Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Jupiter Wagons Limited (JWL) is a provider of comprehensive mobility solutions, with diverse offerings across Freight Wagons, Locomotives, Passenger Coaches (LHB), Braking Systems, Metro Coach, Commercial Vehicles, ISO Marine Containers, and products such as Couplers, Draft Gears, Bogies, and CMS Crossings. JWL has manufacturing facilities located in Kolkata, Jamshedpur, Indore, and Jabalpur with full backward integration to its foundry operations.

With a rich legacy over four decades, the Company has leveraged its deep technological capabilities and robust financial position to emerge as a one-stop shop for mobility solutions and reinforce its position as one of the fastest growing within the industry.

Products, Segments

Railway Wagons

Commercial Vehicles incluising Electric Light Commercial Vehicle business (eLCV)

CMS Crossing

Brake Systems & Brake Disc

Containers including Flex Containers, Marine containers , BESS containers

Strengthsand Certifications

The Group has established partnerships with leading global companies such as Tatravagonka (Slovakia), DAKO-CZ (Czech Republic), Kovis Proizvodna (Slovenia), Telleres Alegria S.A (Spain).

Marquee clients associated with company

JWL is one of India’s largest wagon manufacturers, with a capacity of 9,600 wagons per annum

Improving scale of operations

Healthy order book providing revenue visibility

Experienced Management and leadership team

12 World-class manufacturing facilities

3,000+ Workforce

Clients

Catering to industries such as Railways (Freight + Passenger), Metro Rail, Automobile, Transportation, Logistics, Construction Equipment, Municipalities, Healthcare, Energy, Mining and Infrastructure, the Company boasts a marquee client base including the Indian Railways, American Railroads, Indian Ministry of Defense, Tata Motors, GE, Volvo Eicher Motors

Joint Ventures

Fundamental Ratios, Cash, Loans, EBITDA,PAT margin, Shareholding pattern

Consistent increase in sales over last 12 qtrs barring a quarter or so Profits have multiplies by 8x in last 2 years

Consistent Tax records

ROCE and ROE is reasonably above 20%

Promoter has skin in game, FII is increasing stake, DII stake is stable

Recent Developmentsand Key Triggers

Dedicated Freight corridor, Projected Wagon demand, Improving logistics share through Railways are big triggers for continuous growth of this segment

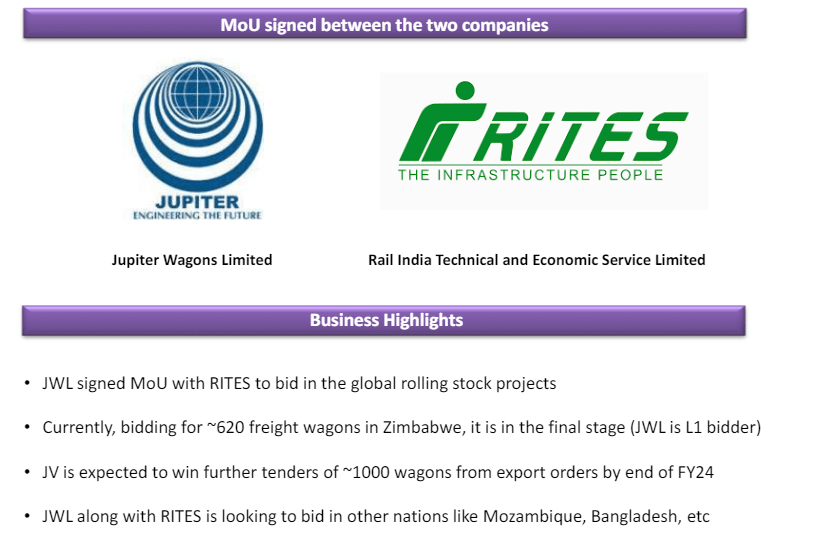

JWL has made a strategic entry into the global markets by signing a long-term Memorandum of Understanding (MOU) with RITES Limited, a prominent PSU associated with the Indian Railways, to explore opportunities in the international market for railway rolling stock projects. JWL’s focus is on the design, manufacturing, and supply of Railway wagons.

The Company is focusing efforts on achieving Import Substitution, particularly in the areas of High-tech and Highend Containers. To further elevate global competitiveness, manufacturing facilities have been fully automated, enabling consistent production and maintaining world-class quality standards. The manufacturing facility is certified by both ‘LRQA’ and ‘BVQI’.

A new foundry is scheduled to be established in Jabalpur over the next 18 months with a capacity of 2,000 tonnes, catering to both captive use and exports. This initiative is expected to yield cost savings in freight expenses.

In the Marine Container Business, the outlook for specialized containers is improving as the Company has: Secured a contract for 40-foot ‘Open Top, Coil Containers’ with a pilot order worth ₹ 1,000 lakh.

Received a Letter of Intent (LOI) from an Indian Subsidiary of a Prestigious Global Group for the supply of 1,000 units of special Flex Inverter containers for the fiscal year 2024-25.

JV Company JWL DAKO CZ India Ltd. has received an order aggregating ~₹ 11,200 lakh for axle-mounted disc brake systems from Indian Railways.

The BESS container, a key element in Solar and Data Centre Containers, offering energy storage capabilities has a huge market opportunity in round-the-clock Renewable Energy Projects as well as Commercial Industrial Energy storage in both domestic and international markets. With Jupiter’s expertise in making containers for this application, we now are looking forward to adding more value for the same by creating complete integrated solutions for varied markets.

Successful Qualified Institutional Placement (QIP) in May and December 2023 amounting to ~ ₹ 528cr which includes prominent investors, including DIIs like Tata MF, HSBC MF, Bandhan Equity Fund, and FII’s like Societe Generale, and Copthall Mauritius Investment Limited.

JWL is one of India’s largest wagon manufacturers, with a capacity of 9,600 wagons per annum with plans to enhance capacity to 12,000 wagons per annum by Q1 fiscal 2025.

JWL has also ventured in brake disc, brake systems for rolling stock and weldable CMS Crossing manufacturing during fiscals 2023-24 equipping JWL to capitalize on robust spendings for developing high speed train infrastructure, and to fortify its market position in this segment, in Q1 fiscal 2024 JWL has acquired Stone India Limited, having extensive infrastructure and licensing for brake manufacturing.

Valuations

Looking at their growth currently and opportunity size in coming years, Stock is trading at fair value. Once the capacity comes online and if company executes the order well , it might look undervalued intermittently

Risks

Exposure to risks relating to fluctuation in raw material prices and intense competition: The key inputs include steel and related products. While the IR projects generally have a long execution period and are covered by a price-variation clause to a large extent, private sector orders are generally fixed in nature.

