Disclaimer – Below Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Tatva Chintan – CMP 2520 (Dated 3-feb-22)

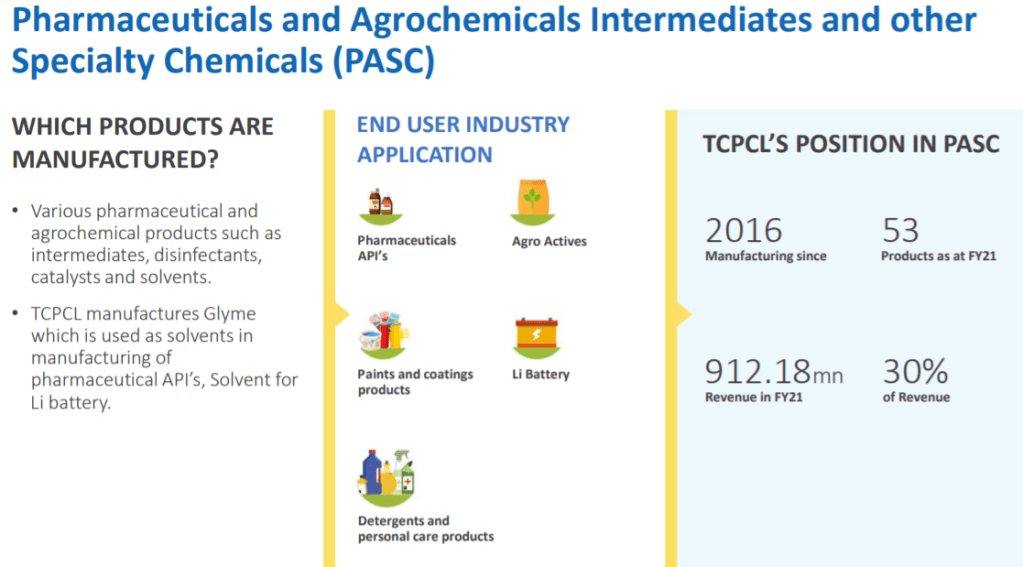

Incorporated in 1996, Tatva Chintan Pharma Chem Limited is a specialty chemicals manufacturing company. It is engaged in the manufacture of structure directing agents (SDAs), phase transfer catalysts (PTCs), electrolyte salts for super capacitor batteries and pharmaceutical & agrochemical intermediates & other specialty chemicals (PASC).

Business —

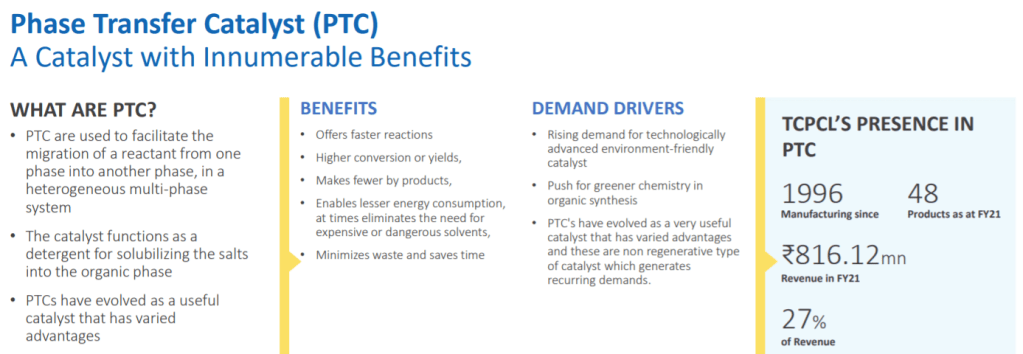

One of the leading producers with entire range of PTCs in India and one of the key producers across the globe

2nd largest manufacturer of SDAs for Zeolites globally and the largest commercial supplier in India

TCPCL is the largest producer of Glymes in India and third largest in the world.

Largest producer of electrolyte salts for super capacitor batteries in India

END USER INDUSTRIES — Growing industries in coming decade

- Pharmaceutical API’s

- Flavors and Fragrances

- Agrochemicals

- Environment Control Processes -NOx removal

- Automotive – Catalytic Converter – Emission Control

- Petrochemicals – Cracking crude

- Automotive Transport & Infrastructure

- Electric Vehicles

- Consumer Electronics

- Renewable Energy

- Grid Balancing

- Paints and coatings products

- Li Battery

- Detergents and personal care products

Moats —

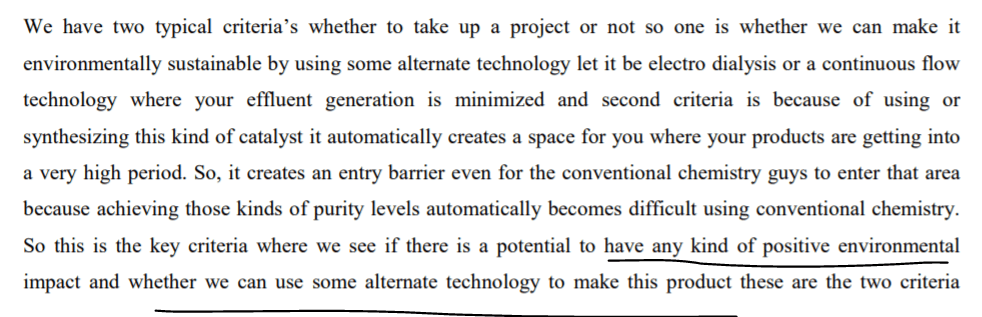

TCPCL is one of the few companies globally that uses Electrolysis process in organic synthesis. Advanced chemistries in process and for commercial development, manufacture and approvals, it takes 1-6 years for new players to enter this field.

