Author: Its real ALPHA

#Investor # Reader #Marathoner #Cyclist #Foodie #Traveler

#Helping people in Finances

Protected: Alpha Electric Portfolio — 300122

Protected: Premium Stocks : 30-Jan-2022

TVS on prowl

ICRA : How economic environment looks like

Tailwinds and no technology risk!

An insight into SaaS company

Disclaimer – Below Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Rate Gain Travel Technologies

Incorporated in 2004, Rategain Travel Technologies Ltd (RTTL) is a ‘software-as-a–service’ (SaaS) company offering distribution, marketing and revenue maximisation solutions for the hospitality and the travel industry. It is one of the leading distribution technology companies globally and the largest Software as a Service (SaaS) provider in the travel and hospitality industry in India.

Business —

It offers a suite of interconnected products that manage the revenue creation value chain for customers by leveraging big-data capabilities and integration with other technology platforms helping hospitality and travel providers acquire more guests, retain them via personalized guest experiences and seek to maximize their margins. The company serves a large and rapidly growing total addressable market.

RTTL’s mission is to be the leading revenue maximization platform for the hospitality and travel industry. It offers an integrated technology platform powered by artificial intelligence enabling customers to increase their revenue through customer acquisition, retention and wallet share expansion. COVID-19 has, however, accelerated the digitization of customer interactions with hospitality and travel companies. These changes are likely to lead to a shift by hospitality and travel companies from in-house solutions to third party software and services.

RateGain Travel delivers travel and hospitality technology solutions through the SaaS platform through 3 business units; 1. Data as a Service (DaaS), 2. Distribution, and 3. Marketing Technology (MarTech).

DaaS –It equips suppliers with data and information to increase acquisition and conversion. It offers data under two categories: Market Intelligence, which provides access to pricing and availability data at scale along with analytics to present trends, opportunities and market developments. Dynamic Pricing Recommendations, to serve certain segments with proprietary dynamic pricing technology to help maximize revenue.

For DaaS products, it operates on a subscription model where its customers in the hospitality sector subscribe to DaaS products such as Optima and Parity for a period. Its competitive intelligence products tracked points such as pricing, ratings, rankings, availability, room descriptions, cancellation policy, payment policy, discounting and package inclusions.

Distribution — It provides mission critical distribution including availability, rates, inventory and content connectivity between leading accommodation providers and their demand partners. Distribution also enables delivery of reservations back to hotel systems to ensure smooth operations and accurate reporting by hotels.

In its Distribution segment, it operates RezGain on a subscription basis where customers pay a subscription fee to access the product while DHISCO operates on a transaction model where it generates revenues from bookings done by OTAs and Global Distribution System operators

Martech — Its MarTech offering enhances brand experience to drive guest satisfaction, increase bookings and increases guest loyalty. It also manages social media for luxury travel suppliers allowing them to be responsive to social media engagements 24×7 as well as effectively manage their social media handles and run promotional campaigns

END USER INDUSTRIES — Growing industries in coming decade

- Hotels,

- Airlines,

- Online travel agencies (OTAs),

- Meta-search companies,

- Vacation rentals,

- Package-providers,

- Car rentals,

- Rail,

- Travel management companies,

- Cruises and

- Ferries.

Customers and Competitors–

Six Continents Hotels, Inc., an InterContinental Hotels Group Company, Kessler Collection, a luxury hotel chain, Lemon Tree Hotels Limited and Oyo Hotels and Homes Private Limited. It also counts 1,220 large and mid-size hotel chains, 110 travel partners including airlines, car rental companies and large cruise companies and over 132 distribution partners including OTAs such as GroupOn and distribution companies such as Sabre GLBL Inc., in over 110 countries as its customers

Moats —

Innovative Artificial intelligence-driven industry-relevant SaaS solution provider.

Leading distribution technology companies globally and the largest Software as a Service (SaaS) provider in the travel and hospitality industry in India.

Any other SaaS players will take time to break into this company niche market segment

Strengths

A large and rapidly growing addressable market opportunity for a vertical-specific platform kind of company

The travel technology segment is backed by industry tailwinds of digitization in the post COVID times.

Diversified clientele portfolio has helped accelerate growth and in innovating and thus retain both new and existing customers

Diversified esteemed clientele, RTTL served 1,462 customers including eight Global Fortune 500 companies till 30sep2021

Diverse and comprehensive portfolio of revenue maximization and business critical solutions

Strong financial performance with track record of successful acceleration post acquisitions

Innovative Artificial intelligence-driven industry-relevant SaaS solution provider.

