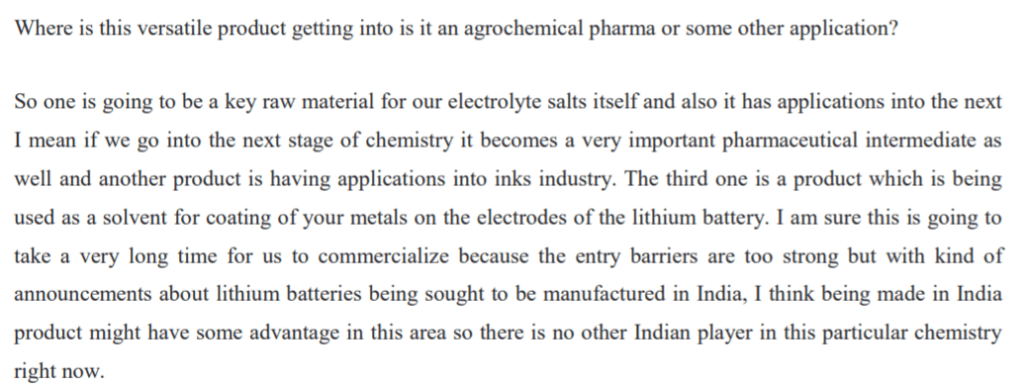

Getting into EV domain with supercapacitor batteries and new horizon opening up faster than anticipated

New versatile product development in Continuous flow chemistry us also capable in other applications including EV

Comfortable Leading market share in almost all operating domains

Mindset of accepting which projects

Delayed expansion –currently scheduled for Nov 22

Delay in semiconductors supplies impacting SDA in FY23 as well (current anticipation is till FY22)

Slow ramp up of electrolyte salts than projected

Approvals for new PASC delayed

Increase in raw material and frieght costs is already impacting margins, further increase will hurt next two quarters badly in terms of margins if it happens ( Q4FY22, Q1FY23)

They have to be seen in terms of huge growth runway available but current valuations don’t give that comfort to take large positions with risks on execution and inflation

Looks better to give time to company and see how it performs and keep accumulating in background in small tranches. That may work.

Your strategy can be different than mine. Your selection of company might be different than mine. So lets not be a BLIND FOLLOWER

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.