Cash flows poses a big risk due to intensive working capital operations

Valuations are subjective but definitely its not hugely undervalued in short term

Most orders are from Railways and have this dependency in business, though company is trying to diversify

Technicals on 11-May-24

Conclusion

If you have understood the triggers and industries it cater to + RISKS which can materialize and have patience then think of buying this company in every dip, market offers, else Ignore the stock

Stock might be volatile in short term and give a chance to buy around 425-525 range for long term investment purpose

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Savita Oil Technologies Limited, established in 1961, is a specialty petroleum products company engaged in manufacturing Transformer Oils, White Oils etc.

The Co manufactures products like Transformer Oils, Liquid Paraffins, White Oils, Automotive and Industrial Lubricants, Coolants and Greases, among others. These products are essentially obtained through refining base oil, and topped with additives to derive the required characteristics. A wide range of lubricants, greases, and coolants of the Co are sold to retail customers under the brand SAVSOL

The Co has a market share of ~35% in the domestic transformer oil and white oil segments.

The Co’s manufacturing facilities are situated in the state of Maharashtra and at Silvassa in the UT of Dadra and Nagar Haveli and Daman and Diu with total refining capacities of 450,000 kilolitres per annum. Its windmills are located at 18 sites in the states of Maharashtra, Tamil Nadu, and Karnataka and have an installed capacity to produce 54.15 MW of wind-powered electricity

Company has 80 % domestic sales vs 20% exports

Revenue distribution 75% from petroleum and 25% from lubricating oils

Unit I – Navi Mumbai, Maharashtra Unit II – Mahad, Maharashtra Unit III – Kharadpada, Silvassa Unit IV – Silli, Silvassa

41 Stock points,

20,000 Retailers

400 Distributors

1,500 Franchise Dealers

Products, Segments and Strengths

Two major segments : Petroleum Oils and Lubricating Oils

Petroleum oils : Transformer oils, White and Mineral oil, Speciality oil : ~75% sales as portion of total sales over last 2 years

Transformer oils : These oils are used as an insulating and cooling medium in distribution transformers, power transformers and instrumentation transformers

White oils :

Offer wide range of highly refined specialty mineral oil based products under the “TECHNOL” and “SAVONOL” brand.

They manufacture petroleum jellies like Ultima White, Snow White, Yellow Petroleum Jelly and other specific industrial grade petrolatum’s under the brand “Savogel”

Key properties of this fluids are good lubricity, smoothness, softness and resistance to moisture in the formulations

Specialized waxes and emulsions including paraffin wax emulsions, microcrystalline wax, Polyethylene wax, oxidized PE wax and a range of wax emulsions. Wax Emulsion protect coating and ink surfaces for diverse applications

Cable filling and flooding compounds for copper cables as well as Optic Fiber Cables under “Savofil”, “Savoflod” and “Vitagel” brand names. This compound helps moisture tolerance, softness and stability at an extreme temperature

3.Formulated & Specialty Products

The 5G Telecom spectrum auction held in 2022 and subsequent rollout of the network is expected to generate healthy demand for this product

› Growing demand from end user market

› Government Linked PLI Scheme

Key Growth Drivers

Optic Fibre Cables

Textile & Leather

Auto components

Polymers

Refrigeration Compressors

Construction Compounds

Lubricating oils : Automotive and Industrial oils

Automotive oils

The lubricant brand SAVSOL manufactures and markets high performance lubricants, fluids, coolants & greases and is amongst the fastest growing lubricant brand of India

It has a comprehensive range of automotive lubricants meeting the growing demand for sustainable products in various categories, i.e., Passenger Car Oils, Motorcycle Oils, Commercial Vehicle Oils, and Other Specialty Products

SAVSOL portfolio has products which successfully meets the latest & stringent BS VI emission norms for automobiles

Savita Oil Technologies known for its high quality lubricant manufacturing with state-of-the-art plants and technology centre has been amongst preferred supplier to automotive OEMs for a wide range of lubricant applications

Trusted partner for leading automotive OEMs. Some of our OEM associations are existing for over two decades

A fully equipped technical and quality control lab ensures high quality standards

Industrial oils

Savita Oil Technologies has been a trusted partner to Industrial OEMs for a wide range of lubricant application needs.

› It has an elaborate product portfolio under Brand “SAVSOL” catering to various Industrial applications and provides

excellent lubrication, performance and protection to different types of Machines and Industrial Equipment

The exhaustive portfolio includes wide range of Hydraulic Oils, Turbine Oils, Thermic Fluids, Heavy Duty Industrial Gear

Oils, Transmission Oils, Greases, Heat Treatment (Quenching Oils), Metal Working Oils and other Specialty Oils

Strengths

Multi-decade relationships with many of our OEM and B2B customers across all product lines

In-house technology and R&D is the backbone of our company and has manifested many high quality products across the product portfolio.

Focus on innovation

Focus on sustainable products development

Management has almost 3 decades of experience.

Company has ISO and other necessary certifications in its field of operations

Clients

Fundamental Ratios, Cash, Loans, EBITDA,PAT margin, Shareholding pattern

Consistent record of Dividends since listing in 1994 Healthy cash generation over the years Debt free balance sheet Consistent track of profitability despite market volatility Longstanding relationships with customers and vendors

Consistent Tax records

Cash conversion cycle and working capital cycle is good.

Cash flows seems good

ROCE is reasonably above 20%

Shareholding pattern

Promoter has skin in game. SBI energy fund has entered recently

Transformer oils : Rising Investments over the next decade in transmission segment to support higher generation capacity and rural electrification Rising demand for modernization of aging grid infrastructure coupled with large scale capacity addition will boost the market

White oils : The Indian personal care industry is witnessing a boom due to changing perceptions, growing awareness, and the rise of direct-to-consumer (D2C) companies making waves in the online retail space Growing demand of cosmetic and pharma products from urban & rural India

Product Innovation

Company is focused on building an independent distribution network for our industrial lubricants and with this now in place , they want to rapidly scale up industrial lubricant volumes

Company has created a subsidiary and moving towards plastic recycling

Savita Greentec Limited (a subsidiary of Savita Oil Technologies Limited) is expected to commence construction of Greenfield Projects in plastic recycling in theQ4Fy24

SAVSOL Bio Boost, one of India’s most biodegradable engine oils is launched

Oct23 – successfully commissioned new Synthetic Ester manufacturing plant

Commissioned new Synthetic Ester manufacturing plant at Mahad, Maharashtra with a designed capacity of 5,000 metric tons of which current operational capacity would be ~3,000 metric tonnes per annum

The new synthetic ester manufacturing plant will provide a strategic advantage to Savita by making it the first company in the world to manufacture and market all three classes of Transformer Fluids vis. Mineral Oil Based, Natural Ester Based as well as Synthetic Ester Based Transformer Fluids. The applications of these Esters are very versatile, and we will be able to leverage our existing client base to cross-sell these products while tapping new clientele. With these plant-based esters, we will have a more sustainable and environment friendly product range in the premium and synthetic categories. We plan to launch a new range of EV Coolants and immersion Cooling Fluids based on Esters from this plant. One of our products has already been approved by a reputed OEM as an EV coolant. We are also undertaking trials with another potential customer for immersion cooling.