Shareholding

Promoter has sufficient skin in game with holding ~67% and other prominent players holding 10% more. Bhanu Chopra is the chairman and managing director (CMD) of RTTL. He founded the company in 2004 and has been leading it since then. He was previously associated with Deloitte and he holds a BS in Business from Indiana University.

Some triggers and updates from recent press releases

Recognition in Industry with new customers

Recognition in Industry with best awards

Increase in Tourism Industry in coming years : Projections and online penetration

Getting along with Students for future

Update in H1FY24 results

Showing important traction in customers, employees increase + down in attrition and increasing contracts wins

Promoters skin in game + Other participants like FII , DII are also increasing in recent times, in Public domain, major chunk with Plutus wealth management

AUG24 Update

Cash flows, Sales, Profits all have improved in 2024

Big money from FII and DII have entered

Technicals on 27th Aug24

Risks (tried to see major risks, please do due diligence to understand more on this part)

Badly affected by Covid-19 in terms of financials. May take time to recover fully and if more variants of Covid-19 appear, it can further delay the cause

Intensive competitive sector both at Domestic and International level. Continuous adaption is the key

Another risk could be the change in channel of distribution. Many client if develop their own software may lead to business kill for company

Valuations —

They have to be seen in terms of huge growth runway available with adaption to digital and highly competitive sector.

Once Covid resides, this could be the one company which gets off the block faster. So need to track on acquisitions, mergers, customers, new deals and financial improvement of company balance sheet

Your strategy can be different than mine. Your selection of company might be different than mine. So lets not be a BLIND FOLLOWER

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It is for educational purpose and it can be used for educational purposes further. There could be lot of things which might have been missed in my analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

