Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Business

Incorporated in 2004, Syrma SGS Technology Limited is a Chennai-based engineering and design company engaged in electronics manufacturing services (EMS). The company provides integrated services and solutions to original equipment manufacturers (OEMs) from the initial product concept stage to volume production through concept co-creation and product realization

Syrma is a technology-focused engineering and design company engaged in turnkey electronics manufacturing services (“EMS”), specializing in precision manufacturing for diverse end-use industries. They are leaders in high-mix low volume product management and are present in most industrial verticals

Product Portfolio

– Printed circuit board assemblies (PCBA)

– Radio frequency identification (RFID) products

– Electromagnetic and electromechanical parts

– Motherboards

– Memory products – DRAM modules, solid state, and USB drives.

Manufacturing facilities

The company operates eleven manufacturing facilities in North India (Himachal Pradesh, Haryana, Uttar Pradesh) and South India (Tamil Nadu, Karnataka). The manufacturing facilities in Tamil Nadu are located in a special economic zone. The manufacturing facility in Haryana has been set up under the Electronic Hardware Technology Park scheme, which allows the company to avail of tax and other benefits.

R&D Capabilities

Co. has 3 dedicated R&D facilities, 2 of which are located in Chennai and Gurgaon, and one in Stuttgart, Germany. R&D efforts are focused on

(i) developing new products and improvement of the quality of existing products, and

(ii) driving the design and engineering capabilities and original design manufacturing capabilities of the company.

Customers and Regions of Revenue

TVS Motor Company Ltd., A. O. Smith India Water Products Pvt. Ltd., Robert Bosch Engineering and Business Solution Pvt Ltd., Eureka Forbes Ltd Limited, CyanConnode Ltd., Atomberg Technologies Pvt. Ltd., Hindustan Unilever Ltd., Total Power Europe B.V.

Company’s products are sold in 25+ countries, including USA, Germany, Austria, and the UK. In FY22, exports contributed 55% of the revenue.

Awards

Dec’22 Best EMS Supplier 2022 Award by Pricol

Nov’22 Innovation & Technology Excellence Award by Wabtec Corporation

Oct’22 Award for Techno Visionary – Industry for the Year 2022

Experienced promoters and established track record of the company

Syrma belongs to the Tandon group, which started its first manufacturing unit in 1976 for the manufacture of floppy drives for IBM. The unit was the first hard disk drive (HDD) manufacturing unit in South Asia then. Mr Sandeep Tandon, Chairman of Syrma, has over two decades of experience in the electronics industry. By 2000, the group diversified to high-volume electronics manufacturing services for leading IT majors of the world. The group’s range of products includes printed circuit boards (PCBs), magnetic disk drives, magnetic coils, RFID tags, etc. The promoters of the acquired entity – SGS – have more than three decades of experience in the electronics manufacturing industry, with operations across six manufacturing facilities. The company is led by four directors, who are also its founders. The promoters of the company are professionally qualified and have degrees in electronics engineering/management from reputed institutions. Mr J S Gurjal, who was the promoter of SGS, is now the Managing Director of Syrma.

Industry and prospects

The global EMS market traditionally comprised of companies that manufacture electronic products, predominantly assembling components on PCBs and box builds for OEMs. EMS differs by service providers, and any particular partner may provide any combination of the following: PCB assembly, cable assembly, electro-mechanical assembly, contract design, testing, prototyping, and aftermarket services. The market in India is highly competitive and there are more than 30 organized companies in the EMS industry, but the commercial semi-conductor fabrication operation is almost non-existent. The competition concentration is moderate as the top three companies account for about 30% of the market. The companies follow either of the two unique business models – high volume/low mix or low volume/high mix.