Environment friendly products

Company have evaluated the introduction of versatile ester-based compounds (esters) in product range to enhance our diversified offerings of environmentally friendly products. Group V Base Oils comprising Polyol, Phosphate and other Esters are the most superior performing fluids that exceed the performance of synthetic base oils on parameters of lubrication, thermal stability, oxidative stability, compatibility with most metals and sealants and biodegradable with low toxicity

Modernisation of Existing Transformers: Majority of India’s transformers and power infrastructure components are ageing and need replacement or modernisation. This drives the demand for newer, more efficient, and technologically advanced transformers.

Implementation of Smart Grid: The development of smart grids requires intelligent transformers that can handle bidirectional power flow, manage voltage fluctuations, and support grid automation. This opens avenues for technologically advanced transformers. Moreover, the demand for energy-efficient transformers that reduce transmission losses and improve overall grid efficiency is steadily expanding in India. The transformer fluids market in India holds promising opportunities as the country strives to meet its increasing power demands while addressing environmental concerns and adopting technological advancements.

Company is seeing a substantial increase in customer order books within the Power and Distribution Transformer sector, with their production capacity reserved for the coming 12-16 months. This heightened demand extends beyond India; the export segment to North America and other regions is also demonstrating promising growth potential. This is attributed to India’s competitive manufacturing ecosystem for transformers, well-suited to meet global requirements.

Alternative Fluids Bio-Based – Your Company also produces bioTransol, a natural ester-based insulating fluid designed for transformers. This groundbreaking product was originally launched by Savita Polymers Limited (earlier a wholly-owned subsidiary of your Company which is in the process of being merged into your Company), in 2015. Remarkably, it marked the first instance of an Indian company introducing such a product to the market. With an extensive reach, bioTransol has been applied to over 300 projects, solidifying its impact. This product promotes environmental consciousness with a high proportion of biodegradability. Moreover, its safety and efficiency surpass conventional options across various equipment applications. Your Company is actively engaged in collaborating with major national and state utility boards, as well as Original Equipment Manufacturers (OEM) clients, to showcase the product’s merits. Not only does bioTransol offer a more effective solution within its grade, but it also embodies environmental sustainability. In an environment where global OEMs are compelled to reduce their carbon footprint, the appeal of such products is further enhanced. Company is confident that the adoption of Natural Ester-Based Transformer Fluids will witness substantial growth, becoming an integral component of OEM consumption.

Synthetic Based – Your Company is poised to introduce Transol Synth100, a cutting-edge synthetic ester-based insulation fluid. This fluid represents a significant advancement in transformer fluid technology, surpassing existing solutions across a range of parameters. Transol Synth100 stands as the most robust transformer fluid to date. As this product comes at a higher cost compared to mineral or natural esters, Transol Synth100 finds application in highly sensitive applications such as Locomotives (Metro and Rail), Mining, and Floating Solar projects. The overall lifecycle cost of this fluid effectively offsets its initial investment which will serve as a key driving force in the gradual transition from mineral to ester fluids within the ecosystem. With the launch of Transol Synth100 in the coming financial year, your Company will achieve a remarkable milestone, emerging as the sole manufacturer of the entire spectrum of transformer fluids – Mineral, Natural, and Synthetic.

Capex

Capacity Expansion Increasing capacity through continued investments for efficient leveraging of comprehensive and balanced product portfolio

Valuations

Reasonable valuations with PE <20. If the company shows growth in coming years as per their talk and opportunity size, this price looks undervalued

Risks

During the quarter under review, two critical components – Base Oils and the Exchange Rate have witnessed major volatility and both of these impacted us adversely. Base Oils Prices have fallen about 25% since June 2022 and the Indian rupee also depreciated significantly in the Quarter ending December, 2022. This resulted in inventory and foreign exchange losses which have impacted our margins

Any policy changes can impact the company hard

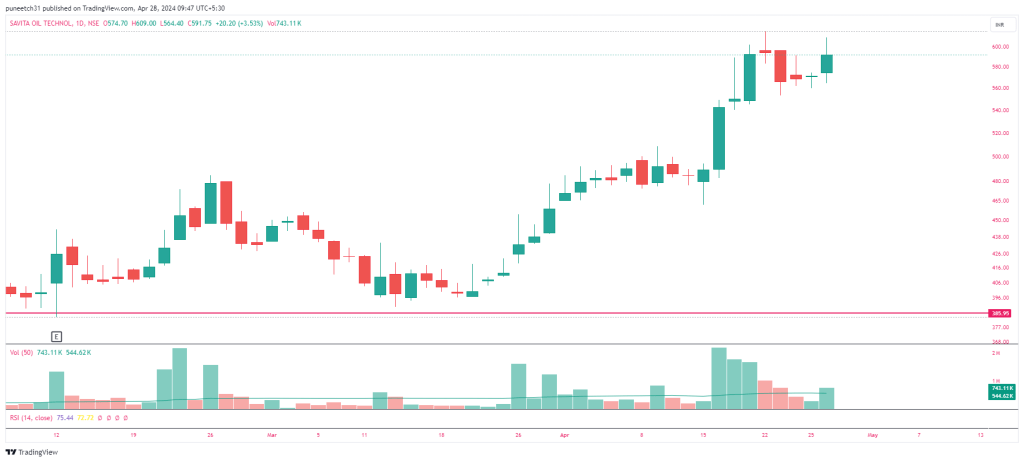

Technicals on 28Apr24

Stock has given a breakout and volumes are supporting upmove as well

Conclusion

If you have understood the triggers and industries it cater to + RISKS which can materialize and have patience then think of buying this company in every dip, market offers, else Ignore the stock

Stock might be volatile in short term and give a chance to buy around 500-650 range for long term investment purpose

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Kilburn Engineering Limited is primarily engaged in designing, manufacturing and commissioning customized equipment / systems for critical applications in several industrial sectors viz. Chemical including Soda Ash, Carbon Black, Steel, Nuclear Power, Petrochemical and Food Processing etc.