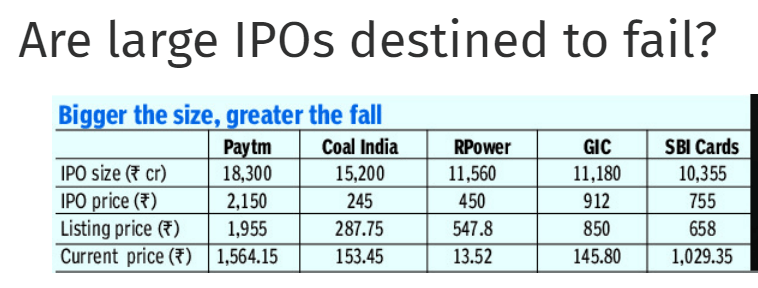

Hot Potatoes : Free fall in many recently listed IPO

Protected: Positional Stocks – 23-Jan-2022

Protected: Alpha Electric Portfolio — 230122

Finoetex chemicals

Protected: Alpha Learners B42

Protected: Premium Stocks : 16-Jan-2022

Protected: Positional Stocks – 16-Jan-2022

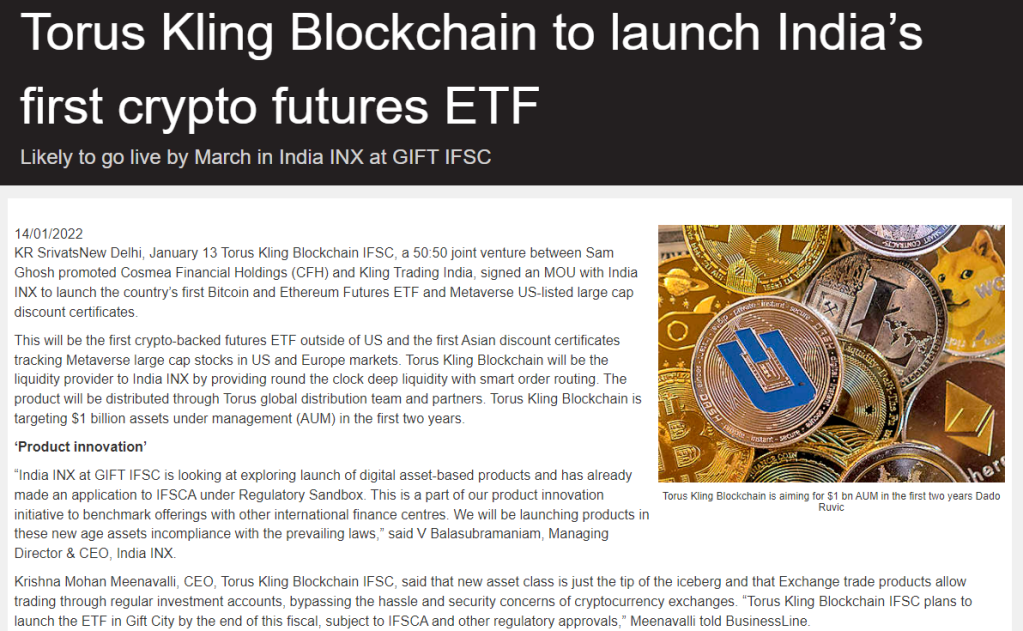

India’s first crypto futures ETF

3 years down the line

Protected: Alpha Electric Portfolio — 140122

Do you have time to make mistakes!! Learn from others learnings

Three by Three

Small Insight into Infra Company

Likhitha Infra (approx 33 yr old company) is an Oil Gas Pipeline Infrastructure provider in India. Operations include Cross Country pipelines and associated facilities, City Gas Distribution including CNG stations, and Operation & Maintenance of CNG/PNG services.

Strong presence in more than 16 states and 2 Union Territories in India.

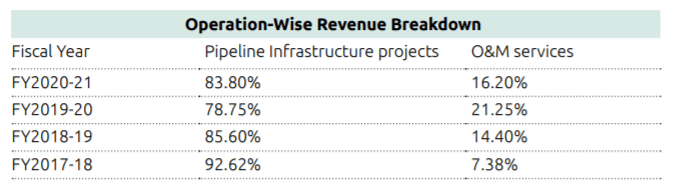

Two major domains, if we divide the operations , are Pipeline Infrastructure Projects and O&M services (Operation and Maintenance)

Revenue breakdown for the domains are highlighted below (for last 4 Financial years)

Strengths

Long standing relationships with domestic marquee customers.

Efficient business model

Strong project execution capabilities

Diversified geographical presence in India

Strong Technical Qualification to bid for new projects

Strong promoter holding showing skin in game

Good ROCE, stable and improving PAT margins and EBITDA

Highly experienced Management Team

Triggers for company in coming quarters

CGD is increasing in India and company is at right place for its business to grow with Strong client base and on top of that company has Strong Technical Qualification to bid for new projects which is visible in orders won recently

Company has received orders worth Rs. 250 Crores (approx.) excluding GST from various City Gas Distribution Companies during the

quarter from October 2021 to December 2021.

Till Aug. 2021 company has an outstanding order book of 1020 cr giving good revenue visibility. In Oct-Dec 2021 , company received 250cr of additional orders

As per the recent Government policies, PNGRB has increased the number of Geographical Areas (GAs) to 228 comprising of 402 districts spread over 27 States and Union Territories, covering 70% of Indian population and 53% of its area. These recent Government initiatives have provided lucrative opportunities for Oil & Gas infrastructure service providers

Recent policy moves, including a wide-scale rollout of CNG and the expansion of gas infrastructure including LNG terminals, long-distance transmission pipelines and city gas distribution networks, will help drive 30bnm³ of gas demand growth over the next decade through fuel switching away from coal and oil. A recent switch to CNG from coal in India’s brick industry is encouraging greater gas use.

Exit Triggers

Order chain drying up in coming quarters

Unforeseeable change in Government policies

Declining margins and increasing debtors or working capital cycle days

Risks

Any change in CGD policy

Much faster penetration of EV in coming 2-3 years

Rising raw material and commodity costs

The Company is deriving significant portion of orders from major Oil & Gas distribution companies inducing a client concentration risk

Insight into Vishnu Chemicals

Vishnu Chemicals Limited is a market leader in manufacturing and sales of Chromium chemicals and Barium compounds across the world

Serving 12+ industries across 50+ countries (83 countries as per publicly available information)

Chromium Chemicals –>

~85% revenues (FY21) , Leading manufacturer in India as well as South Asia,

FY21 Domestic: Export Sales Mix: 51:49 , 3 manufacturing units

Over the last few fears, the company has diversified its Chromium revenue profile with presence in both domestic and export markets. Earlier the portfolio was concentrated in chromium, domestic oriented and now diversified and balanced geographically in domestic and export markets

Applications –> Pharmaceuticals, Leather tanning, Pigments and Dyes, Plastic masterbatches, Ceramic glazes, tiles, Electroplating, Automotives, Refractories, Wood Preservative, Paper pulping and others.

