BNPL model : Wallet Based

BE FINANCIALLY INDEPENDENT

Mobikwik is a Fintech company – one of the largest mobile wallets and one of the largest Buy Now Pay Later players

Its a leading company in its domain

They are filed their DRHP for an IPO and IPO is expected in 1-2 months

Limited quantity of its shares are on offer for sale and those interested,please email me at alphaaffairsf2f@gmail.com to collaborate further on this

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Exxaro Tiles IPO-Incorporated in 2008, Exxaro Tiles is engaged in the manufacturing marketing activities of vitrified tiles.,

Business — The company manufactures Double Charge Vitrified Tiles (double layer pigment) and Glazed Vitrified Tiles made from ceramic materials i.e. clay, quartz, and feldspar. Its product portfolio consists of 1000+ different designs of tiles in 6 sizes. Topaz Series, Galaxy Series, and High Gloss Series are some of the well-established products of the company. It supplies its products to large infrastructure projects i.e. residential, educational, commercial, hotels, hospitals, government, builders or developers, religious institutions, etc.

Region of operation — Major cities in India and It also exports tiles to different countries across the globe i.e. Poland, Bosnia, USA, and others.

Offer purpose — The IPO is issuance of shares worth ₹161 crore for debt clearance and general corporate purposes.

Risks —

The tiles segment is highly competitive with established listed names in the market as well as a huge unorganized segment that is active in manufacturing tiles. The company provided security regarding loans from banks by creating a charge over its movable and immovable properties. The total outstanding amount payable by the company stands at Rs 142 crore as of FY21. It carries high trade receivables on its balance sheet, accounting for 94 per cent of its current assets and 24 per cent of its total assets. As the company plans to expand, this can increase the quantum of trade receivables and inventories

Strength

Variety of vitrified tiles design choices in different sizes.

Large dealer network with 2,000+ registered dealers.

Strong PAN India presence in 27 states of India.

International presence with export to 13+ countries across the globe.

One of the largest manufacturing plants of glazed vitrified tiles in India.

Future

Earnings have been growing well and with real estate boom talk, it may turn out to be good story. Overall company and its products don’t have any moat

Valuations

Valuations do look fully priced at the current earnings levels of FY21, the earnings have been growing also well.

Should we apply?

People can subscribe only for listing gains.

If holding, need to patient for medium to longer term

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Devyani Internationals Limited IPO-“DIL” is the largest franchisee of Yum Brands in India and is amongst the largest operators of chain quick service restaurants in India and are among the largest operators of chain quick service restaurants (“QSR”) in India on a non-exclusive basis. DIL is also a franchisee of the Costa Coffee brand in India, which is owned by Costa,

Business — DIL’s business is broadly classified into three verticals that includes stores of KFC, Pizza Hut and Costa Coffee operated in India (KFC, Pizza Hut and Costa Coffee referred to as “Core Brands”, stores operated outside India primarily comprising KFC and Pizza Hut stores operated in Nepal and Nigeria (“International Business”); and certain other operations in the F&B industry, including stores of our own brands such as Vaango and Food Street

Region of operation — Major cities in India and in Nepal, Nigeria

Offer purpose — The IPO is issuance of shares worth ₹1838 crore for debt clearance and general corporate purposes.

Risks —

Termination of or inability to renew long term contracts with brands

Loss making company

High and intense competition in QSR space

Outstanding litigation proceedings against the Company, Subsidiaries, Directors, and Promoters

Strength

Presence across key consumption markets

Highly recognized global brands catering to a range of customer preferences

Multi-dimensional comprehensive QSR player

Future

The quick-service restaurant channel has been rapidly growing in popularity in India, owing to factors such as rise in literacy, exposure to media, increase in disposable incomes, and easier and greater availability. Affordability has also been a key factor.

Valuations

Valuations are high and bit lesser than peers

Should we apply?

People can subscribe only for listing gains. Sell on listing day

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

KRSNAA IPO– Incorporated in 2011, Krsnaa Diagnostics Ltd or “KDL” is one of the fastest-growing diagnostic chains in India..