In terms of government initiatives for the sector, the Indian Government is attempting to enhance manufacturing capabilities across multiple electronics sectors and to establish the missing links in order to make the Indian electronics sector globally competitive. India is positioned not only as a low-cost alternative but also as a destination for high-quality design work. Many multinational corporations have established or expanded captive centres in India. Post the COVID-19 pandemic, many global electronics manufacturers are contemplating on the China+1 strategy and looking for alternate manufacturing locations for exports business, which is advantageous to Indian manufacturers. Syrma’s presence in the ODM segment offers the company a better position and margins. However, the company’s ability to scale up operations amid the improved demand for the sector and the capability of the company to manage the shortage of raw materials and the working capital cycle remains key to the prospects

Revenue mix

Quarterly basis

Nine month basis

Current mix of the Auto, Consumers, Healthcare , Industrials, IT and Railways

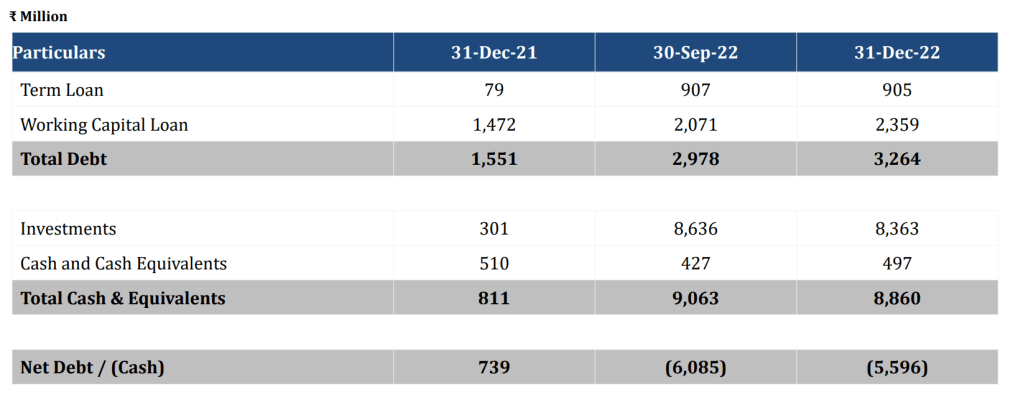

Fundamental Ratios, Cash, Loans, EBITDA,PAT margin, Shareholding pattern

Company has sufficient Cash to grow

Stable PAT and EBITDA margins , ROCE is approx 13%

Opportunity Size

The Indian ESDM market is expected to grow at about 40% annually. The company expects to grow in line with industry growth rates.

Triggers

The company IPO has given sufficient cash for capex. Capex will involve around Rs.38 crore for setting up a R&D facility in Chennai, Rs.108 crore for setting up and expanding the manufacturing facility at the Chennai Plant, around Rs.52 crore for setting up new manufacturing facilities in Hyderabad, around Rs.228 crore for setting up and expanding of manufacturing facilities in Manesar, around Rs.62 crore for setting up new facilities in Bawal, and around Rs.83 crore for setting up new facilities in Hosur.

Q3Fy23 bringing up our new facility in Manesar and Chennai for the design and development

Incorporation of new subsidiary

Syrma SGS Electronics Private Limited is incorporated as a wholly owned subsidiary of the Company on March 03, 2023

To carry on the business of designers and manufacturers, buyers, sellers, assemblers, exporters, importers, distributors, agents, and dealers in memory chips, memory modules, PCB assemblies and other storage products, printers, readers magnetic or otherwise, CRT displays and terminals and all other electronic and communication equipment and parts, components, assemblies and subassemblies to be used in the computer and electronic industry

including voice coils, voice coil actuator assembly, antenna coils, smart cards and radio frequency identification devices.

Acquisitions of SGS and PerfectID

This is playing out already in right direction as businesses acquired are complementary

Syrma acquired a 20% stake in SGS in November 2020. Funds of Rs.92.04 crore from private equity funds and other shareholders have been infused in Syrma in FY21, partly as equity and partly as preference capital, which has been utilised for the purpose of inorganic growth by way of acquisition of SGS. The erstwhile promoters of SGS now hold 9.23% share each in Syrma, totaling to 37%.

SGS, incorporated in 1986, is an Indian EMS company that primarily assembles PCBs for its clients. In terms of customer and geographical profile, there is no overlap between Syrma and SGS, thereby diversifying the segment and client profile on a consolidated basis.

Syrma also acquired 75% stake in Perfect ID India Private Limited in October 2021. PerfectID manufactures RFID label tags and passive inlay tags, which is in addition to the existing capabilities for the manufacturing of RFID hard tags, thus expanding the RFID products portfolio.