Barium Chemicals –>

~15% revenues (FY21), Leading manufacturer in India, FY21 Domestic: Export Sales Mix: 45:55 ,1 manufacturing unit.

Applications –> Ceramics, tiles, glazes, bricks, refractories and water purification chemical in caustic soda industry, speciality glass, Luminescent Compounds, etc.

Strengths

Long standing relationships with domestic and overseas marquee customers.

Well diversified board with specialists in field

Certifications — ISO 9001:2015 , ISO 14001:2008, REACH Quality Certification

Income, EBITDA, PAT, PAT Margin improving

D/E is high but decreasing as desired

Ability to pass the rise in input prices and freight costs.

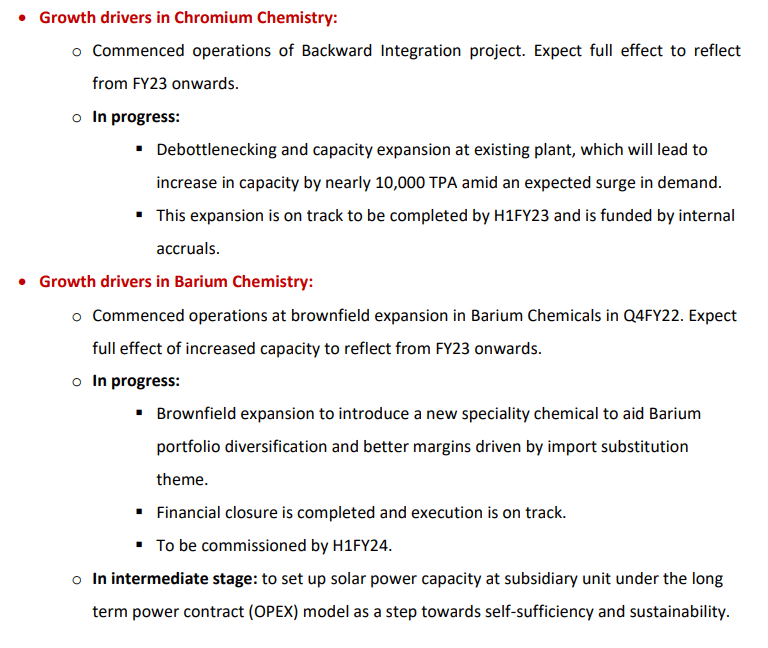

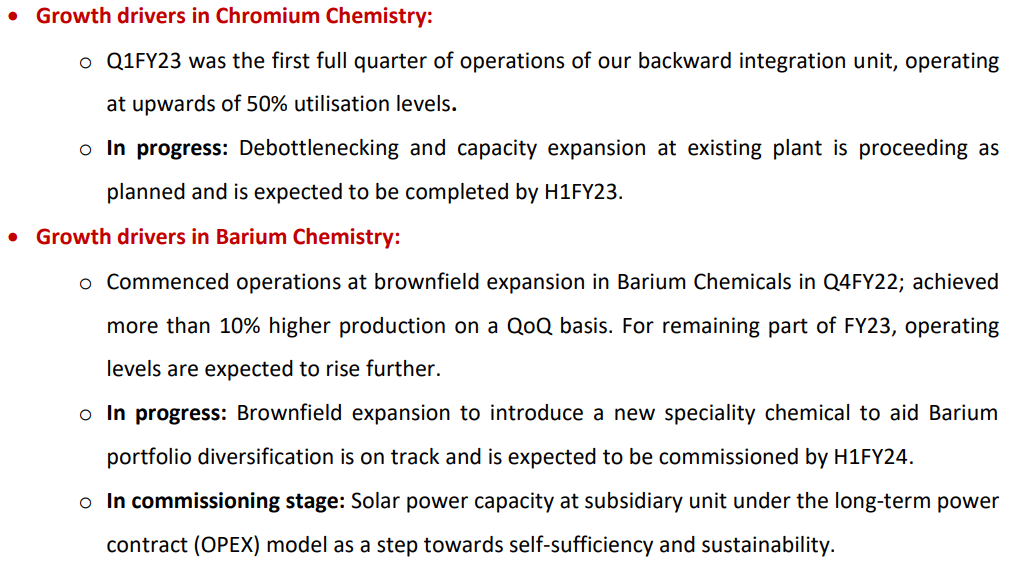

Triggers for company in coming quarters

Operating leverage: Most of the overheads or manpower addition are largely done considering FY21 as a base.