Business — offers a wide range of diagnostic services such as imaging/radiology services (X-rays, MRI), routine clinical laboratory tests, pathology, and tele-radiology services to private/public hospitals, medical colleges, and community health centres.It currently operates 1,823 diagnostic centres that are offering radiology and pathology services across 13 different cities in India.

Region of operation — Key focus on Non metro cities and lower tier towns

Offer purpose — The IPO is issuance of shares worth ₹1213 crore to Finance the cost of establishing diagnostics centres at Punjab, Karnataka, Himachal Pradesh and Maharashtra; debt clearance and general corporate purposes.

Risks —

KDL generates nearly two-thirds of revenues under PPP model, increasing its dependence on payments under contracts with public health agencies.

Pricing dependent on recommended or mandatory fees fixed under the terms of the agreements

High and intense competition

Strength

Rentals are limited and marketing spends are low, with captive customers ensuring high growth

Fastest growing diagnostic chain in India on multiple parameters

Company’s PPP agreements are typically long-term in nature, enabling higher revenue visibility

Extensive network of integrated diagnostic centres across India

Future

The Indian diagnostic industry has grown consistently over the past 3 fiscals and is projected to grow at a CAGR of ~15% over next few yearsAdditionally, the PPP segment of healthcare services is large on the back of higher government spending in the PPP segment.

Valuations

Valuations are high and comparable to peers

Should we apply?

People can subscribe for long term

Expecting good listing gains.

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Glenmark Life Sciences IPO– Incorporated as Zorg Laboratories Private Limited in 2011 and acquired by Glenmark Pharmaceuticals Limited in 2018,.

Business — Glenmark Life Sciences Limited is one of the leading developer and R&D driven manufacturer of select high value, non-commoditized active

pharmaceutical ingredients (APIs) in chronic therapeutic areas, including cardiovascular disease (CVS), central nervous system disease (CNS),

pain management and diabetes

Region of operation — The company sells APIs in India and exports to multiple countries in Europe, North America, Latin America, Japan and the rest of the world (ROW)

Revenue/Product Mix – India 56%, Exports 44%

Regulated 66%, Emerging 33%, others 1%

Offer purpose — The IPO is fresh issuance of shares worth ₹1060 crore and an offer for sale to the tune of ₹454 crore by existing promoters and shareholders.Proceeds from the fresh issue would be used towards funding capital expenditure requirements for expansion of the company’s manufacturing facility; debt clearance and general corporate purposes.

Risks —

Revenue of ~55% from Top 5 Customers leads to concentration risk with promoter being the major customer itself

High dependency on China for key raw materials

High dependency on API business

Strength

Strong Promoter

Key Strong customers

Consistent track record of financial performance.

International presence with export to regulated markets

Future

Company has been growing well in revenue and profitability. High Value and non commoditized API are the key. Promoter backing also there. API have good future and Expansion of facilities and entering into CDMO will help company for next phase of growth

Valuations

Valuations are decent and comparatively lesser than peers

Should we apply?

People can subscribe for long term and keep on adding on dips & review holdings with each quarter earnings

Expecting good listing gains.

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Tatva Chintan IPO– Incorporated in 1996, Tatva Chintan Pharma Chem Limited is a specialty chemicals manufacturing company. It is engaged in the manufacture of structure directing agents (SDAs), phase transfer catalysts (PTCs), electrolyte salts for super capacitor batteries and pharmaceutical & agrochemical intermediates & other specialty chemicals (PASC).

Business — It is the largest and the only commercial manufacturer of SDAs for zeolites in India. It also enjoys the second largest position globally. It serves customers across various industries including automotive, petroleum, pharmaceutical, agro chemicals, paints and coatings, dyes and pigments, personal care and flavor & fragrances

Region of operation — The company exports most of its products to over 25 countries, including the US, China, Germany, Japan, South Africa and the UK

Revenue/Product Mix – India 28%, China 18%, US 15%, Others 39%

SDA 40%, PASC 31%, PTC 28%, Electrolyte Salts 1%

Offer purpose — The IPO is fresh issuance of shares worth ₹225 crore and an offer for sale to the tune of ₹275 crore by existing promoters and shareholders.Proceeds from the fresh issue would be used towards funding capital expenditure requirements for expansion of the company’s Dahej manufacturing facility; up-gradation of research and development facility in Vadodara; and general corporate purposes.