Company has cutting-edge manufacturing facility for fabrication, machining, and assembly of equipment located in Thane, Maharashtra (India). Manufacturing plant spans an area of 30,960 square meters and is equipped with state-of-the-art technology and machinery.

Products, Segments and Strengths

Company operates in two segments viz. Process Equipment and Tea Drying Equipment

Food Processing Equipment -During FY23 Company had bagged a total of 103 orders in the domestic market and 5 from overseas Market for tea dryers

40+ Years of rich experience with 3,000+ Installations globally done 200+ Workforce and 15+ Sectors catered by products and solutions

Kind of Equipment’s & system’s orders got by company

Silos for storage of PTA.

Metal extraction plant for extraction of exotic material from refinery spent catalyst.

Dryer, cooler, Granulator and Coater for fertilisers.

Calciner package for API (Active Pharmaceutical Ingredients) industry.

Hydrogen Fluoride Reactor package (Rotary Kiln)

Rotary Dryers

VFBD for wet clay

Tea Dryers and others

In the wake of increasing concerns about environmental degradation, our Paddle dryers have emerged as a sustainable solution for drying sludge. These advanced dryers play a vital role in states where strict pollution norms have been enforced, making it imperative for industries to adopt ecofriendly practices. By efficiently removing moisture from sludge, these dryers significantly reduce the volume of waste generated, thereby minimizing the environmental footprint of industrial processes

Sewage treatment — The market size for water and wastewater management in India was 216.03 billion in 2022. By 2027, it is anticipated to grow to518.15 billion, with a projected CAGR of 15.95% during the period 2023-2027.

On similar note, many other industries catered by Kilburn are expected to grow at 5-14% CAGR till 2030 and further

Eextensive and sophisticated R&D facility that are equipped with a full range of pilot plant dryers, including

Paddle Dryers

Vacuum Paddle Dryers

Band Dryers

Fluid Bed Dryers,

Vibrating Fluid Bed Dryers

Company has good manufacturing capabilities and order book of 236cr in hand at 31st Dec23.

Order received in Q3FY24 94cr. Executed 73cr

Continuous order inflow in Q4FY24 as well

Order Enquiries –> Approx 100cr

Clients

Reputed clientele lik ACC, JSW , Reliance, Arvind, PCBL, Fnolex, Granules, Coromandel, SRF, LnT and many other renowned names

Professional Managementteam

Fundamental Ratios, Cash, Loans, EBITDA,PAT margin, Shareholding pattern

Similarly ROCE and ROE are at reasonably good levels

Debt to Equity is under control

Sales, OPM, Net profit has been on rising trend continuously

Cash conversion cycle needs to be monitored.

Working capital days are good and have been improving

Shareholding pattern

Promoter has skin in game. One of the old promoters has been selling and other has been buying. Now its settled and Publicdomain have few strong holdings as well.

Promoter has been buying from open market continuously. Good buying happened between 270-310 zone

Last buy around 320

Acquisition of ME energy

This acquisition will help the company to grow faster

Company has put an estimated target of 500cr revenue by FY25 as ME energy has a 118cr pending order book

Capex

Expecting small capex of 15-20 cr till Dec25

Valuations

Expected Cumulative sales projections for FY25 is ~500cr (considering orders and Acquisition) and with PAT margin of ~12% after merger, we get PAT of 60 cr. So stock price may move towards 500 by 31Mar25. There could be volatility in stock which can be used for accumulation

Risks

Chequered history of non-payment of loans and subsequent new promoters on board.

Due to the non-payment of its loan obligations to RBL Bank Limited (RBL) starting in March 2020, KEL underwent debt restructuring in FY21. The resolution plan (RP) sanctioned by RBL in accordance with the Reserve Bank of India’s criteria was accepted by the company board on March 4, 2021, and it was put into effect on March 31, 2021. As per the RP, the outstanding principal loan of Rs 95 crores and interest of Rs 9 crores due to RBL up to 31 March 2021 was to be restructured. As part of the debt restructuring, Rs 65 crores of sustainable debt was converted into long- term loans with a 12.5 year payback period at an annual interest rate of 9%, Rs 13.5 crores in equity shares were allocated to RBL, and Rs 25.5 crores in 0.01% cumulative redeemable preference shares (CRPS) were also allocated to RBL.

Chemical companies are facing challenge to make sales. Their capex plan may be delayed further leading to slow flow of order to companies like Kilburn

Economy impact because of possible US recession might delay things by a year or more

High capital working requirements remain a risk.

Delay in Acquisition of ME energy. This is major risk in short term

Technicals on 10Feb24

Stock has been consolidating between 260-290 for almost few months and given a breakout recently and then got good results as well

Technicals on 31-Mar-24

Survived well in last one month market correction

Conclusion

If you have understood the triggers and industries it cater to + RISKS which can materialize and have patience then think of buying this company in every dip, market offers, else Ignore the stock

Stock might be volatile in short term and give a chance to buy around 270-340 range for long term investment purpose

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Ami Organics

SS9

CMP 1116, Market cap ~4100cr

ROCE ~20%, ROE ~15%, D/E ~0.16 PE ~57 (based on screener)

AMI Organics (AMI) is a research and development driven manufacturer of specialty chemicals with varied end usage and is focused on the development and manufacturing of advanced pharmaceutical intermediates for regulated and generic active pharmaceutical ingredients (“APIs”) and New Chemical Entities (“NCE”) and key starting material for agrochemical and fine chemicals. AOL has three manufacturing facilities (excluding the recent acquisition of Baba Fine Chemicals [BFC] during H1FY24). Company manufactures intermediates from the ‘N minus 8’ to the ‘N minus 1’ level (where N is the final active pharmaceutical ingredient [API])

Products, Segments and Strengths

Company operates in two segments

Advance Pharma intermediates — 185+ Products, Intermediates across 17 therapeutic areas, Chronic Therapy focus: ~90%, Majorly backward integrated to Basic Chemical level, 50-90% global market share key molecules

Fermion had been among the biggest clients for Ami Organics in this domain. Ami Organics had been supplying intermediates for APIs like Darolutamide (prostate cancer), Entacapone (Parkinson) and Trazodone (Antidepressant). Company would be supplying an advanced intermediate for the Darolutamide API, starting from Q4FY24. At present, the company is the exclusive supplier for the same.