Higher utilizations from existing capacity: Major debottlenecking completed in Vizag unit in FY21 will lead to better throughput & efficiency

Majority of the capital expenditure towards sodium carbonate in Chromium chemicals is completed, Majority of company’s sodium carbonate’s current requirement will be met through the process. Significant cost reduction expected from upon being operational by Q4FY22E.

Focus is to increase market share with higher volumes in Barium chemicals

Leading manufacturer in India for Barium Chemical : Other players have less than 1/10th of Vishnu’s current capacity.

Incremental capacity of 20,000 TPA of Barium Carbonate expected to be operational by Q4FY22E

China plus 1 strategy has made them a preferred vendor instead of being a second option for their customers.

Exit Triggers

Crash in finished products prices or inability to pass on raw material in coming quarters

Any change in China +1 strategy for customers

Less than expected utilization of incremental capacity

Risks

Debt profile is still out of comfort zone

ROCE and PAT Margin still not as much as desired

Any Exports oriented issues including currency risk, freights costs

Significant promoter pledge of 40%

Any delay in operations of underway capacity expansion

Protected: Alpha Electric – 100122

Protected: Positional Stocks – 10-Jan-2022

Protected: Alpha Learners ACCD

Protected: Alpha Learners MF

Protected: Alpha Learners 18

Flying EV sales : Future looks here

Cryptowire index of Cryptocurrencies

Inspection as a Service (IaaS)

Protected: Premium Stocks : 02-Jan-2022

Protected: Alpha Electric – 020122

Protected: Alpha Learners Class17

HAPPY NEW YEAR 2022

HAPPY NEW YEAR to ALL

CHALLENGE YOURSELF to CHANGE YOURSELF!!

Let this year be the BEST in Personal, professional life and in Fitness n Finance

Target big always

,

Take

in your strides

Keep Moving, Even a slow mover will beat standstill by handsome margin

Sodium-ion : Faradion and Reliance

Flex Fuel Vehicles (FFV) : Unrealistic timelines

Vikas of NPA underway!!

Aatmnirbhar version : PLI Semiconductors

ALPHA LEARNERS – Mentorship program Jan22

With great pleasure and best wishes from all of you, we are delighted to launch

ALPHA Mentorship program

ALPHA LEARNERS

Art and Science of Investing

to make you Independent in stock markets

A PROGRAM TO MAKE YOU LEARN AND EARN

This is a unique live program for approx. 5 months (on weekends) Where one can learn necessary

Fundamental Qualitative concepts to understand the things which create wealth in long run–like how to evaluate management, how to evaluate certain corporate actions, how to understand direction of company

Fundamental Quantitative concepts to substantiate what we have seen qualitatively, understanding ratios and numbers like margins and numbers like EBITDA, PAT, OPM, Financial Ratio, Valuation ratios PE, PB, PS, EVEBITDA, ROE, ROCE, Debt, equity and many other deep ratios to understand whether stock at right price or not

Learn about cost of capital, working capital cycle, inventory turnover, asset turnover, interest coverage, pledging(good or bad)

Why Dividend is good or bad

How long we can hold a stock or when to leave the stock

Capex, opex and how it impacts and when it impacts

Why certain high pe stocks keep on running and low pe stocks remain down

Red flags and green flags

Necessary Technical aspect to make our entry and exit better in stocks ,oscillators and indicators including RSI, MACD, STOC RSI, EMA, TEMA, DEMA, Trends, SL

Technical aspect and understanding of Price Volume action, candlestick patterns ( bullish, bearish, single, double, triple patterns)

Technical understanding of Targets from different patterns, How to look for patterns and when to look for which pattern

Resources to analyze faster to analyze more companies faster

Understand Contrarian, Cyclical, Value and Growth investing

Bucket and GRADE Framework

Business Moats understanding–how to categorize moats, what is real moat, what is fake moat

Exit Strategies in stocks

Reading Balances sheet in simple way to analyze results and issues to make quick exits or to do pyramiding after results

Reading Cash flows in simple way to understand where money is being moved in company