Risks —

Revenue of 60% from Top 10 Customers leads to concentration risk

Highly competitive industry and well established peers like Aarti Industries Limited, PI Industries Limited, Fine

Organic Industries Limited, Delta Finochem, Dishman group

High Expenses on raw materials (~50% of total expenses)

Strength

It is the largest and the only commercial manufacturer of SDAs for zeolites in India. It also enjoys the second largest position globally

Marquee list of customers Bayer, Merck, Navin Flourine, Divis,SRF, Atul, Laurus.

Strong long-term relationship with key customers with 53% customers with it over 5 years

Consistent track record of financial performance.

International presence with export to several countries i.e. China, USA, Japan etc.

Future

Company has been growing well in revenue and profitability. Unique products and diversified portfolio may help the company to retain growth path. Competition is high and will increase in coming years. Expansion and investment into R&D will help company for next phase of growth

Valuations

Valuations are as per bull market and comparatively lesser than peers

Should we apply?

People can subscribe for long term and keep on adding on dips & review holdings with each quarter earnings

Expecting strong listing gains.

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Zomato IPO is little different because company is showing losses and when they will break-even is not sure. So read further and analyse all points with a pinch of salt. Many investors dream of being a venture capitalist one day and to all those guys, Zomato is giving you a chance.

Put your HAT of venture capitalist and drop the hat of investor to view this IPO. If it works good — ENJOY!!, If it does not–Don’t lose sleep.

Zomato IPO– Incorporated in the year 2008 as a restaurant-discovery website – Zomato, is now one of India’s largest food delivery company.

Business — Zomato has four business segments – two core B2C offerings including food delivery and dining-out. There is B2B ingredients procurement platform ‘Hyperpure’ and the customer loyalty program, ‘Zomato Pro’ as well

Region of operation — Company has operations in 23 foreign countries – UAE, Australia, New Zealand, Philippines, Indonesia, Malaysia, USA, Lebanon, Turkey, Czech, Slovakia, and Poland. However, the company generates 90% of its revenue from India.

Offer purpose — 9,000 crore will be a fresh issue, while the remaining an offer for sale from the oldest investor – Info Edge (India) Ltd. Company will be possibly using this money for organic and inorganic growth

Risks —

Company unit economics of profitability is not sustainable as of now

Highly competitive industry and many players have shut down in past few years. Any new player with deep pockets can come and start competing. Amazon has already started with aggressive pricing

High dependence on order size and repeat orders for making money

Strength

Adjusted for cash and cash equivalents, Zomato has an asset-light balance sheet and it will help company to sustain for few more years with almost 16000cr cash and cash equivalents

Covid-19 has given push to delivery based eating model and it will possibly help the company to cut operational costs with lower discounts and higher delivery charges

Only two major players in fray and other players are only focused on one part of business while Zomato is well leading ahead in other domains as of now

Able management

International presence

Future

Company has been growing and survived last few years onslaught when many players have shut shop(including uber, ola, foodpandaetc). The way Indian population is moving to nuclear families, demand for food delivery will increase and so will be competition.

Hence ability to charge high prices may remain limited.

Diversification into other areas like stake in grofers, kitchens, increase in memberships may help the company to survive against competition a bit longer.

How fast they can expand in tier 2 and tier 3 towns and how much they are able to extract from people is the key in next few years for breaking even.

Its the only player in 4 different segments as compared to peers is an advantage for them as of now

Valuations

Valuations are extremely stretched out. Nothing much to talk sensible here

Should we apply?

People falling into high risk taking category can bid in IPO and and add more after listing to play out this theme over few years.

People who can take risk of capital erosion can subscribe with one lot and book out on listing gains if any.