PLI approvals

Company has received 2 PLI application Approvals in the telecom and in white goods air conditioning sector. As of date, the telecom PLI investments are on track, new facility at Manesar has been commissioned, it has gone into production in the second quarter of FY23 and expect huge traction in that business going forward in the coming quarters. The air conditioning PLI for products are under validation and it would be some quarters before we see any outcome. Products for the Indian market both inverter and non-inverter are under validation.

Company is focused on building out more ODM type development with current and new customers.

Very strong audits done by new marquee customers throughout facilities are done, so company is expecting new business to roll in over the next six to nine months with those customers

Order book size 1700 cr Sep22, 2100cr in Dec22–which is executable within 12 months is about Rs.1800 Crores and the spillover is about Rs.300 Crores

Capacity utiliation of old plants 75% approx, new plants commisioned approx 50%

Top 10 client concentration is 47% Dec22

In future margins increase can come from healthcare shipments which is export oriented business, or box build assemblies going more or asset turn increases with more production line and bulk order in consumer segment

Company is the single source for a lot of customers

Company is expecting rebound in Europe in two quarters

The growth is primarily led by continuous efforts on design lead manufacturing and has broadly been across sectors, but led by auto and consumer. The growth in a few sectors like healthcare and exports has been muted and slow because of the recessionary conditions and inflation in Europe, but we are very confident on the long term story and expect this to rebound in the coming quarter or two quarters.

Q3Fy23 call

Consumer growth business is primarily lead by our entry into the fiber to home devices and the telecom PLI scheme and the visibility which we have received makes us confident that this will lead to a sustainable growth in this segment in the coming quarters. It is not a one off growth, but a sustainable growth and we have also added more technology partners in this segment, which will further broaden the base and derisk the segment from the risk of a particular technology partner going down or a customer going down so we are broadening the base on this front.

In the automotive, the higher traction of growth will be in the EV segment

Next cycle of growth from EV charging infra and energy storage infra

Risks

High Valuation in short term

One needs to keep long term view, buy as SIP for risk mitigation of valuations

Exposure to volatility of raw materials and forex rate fluctuations due to high reliance on imports

Syrma’s raw materials consist of many components, including ICs, among others. Majority of the components, chips and PCB ICs, are imported and Syrma has the liberty to choose the buyer in most cases. Most of the contracts of Syrma with its suppliers are back-to-back contracts. Also, though the prices with most of Syrma’s customers are negotiated and agreed to initially, they are reviewed regularly. Recent times have seen a severe shortage of key components like ICs and this may also impact the operating margins and the working capital cycle of the company. Due to the high lead time for chips, which extends up to 52 weeks in some cases, the inventory-holding has increased. The company has to make advance payments in some cases to secure the raw materials, which has increased the working capital borrowings of the company. In the short term, this is expected to continue and the margins and working capital will remain affected by the shortage of semi-conductor chips.

Technological obsolescence risk

Electronics manufacturing companies are constantly exposed to obsolescence risk, which requires the company to keep up with the changes and advancements by constantly upgrading its products and technologies. But the company has seen and adapted to changes since inception and has been aware of the technological advancements, right from floppy disks manufacturing to RFID tags now. Syrma has recently forayed into manufacturing RFID tags, considering that the market for the same is expected to grow exponentially in future. The ability of the company to continuously enter new advanced product categories will be key to its future prospects.

Impact of the slowdown in the European and the U.S. market would only on this portfolio? Or it could be in any of the other segments of the exports of EMS?

In general, there’s a softening of the growth, I would say there is a reduction but there is a softening of the growth which we had projected, which we believe is for maybe 2 quarters or I don’t know, it’s just the geopolitical situation. But because of the diversified portfolio which we have, we have been compensated by other segments of the business, which is the domestic-led business. So, we would see the export business impacting on our overall plan for this year, in terms of our customer mix

Technicals on 14th May

Technicals when I entered

Disclosure –Invested from lower Levels . Do your own diligence before buying/selling

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Discover more from ALPHA AFFAIRS

Subscribe to get the latest posts sent to your email.

5 thoughts on “Company at Y2K moment”

Comments are closed.