Reading Quarterly, half yearly, yearly results and interpreting them better

Tricks and Checklist for faster analysis of Annual Reports to help us all understand whether to deep dive or not

Conf-call understanding, Transcripts Concepts and Tricks to understand faster

Big money moves aspect to understand where money is moving

Concepts and tricks on various intricacies in stock market

Understanding about primary, secondary market

Also get a KNOWHOW on

Checklist for stocks to identify red flags faster

Checklist for deep dive into selected stocks

How to build Portfolio for Short term

How to build Portfolio for Long term

How to find Multi bagger stocks

How to avoid pitfalls in market

When to exit stocks

Concept of Futures and options

4 Bonus sessions from experts (apart from Program content)

Mutual Funds

Financial planning

IPO and

Accumulation Distribution session

3-4 months of teaching and mentoring

Can be extended based on queries, case studies1-2 months of handholding

To clear doubts, correction of mistakes, independent walking in markets

10+ Assignments

Based on actual events happening in markets during the course

Case studies

Based on future growth understanding and pitfalls to avoid

Quizzes

To help you assess yourself whether you are progressing or not during the programPresenting Stock idea by Learners to bridge the learning gap

This is a program YOU CAN NOT AFFORD TO MISS

LET THIS NEW YEAR 2022 be the start of your journey towards INDEPENDENCE IN STOCK MARKETS