Please note that company is not profitable and entire capital put in company shares can go down the drain if things do not turn in anticipated way

Whatever you want to do with this IPO , don’t become a long term investor if you applied for listing gains or vice versa. Be sure of why you are applying and stick to that

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

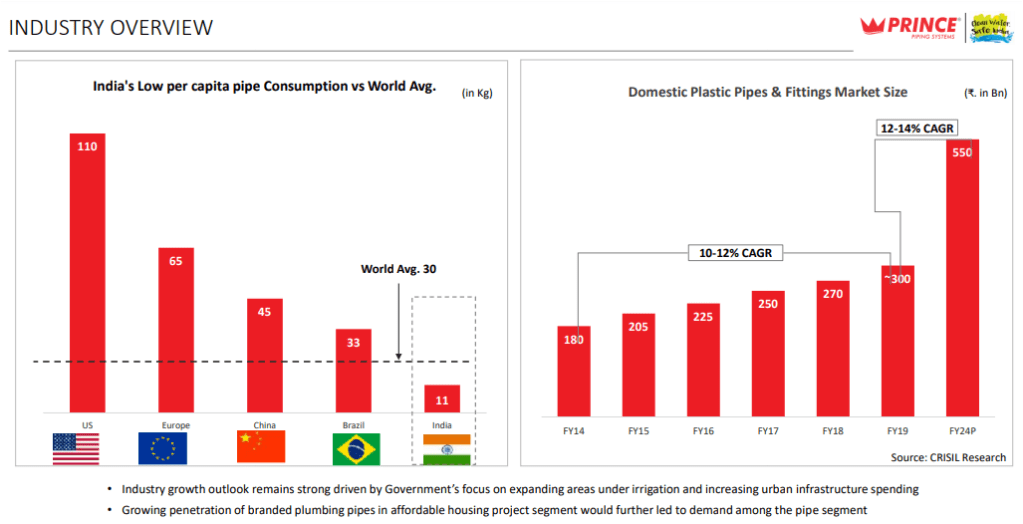

Prince Pipes and Fitting makes polymer pipes and fittings in India that are used in plumbing, irrigation and soil, waste and rainwater (SWR) management

It has 7,200 stock keeping units (SKUs) and 1,500+ channel partners.

Company has strong cash flow from operations and business share in Q4FY21 has been 69% from construction

Company current strategy is to expand in south india and increase distribution network while keeping the margins(EBITDA,OPM), ROCE in similar range

Company has been able to make use of 3 drivers of margin expansion in FY21 : inventory gains, product mix change, superior pricing power: past 8 Quarters company has been aggressive in passing on price .

Growth triggers

Total installed capacity of approximately 259,000 tonnes per annum (TPA). This will increase by a further 51,000TPA once its Telangana plant is fully commissioned- that means almost 20% increase in capacity

Various Government initiatives like AMRUT scheme, which is aimed at providing basic services, such as WSS, and ensuring that every household has access to assured tap water supply and a sewerage connection. Jal Jeevan mission (Urban) focuses on providing water supply to 4,378 urban local bodies with 260 million household tap connections. Nal se Jal scheme is planned to offer piped water to every rural household by 2024 –all these schemes is helping industry to grow by 35%(estimated) in next 2-3 years

There is a visible structural shift from unorganized to organised players and Prince pipes has shown both volume and sales growth wile other major players have shown de-growth in FY21

PPF is gradually increasing its emphasis on high-margin business of CPVC and double-wall corrugated pipes (DWC).

Recent tie up with Lubrizol will help the company in getting its supplies secure and as well as will attract more distributors towards company

Expansion into South India with Telangana Plant and focus on east india in coming years may keep the growth rate intact

Data-driven pull against conventional push is the new sales strategy of the company for the retail segment. Business-to-business (B2B) remains an area of improvement where PPF sees ocean of opportunities. It has moved into technology driven plumber data to move into B2B business as well as for normal business

Risks

Raw Materials Prices: Raw materials (resin) are derived from crude oil and any increase in crude oil price can hurt margins in short term.

COVID Lock-downs: Second wave of COVID, many states have had to announce lock-downs, although this time plants were not completely shut but still first quarter at least, could be dampner.