Speciality chemicals –This is where we are interested in coming future

Niche KSM for Agrochem and Finechem companies, Parabens & paraben formulations, Salicylic Acid and other specialty chemicals that find end-use in cosmetics, dyes, polymers and agrochemical industries, animal foods, and personal care industries New segment – Electrolyte used in manufacturing cells for energy storage devices. This also has huge potential in solar industry, automobiles industry

Clients

Advance intermediates : Speciality chemicals sales ratio –Approximate is 82:18 which is expected to go towards 75:25 in coming time. FY23 Ratio was 84:16

Export Sales: Domestic Sales ratio is approx. 58:42 in FY23, Q2FY24 ratio was 54:46 due to China oversupply and price erosion factors

➢ Well established and long-term relations with domestic and MNCs across large and fastgrowing markets globally ➢ Diversified customer base, 58% of revenue from Top 10 customers in FY23, 13 customers associated since last 10 years, 50 customers associated since last 5 years ➢ Long term supply contract with key customers ➢ Prolonged adherence to stringent client requirements leads to new business from existing customer base as well as from new client. ➢High entry barriers due to long gestation period to be enlisted as a supplier, Involvement of complex chemistries, Regulatory requirements. First to Market in most of the products

Strong focus on R&D

120 R&D members with 16 PhD, 14 process patents, Average approx expense on R&D is 1.7% of Revenue over last 4 years. In absolute terms its almost 7-8Cr per year

The Patent Office, Government of India, has granted Pracess Patents to Company for its inventions titled:

A PROCESS FOR THE PREPARATION OF 2- (PIPERIDIN-4-YL)-1H-BENZO[D]IMIDAZOLE

APROCESS FOR THE DIRECT SYNTHESIS OF FEDRATINIB INTERMEDIATE for the term of 20 years in accordance with the provisions of the Patents Act, 1970. The above mentioned patented processes have been indigenously developed at the R&D Centre of Ami Organics Limited. With this the total number of Patents granted to Company for its innovative processes and technology stands at 9.(march2024)

Fundamental Ratios, Cash, Loans, EBITDA,PAT margin, Shareholding pattern

Sales and Profits have been growing decently(>25-30%) over past few years while for current FY24, it has slowed down, FY25 and FY26 seems to be the major booster for company going forward

Similarly ROCE and ROE has come down in last 2 years but still at reasonable levels

Debt to equity is at comfortable levels and can afford more debt for future expansions

Cash conversion cycle is on uptrend (not a good sign) and Working capital days are also increasing . Need to be monitored closely

Shareholding pattern

Increasing promoter holding, FII, DII are increasing stake, Public domain have few strong holdings as well

➢ Fermion contract: – Signed a new contract for additional advanced intermediate taking total product under CDMO contract to 3 products. On track to start the production from Q4FY24 onwards from Ankleshwar Unit

15-sep-23 Ami Organics Limited has signed another definitive multi-year, multi-tonne agreement with Fermion. As part of the agreement, Ami Organics will supply an additional advanced pharmaceutical intermediate to Fermion. Based on the supply projection shared by Fermion, the total minimum contract value is expected to be multi-million Dollar, spread across multi-year horizon. The product is expected to start contributing meaningfully to the revenue from FY25. Ami Organics had signed its first agreement with Fermion in November 2022 for supply of an advanced pharmaceutical intermediate. This agreement is in addition to previous agreement and further increases the total value of the CDMO contract with Fermion.

14-Dec-23 Ami Organics and Fermion ink another agreement for two additional Advanced Pharmaceutical Intermediate with Fermion. The products are slated to be manufactured at the Ankleshwar Facility and is expected to start contributing meaningfully to the revenue from FY25

Specialty Chemicals

Received orders for a UV Observer product used in Paint Industry. Expect commercial production to start from Q3 FY24

Electrolyte additives update- Advanced stages of negotiation of contract with couple of customers.

Process upgradation for existing products – methyl salicylate and parabens

it is working on two additives, not been manufactured so far by any other company in India. In this space, the company has received approval from nine customers and expects a large commercial order

Ami Organics Limited has signed a non-binding MOU with a global manufacturer of Electrolytes for manufacturing of electrolytes for battery cells and allied materials in Gujarat, India. In furtherance to this, the company will also sign an MOU with Government of Gujarat for investment amounting up to Rs 300 crores for set up of dedicated manufacturing facility for electrolytes business in the state of Gujarat, in the upcoming Vibrant Gujarat Summit 2024.

Capex ongoing

Pharma intermediates capacity to expand to 4x

Related to the Fermion contract is the capacity expansion plan in Ankleshwar at a capital outlay of Rs 190 crore. Here, one block is dedicated for Fermion. This would carry on supplies related to the recent contract. Machinery installation in progress in block-1 at Ankleshwar unit, Started the recruitment process for the new facility. On track to commence the production activity in Q4 FY24 .The Ankleshwar facility is envisaged to have 436 KL — nearly 3x bigger than the existing facility

Acquisitions

Baba Fine Chemicals Acquisition – Completed acquisition of majority partnership stake in Baba Fine Chemicals during Q2FY24. The acquisition of Baba Fine Chemicals (55 percent stake) is interesting as it deals with high entry-barrier products (photo-resistant chemicals), having applications in the semiconductor industry.

To reduce operational cost , the board has approved investment in a 16 MW solar power plant which along with already work in progress 5 MW solar power plant that will nullify our electricity expense once fully operational.

Company decided to fully impair the existing investment of Company, in the joint venture Ami Oncotheranostics LLC, as it is presumed that revenue generation from Ami Oncotheranostics will take significant time considering the inherent nature of its research activity in terms of longer gestation period and uncertain success rate

Transformation of acquired entities like Gujarat Organics

Recently they acquired two manufacturing facilities Gujarat Organics (which was making loss makings as they did green field expansion in 2018) as Guj Org was making losses, it was bought by AMI Organics and turned EBITA margin moved from meagre 2% to 10% as of now (expected to touch 18% by next 2 year – also highlighted in their conf call as they are moving from batch processing to continuous flow chemistry). This acquisition enhances its specialty and fine chemical portfolio to enter Agrochemical, Cosmetics & Polymer Industry. Due to this acquisition, one of client of Guj Organics referred them to make this electrolyte addictive. And hence, they have ventured into electrolyte addictive (belonging to carboxylic group) which is made by AMI in the whole Asia (except for few Chinese companies)

Details about Baba Fine chemicals

Valuations

Expected Cumulative sales projections for FY25 and FY26 is 2800-3500cr (considering existing business will also grow at 18-20%) and with PAT margin of 14% , we get PAT of 390-525 cr cumulatively. So stock price may move towards 2000-4200 Range by 31Mar26. There could be short term downside in stock which can be used for accumulation in case we are convinced about projections and sales

Risks

Susceptibility to raw material cost could affect Company profitability.