In many of the segments, it is amongst top five players

Strengths

Considering the wide range of applications of our products, TCPCL can cater to customers across wide spectrum of Chemical Industries

which ensures a sustainable business model.

Diversified product portfolio has helped accelerate growth and in innovating and thus retain both new and existing customers

Diversified esteemed clientele

Necessary certifications in place : ISO 9001:2015 ISO 14001:2015 BS OHSAS 18001:2007

Advantages of Electrolyses

- Electrolysis is considered as a ‘green’ chemistry process wherein apart from a single starting raw material, the process largely uses only water and electricity

- Since no additional solvents or other chemicals are used, it is a safe chemistry

- It has minimum requirement of auxiliary substances

- The process enables faster output and Higher Purity

- By deploying electrolysis, the products achieve the lowest possible process mass intensity

Region of operation

The company exports most of its products to over 25 countries, including the US, China, Germany, Japan, South Africa and the UK.

It reduced % revenue dependency on top 10 customers from 60% to 47%

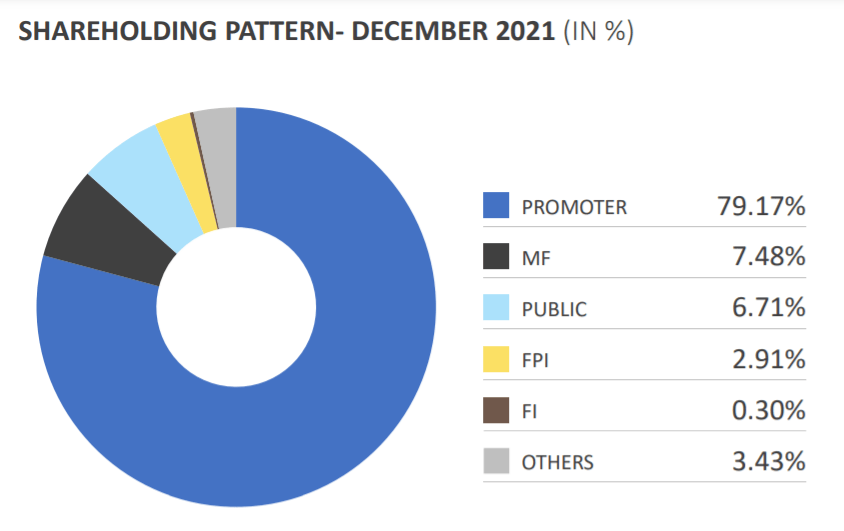

Shareholding

Promoter has sufficient skin in game with holding ~79% and other prominent players holding 10% more

Some triggers and updates from recent Q3Fy22 Concall

Getting approvals from two large customers

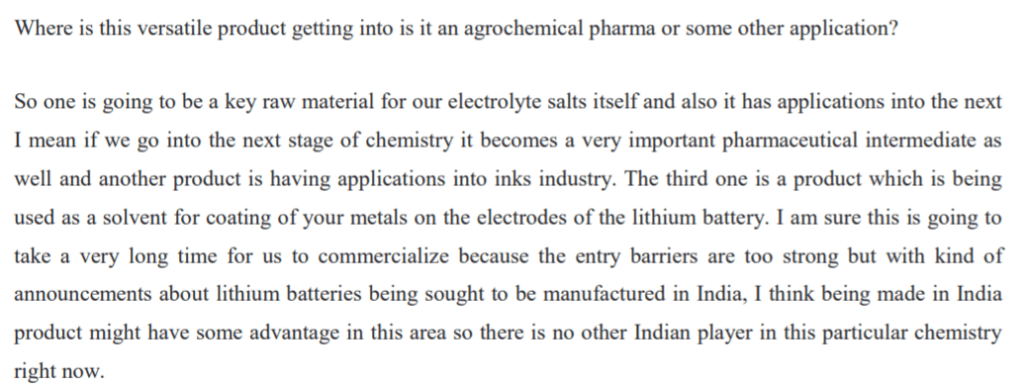

Getting into EV domain with supercapacitor batteries and new horizon opening up faster than anticipated

New versatile product development in Continuous flow chemistry us also capable in other applications including EV

Comfortable Leading market share in almost all operating domains

Mindset of accepting which projects

Risks (tried to see major risks, please do due diligence to understand more on this part)

Delayed expansion –currently scheduled for Nov 22

Delay in semiconductors supplies impacting SDA in FY23 as well (current anticipation is till FY22)

Slow ramp up of electrolyte salts than projected

Approvals for new PASC delayed

Increase in raw material and frieght costs is already impacting margins, further increase will hurt next two quarters badly in terms of margins if it happens ( Q4FY22, Q1FY23)

Valuations —

They have to be seen in terms of huge growth runway available but current valuations don’t give that comfort to take large positions with risks on execution and inflation

Looks better to give time to company and see how it performs and keep accumulating in background in small tranches. That may work.

Your strategy can be different than mine. Your selection of company might be different than mine. So lets not be a BLIND FOLLOWER

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Discover more from ALPHA AFFAIRS

Subscribe to get the latest posts sent to your email.