Corporate Governance Issues: There have been allegations of inadequate disclosure in the IPO prospectus of PPF PPF did not disclose all litigations, claims and criminal proceedings against the promoters (although re-filed DHRP corrected anamolies but still some differences are claimed)

No moats and No barriers to entry in this business

Fake / duplicate products can hurt company business

Exit Strategy

COVID-19 third wave creating more havoc than 2nd wave can impact the company balance sheet in big way for construction and this should be on radar

Break up with Lubrizol will definitely hurt the company and we need to relook if such thing happens in future

Any negative change in Govt policy for water schemes can hurt the growth prospects and may warrant an exit

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Clean Science and technology IPO– Incorporated in the year 2003, fine and specialty chemical manufacturing company, with innovative chemical processes developed in-house. Clean Science and Technology is a family-owned business and work primarily on developing clean and eco-friendly manufacturing processes.

Business — Clean Science Technology manufactures functionally critical specialty chemicals such as performance chemicals, pharmaceutical intermediates and FMCG chemicals. Its products are used as key starting level materials, as inhibitors, or as additives, by customers, for products

Region of operation — Customers include manufacturers and distributors in India as well as other international markets including China,

Europe, the US, Taiwan, Korea, and Japan. Approx. 66% of the company’s revenues come from exports

Offer purpose — The IPO is 100% Offer For Sale (OFS) . None of the proceeds will flow to the company

Risks —

Company will not get anything from IPO for future expansion etc

Highly competitive industry and well established peers

High dependence on exports

Strength

Globally leading supplier of certain chemicals; Ansole, 4-MAP, MEHQ, BHA, DCC, etc.

Strategically located manufacturing facility with close proximity to JNPT port to export products.

Strong long-term relationship with key customers.

Consistent track record of financial performance.

International presence with export to several countries i.e. China, USA, Korea, Japan, Taiwan, etc.

Future

Company has been growing well and automated operations, continued focus on product identification, process innovation, catalyst development, significant scale of operations as well as our measures towards strategic backward integration have all contributed to its success as one of the fastest growing and among the most profitable specialty chemical companies globally .

Valuations

Valuations are little on higher side and compare well with peers

Should we apply?

People can subscribe for long term and keep on adding on dips & review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

KIMS IPO– Incorporated in the year 1973, KIMS is one of the largest corporate healthcare groups in Andhra Pradesh and Telangana in terms of patients treated and treatments offered.

Business — The Hyderabad-based hospital chain offers multidisciplinary healthcare services with primary, secondary, and tertiary care across 2-3 tier cities, and an additional quaternary healthcare facility in tier-1 cities.

Region of operation –Main presence in 2 states , Telagana and Andhra Pradesh

Offer purpose — The IPO includes a fresh issue of Rs 200 cr and an Offer For Sale (OFS) of up to 2.35 cr equity shares by the promoters and existing shareholders. This includes roughly 1.6 cr shares by the biggest investor in the company – General Atlantic Singapore KH Pte. for prepayment of borrowings and general purposes

Risks —

Extremely high level of dependency on top 10 doctors

Concentrated region of operation

ARPOB is on the lower side as compared to industry numbers

Strength

Multidisciplinary healthcare services with primary, secondary, and tertiary care across 2-3 tier cities at afforable rates

Better cost operating profile wrt peers due to operational leverage

Strong Balance sheet and operating margins

KIMS has expanded its business by successfully completing 4 significant acquisitions from FY 2017-2018 to FY 2019-2020

Future

Company has plans to expand number of beds and expanding in Chennai and Bengaluru in coming years that will help the growth

As hospital chain becomes more mature, EBITDA margin will improve further

Valuations

Valuations are reasonable and compare well with peers

Should we apply?

People can subscribe for long term and keep on adding on dips & review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Dodla Dairy IPO– An integrated Dairy company based in south India , 2nd largest in terms of milk procurement, 3rd largest in terms of presence among private dairy companies

Business — Sale of Milk and Milk based Value Added Products(VAP)

Revenue segments — 73% from processed milk, 27% from VAP

Region of operation –Main presence in 5 states of south India,overseas operation in uganda and kenya

Offer purpose — Fresh issuance of equity shares worth up to ₹50 crore and a ₹470 crore offer for sale by existing shareholders for prepayment of credit, capex and general purposes

Risks —

Low margin business

Highly competitive business with unorganised players chasing same customers

Strength

Diversified nature of products portfolio

Strong distribution netwrork

Strong Brand presence in southern region of India

Future

How they expand and grab market share in highly competitive industry determines their growth

Any addition of VAP and increase in revenue from VAP may lead to good growth

Valuations

Valuations are bit on higher side

Should we apply?