Inherent regulatory risk (USFDA compliance)

Competitive nature of industry driving pricing pressures. Oversupply from China does impact company growth in targeted markets

Combination of low margin and high margin products causes volatile OPM –This risk is expected to reduce with integration and business of other acquisitions done in recent years

High Capex ongoing and timely completion and start of production along with capacity utilization is a risk which needs to be monitored

High capital working requirements remain a risk. This is due to its wide portfolio, AOL needs to maintain sufficient inventory of the raw material as well as finished products.

Fermion contract getting cancelled midway

No major breakthrough in BFC business or electrolyte business

Technicals on 13Jan24

Stock has been consolidating between 900-1300 mostly in last 2+ years

Technicals on 3-Mar-24

Conclusion

If you have understood the triggers and industries it cater to + RISKS which can materialize and have patience then think of buying this company in every dip market offers else Ignore the stock

Stock might be volatile in short term and give a chance to buy around 1000-1200 range for long term investment purpose

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Below Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Tatva Chintan– CMP 2520 (Dated 3-feb-22)

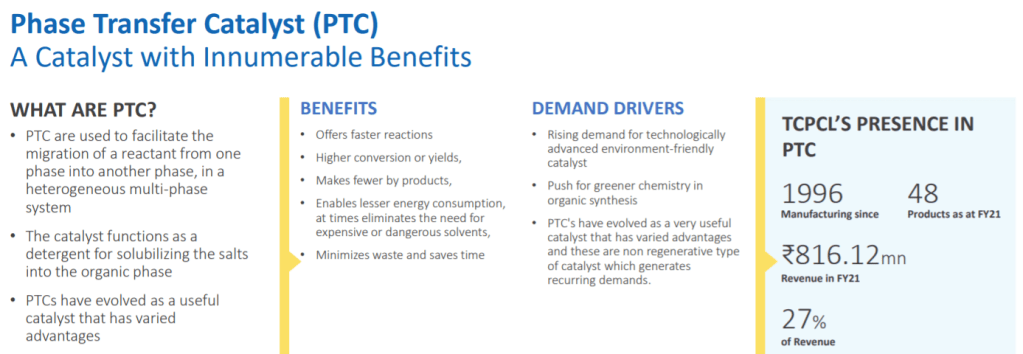

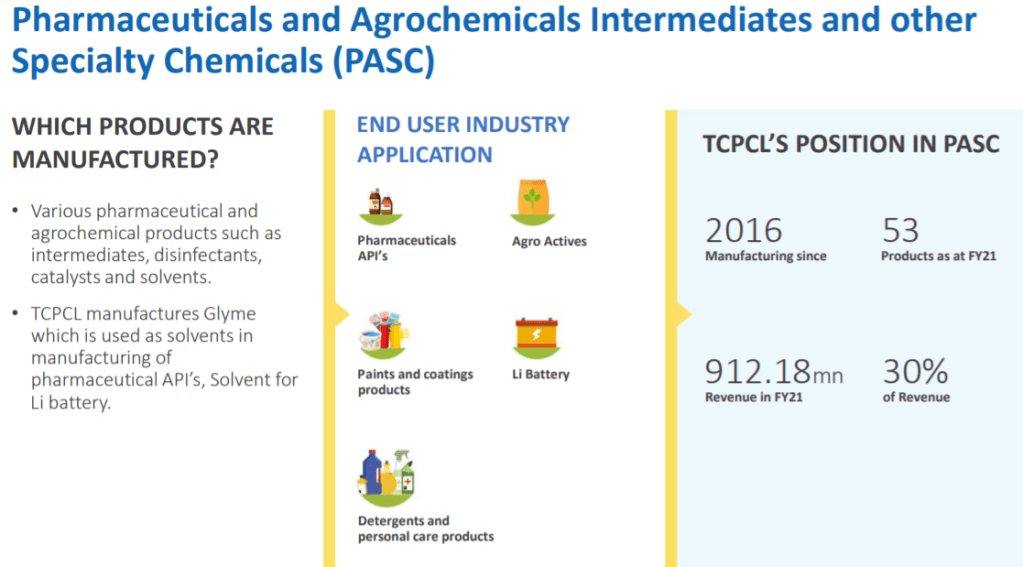

Incorporated in 1996, Tatva Chintan Pharma Chem Limited is a specialty chemicals manufacturing company. It is engaged in the manufacture of structure directing agents (SDAs), phase transfer catalysts (PTCs), electrolyte salts for super capacitor batteries and pharmaceutical & agrochemical intermediates & other specialty chemicals (PASC).

Business —

One of the leading producers with entire range of PTCs in India and one of the key producers across the globe

2nd largest manufacturer of SDAs for Zeolites globally and the largest commercial supplier in India

TCPCL is the largest producer of Glymes in India and third largest in the world.

Largest producer of electrolyte salts for super capacitor batteries in India

END USER INDUSTRIES — Growing industries in coming decade

Pharmaceutical API’s

Flavors and Fragrances

Agrochemicals

Environment Control Processes -NOx removal

Automotive – Catalytic Converter – Emission Control

Petrochemicals – Cracking crude

Automotive Transport & Infrastructure

Electric Vehicles

Consumer Electronics

Renewable Energy

Grid Balancing

Paints and coatings products

Li Battery

Detergents and personal care products

Moats —

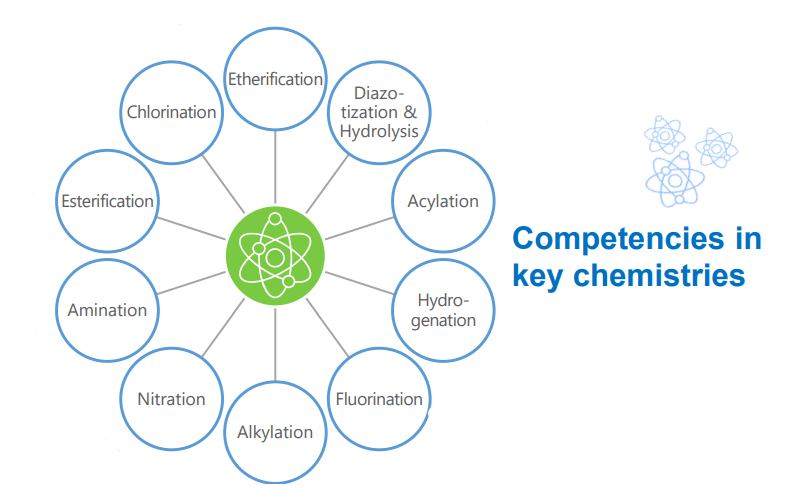

TCPCL is one of the few companies globally that uses Electrolysis process in organic synthesis. Advanced chemistries in process and for commercial development, manufacture and approvals, it takes 1-6 years for new players to enter this field.