People can avoid and look at listed peers instead

One can wait to enter at low prices for investment purposes and review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Shyam Metalics IPO– Shyam Metalics and Energy Ltd (SMEL), company in a cyclical business

Business — An integrated metal producing company with focus on long steel products and ferro alloys

~50% business comes from finished steel

Offer purpose — Fresh issuance of equity shares worth up to ₹657 crore and a ₹252 crore offer for sale by existing shareholders.

Risks —

Being in a cyclical industry is the biggest risk

Commodity cycle if dies down early may inflate the risk

Strength

Diversified nature of product portfolio

Low debt with effective cost control measures

Future

Company plans to double finished steel capacity but that’s still 3 yr away

Any slowdown in coming years in commodity cycle may cause the company financials to go bad

Valuations

Although no direct peers, but valuations are not cheap

Should we apply?

People can only subscribe for possible listing gains only

Recommended to sell if getting 10-30% gains on listing day

One can wait to enter at low prices for investment purposes and review holdings with each quarter earnings

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Sona BLW Precision forgings IPO– one of leading automotive technology companies in India and among top 10 globally for differential level gear segment.

Business — Designing, manufacturing and supplying differential assembly, gears, conventional and micro hybrid starter motors

~75% business comes from exporting

Offer purpose — Offer of 5550 cr for debt prepayment and exit of one of PE investors

Risks —

High valuations

Most of EV related business form one customer and client concentration risk for ~60% revenue from top 5 customers

Strength

Company has diversified business revenue mix in terms of geography, vehicle segment, powertrain and products

With about 40 per cent of its revenues from hybrids (mostly micro hybrids) and EVs, the company is a play on the growing market for cleaner vehicles across the globe

Future

Electric drive motors and inverters to Sona BLW’s existing product line of differential gears and assemblies for electric vehicles (EVs) has been added after the acquisition of comstar few years back

The expected change in product mix is value adding for the company as revenue realisations (and hence, profitability) for differential assemblies generally move up as the powertrain shifts from combustion to full hybrids and EVs.

Valuations

Very expensive looking at last results

As consolidation and revenue mix changes, may become available at decent valuations

Should we apply?

People can ideally avoid and if one subscribe, then do for possible listing gains only. If no listing gains then may need to hold longer

Recommended to sell if getting 10-20% gains on listing day

One can wait to enter at low prices for investment purposes after listing

Also Read

Burger King IPO crisp Summary — Listing with huge gains as shared

CAMS IPO crisp summary — Listed with 20% gains as shared

Happiest Minds IPO crisp summary –Listed with substantial gains as shared

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

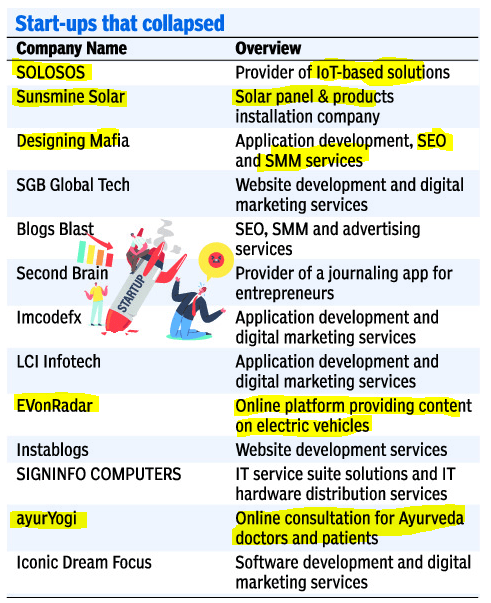

Some interesting names which are working on current themes like IoT , Ayurveda, SEO, EV content