In many of the segments, it is amongst top five players

Strengths

Considering the wide range of applications of our products, TCPCL can cater to customers across wide spectrum of Chemical Industries which ensures a sustainable business model. Diversified product portfolio has helped accelerate growth and in innovating and thus retain both new and existing customers

Diversified esteemed clientele

Necessary certifications in place : ISO 9001:2015 ISO 14001:2015 BS OHSAS 18001:2007

Advantages of Electrolyses

Electrolysis is considered as a ‘green’ chemistry process wherein apart from a single starting raw material, the process largely uses only water and electricity

Since no additional solvents or other chemicals are used, it is a safe chemistry

It has minimum requirement of auxiliary substances

The process enables faster output and Higher Purity

By deploying electrolysis, the products achieve the lowest possible process mass intensity

Region of operation

The company exports most of its products to over 25 countries, including the US, China, Germany, Japan, South Africa and the UK.

It reduced % revenue dependency on top 10 customers from 60% to 47%

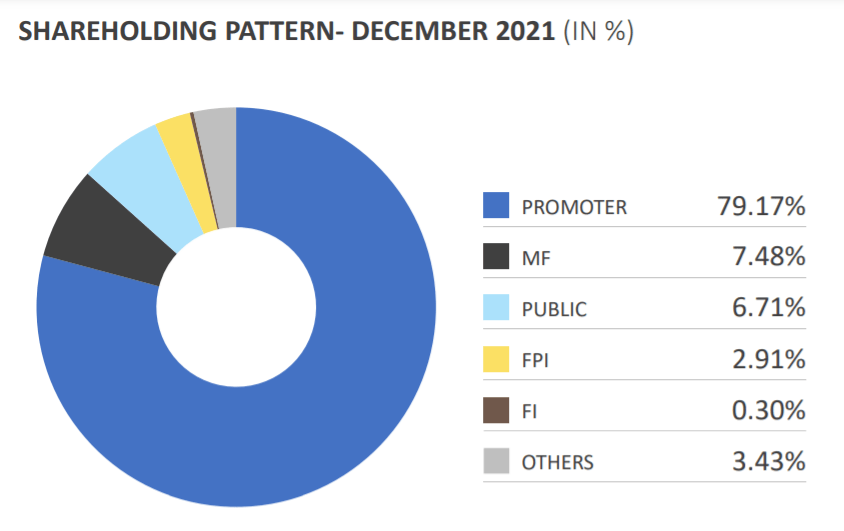

Shareholding

Promoter has sufficient skin in game with holding ~79% and other prominent players holding 10% more

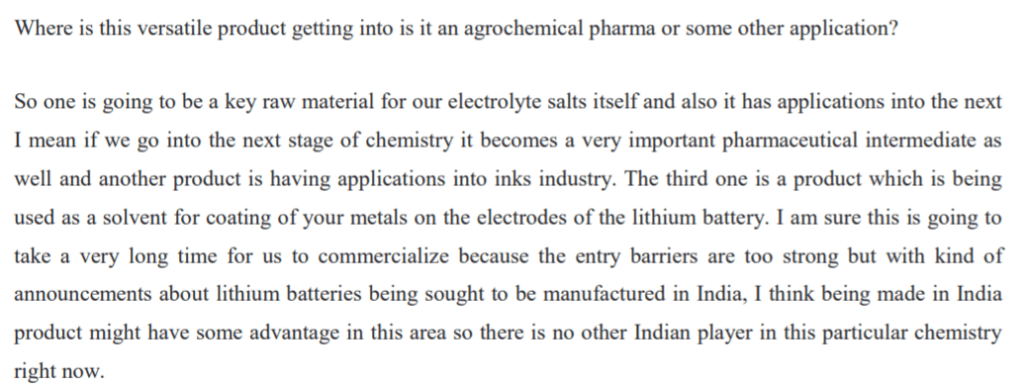

Getting into EV domain with supercapacitor batteries and new horizon opening up faster than anticipated

New versatile product development in Continuous flow chemistry us also capable in other applications including EV

Comfortable Leading market share in almost all operating domains

Mindset of accepting which projects

Risks (tried to see major risks, please do due diligence to understand more on this part)

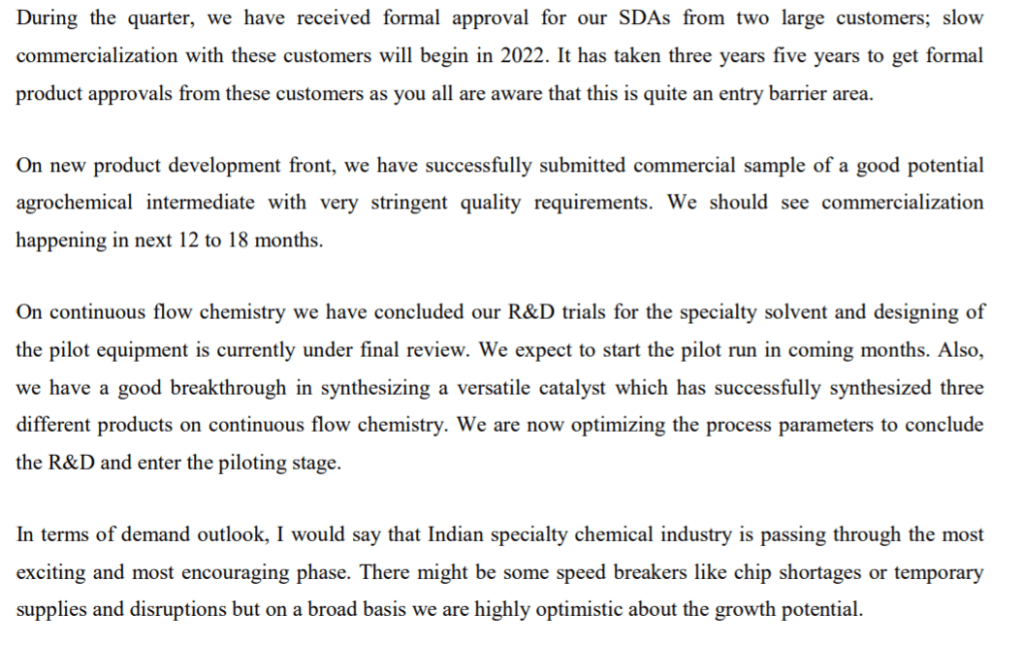

Delayed expansion –currently scheduled for Nov 22

Delay in semiconductors supplies impacting SDA in FY23 as well (current anticipation is till FY22)

Slow ramp up of electrolyte salts than projected

Approvals for new PASC delayed

Increase in raw material and frieght costs is already impacting margins, further increase will hurt next two quarters badly in terms of margins if it happens ( Q4FY22, Q1FY23)

Valuations —

They have to be seen in terms of huge growth runway available but current valuations don’t give that comfort to take large positions with risks on execution and inflation

Looks better to give time to company and see how it performs and keep accumulating in background in small tranches. That may work.

Your strategy can be different than mine. Your selection of company might be different than mine. So lets not be a BLIND FOLLOWER

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Vishnu Chemicals Limited is a market leader in manufacturing and sales of Chromium chemicals and Barium compounds across the world

Serving 12+ industries across 50+ countries (83 countries as per publicly available information)

Chromium Chemicals –>

~85% revenues (FY21) , Leading manufacturer in India as well as South Asia,

FY21 Domestic: Export Sales Mix: 51:49 , 3 manufacturing units

Over the last few fears, the company has diversified its Chromium revenue profile with presence in both domestic and export markets. Earlier the portfolio was concentrated in chromium, domestic oriented and now diversified and balanced geographically in domestic and export markets

Applications –> Pharmaceuticals, Leather tanning, Pigments and Dyes, Plastic masterbatches, Ceramic glazes, tiles, Electroplating, Automotives, Refractories, Wood Preservative, Paper pulping and others.

Barium Chemicals –>

~15% revenues (FY21), Leading manufacturer in India, FY21 Domestic: Export Sales Mix: 45:55 ,1 manufacturing unit.

Applications –> Ceramics, tiles, glazes, bricks, refractories and water purification chemical in caustic soda industry, speciality glass, Luminescent Compounds, etc.

Strengths

Long standing relationships with domestic and overseas marquee customers.

Well diversified board with specialists in field

Certifications — ISO 9001:2015 , ISO 14001:2008, REACH Quality Certification

Income, EBITDA, PAT, PAT Margin improving

D/E is high but decreasing as desired

Ability to pass the rise in input prices and freight costs.

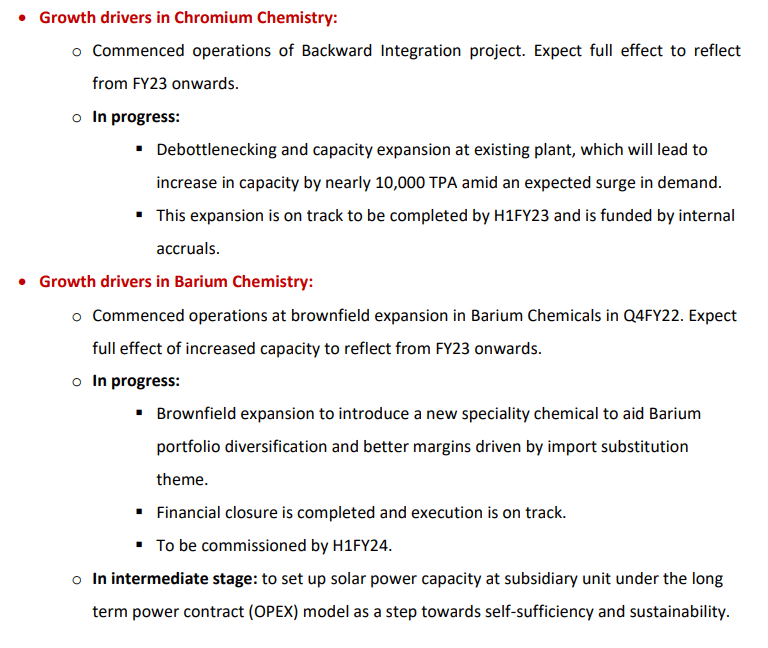

Triggers for company in coming quarters

Operating leverage: Most of the overheads or manpower addition are largely done considering FY21 as a base. Higher utilizations from existing capacity: Major debottlenecking completed in Vizag unit in FY21 will lead to better throughput & efficiency

Majority of the capital expenditure towards sodium carbonate in Chromium chemicals is completed, Majority of company’s sodium carbonate’s current requirement will be met through the process. Significant cost reduction expected from upon being operational by Q4FY22E.

Focus is to increase market share with higher volumes in Barium chemicals

Leading manufacturer in India for Barium Chemical : Other players have less than 1/10th of Vishnu’s current capacity.

Incremental capacity of 20,000 TPA of Barium Carbonate expected to be operational by Q4FY22E

China plus 1 strategy has made them a preferred vendor instead of being a second option for their customers.

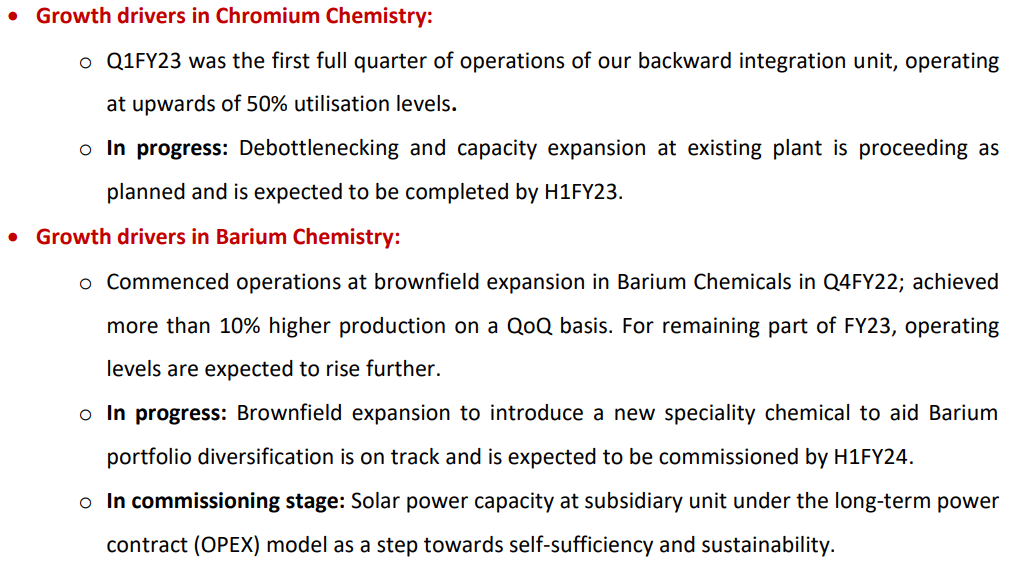

16-may-22 update by management

7-Aug update by Management

Exit Triggers

Crash in finished products prices or inability to pass on raw material in coming quarters

Any change in China +1 strategy for customers

Less than expected utilization of incremental capacity

Risks

Debt profile is still out of comfort zone

ROCE and PAT Margin still not as much as desired

Any Exports oriented issues including currency risk, freights costs

Significant promoter pledge of 40%

Any delay in operations of underway capacity expansion