ACT NOW for your Independence

CONTACT us

AVAIL EARLY BIRD OFFER till 1st Jan 2022

ACT NOW for your Independence

FEEDBACK By Ongoing ALPHA LEARNERS

CONTACT us

Number of batches and batch size is very very limited considering live classes

Major part of this initiative will go towards orphan children education and food

Do make use of this opportunity and be part of bigger initiative

Connect with us to help genuine needy children

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

FAME-II Going strong

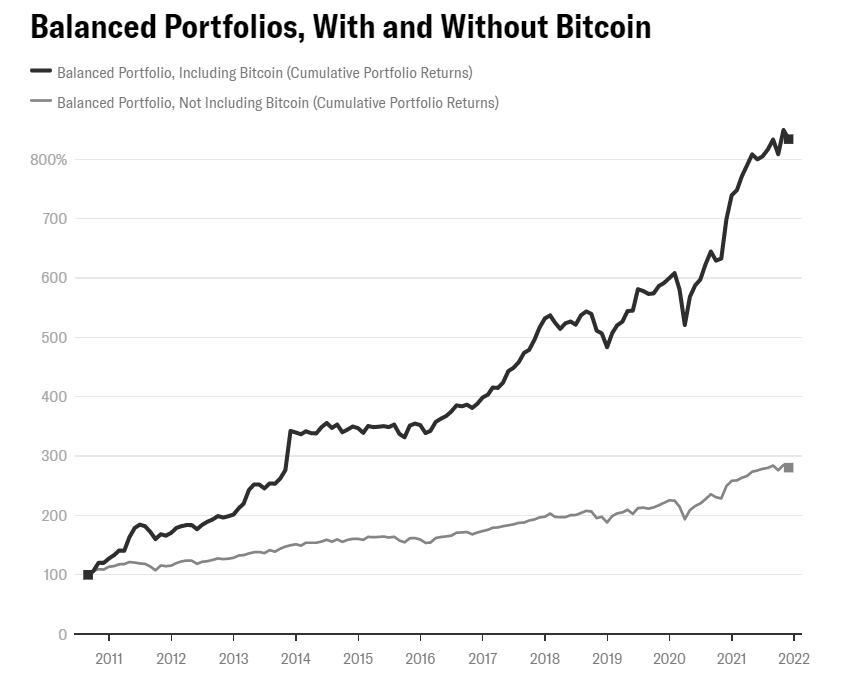

Balanced Portfolio with and without Bitcoin

Biggest Revolution in Power electronics in 30 years

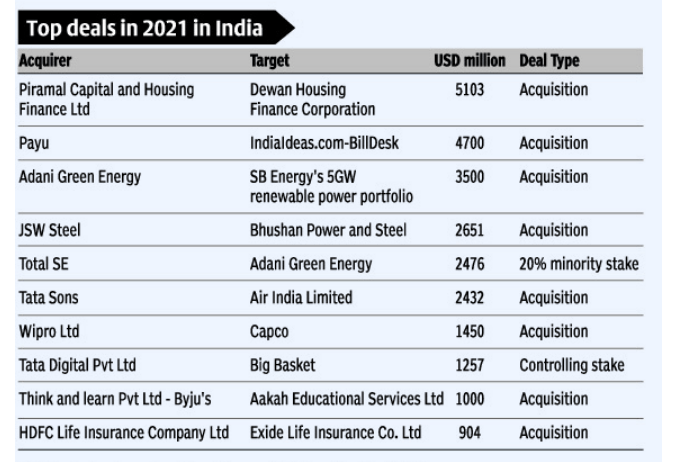

Top Deals in 2021

Protected: Alpha Learners class

Porous Liquid and CO2

Crypto Super App : Cryptowire

TVS BMW EV

Aatmnirbhar version : PLI Semiconductor

Blockchain Protocols

Satellite Broadband

Protected: Alpha Learners session15

Protected: Positional Stocks – 11-Dec-21

Medical devices : Aatmnirbhar Version

What’s Hot : It’s SaaS

NO DIVIDENDS

Tega Industries IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Tega Industries IPO — Established in 1976, Tega Industries is a leading manufacturer and distributor of specialized, critical, and recurring consumable products for the global mineral beneficiation, mining, and bulk solids handling industry.

Business and Key areas of Operation -Tega industries are the second largest producers of polymer-based mill liners. The company offers a wide product portfolio of specialized abrasion and wear-resistant rubber, polyurethane, steel, and ceramic-based lining components used by their customers across different stages of mining and mineral processing, screening, grinding, and material handling. The company’s product portfolio comprises more than 55 mineral processing and material handling products.

The company has 6 manufacturing sites, including 3 in India, and 3 sites in major mining hubs of Chile, South Africa, and Australia. Majority of the company’s revenue (86.42% in 2021) comes from operations outside India. The company has 18 global and 14 domestic sales offices located close to its key customers and mining sites.

Also READ : DMR HYDRO IPO : SUBSCRIBE OR NOT

Also Read : Latent View IPO : BUMPER LISTING

Also Read : Tarsons Products IPO : BUMPER LISTING

Offer purpose — The issue consists of a offer for sale of 619 Cr.

Risks —

Entire money is offer for sale, Company will not have any access to money raised

Strength

One of the world’s largest producers of polymer-based mill liners

Products cater to after-market spends providing recurring revenues

In-house R&D and manufacturing capabilities and a strong focus on quality control

Global customer base, and strong global manufacturing and sales capabilities

Consistent market growth and operational efficiency

Experienced management team supported by a large, and diversified workforce

Future

Tega Industries are further expanding their operations in major markets including North America, South America, Australia, and South Africa.

Valuations

Valuations are on higher side as expected in bull market

Should we apply?

For medium to long term, prospects looks ok

Wait for listing to buy

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Star Health IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Star Health IPO — Incorporated in 2006, Star Health and Allied Insurance Company Ltd is one of the largest private health insurers in India with a market share of 15.8% in Fiscal 2021.

Business and Key areas of Operation – The company primarily focuses on the retail health and group health segments which accounted for 89.3% and 10.7% of the company’s total GWP in Fiscal 2021 respectively. The company mainly distributes policies through individual agents and also includes corporate agent banks and other corporate agents. As of Sep 31, 2021, its network distribution includes 779 health insurance branches across 25 states and 5 union territories in India. Star Health has also built one of the largest health insurance hospital networks in India with more than 11,778 hospitals.

Also READ : DMR HYDRO IPO : SUBSCRIBE OR NOT

Also Read : Latent View IPO : BUMPER LISTING

Also Read : Tarsons Products IPO : BUMPER LISTING

Offer purpose — The issue consists of a fresh equity issue of 2000 Cr and offer for sale of 5250 Cr. Offer is to augment its capital base

Risks —

In Short term , Increasing Covid-19 is a major risk. In Long term, any such major disease can be a risk

Strength

Largest private health insurance company in India with leadership in the attractive retail health segment.

Largest network distribution in the health insurance industry.

Diversified product suite with a focus on innovation and specialized products.

Strong risk management with superior claims ratio and quality customer services.

Demonstrated track record of operating and financial performance.

Future

Company is working in an underpenetrated but highly competitive sector

Valuations

Valuations are pricey, better options in secondary market

Should we apply?

For medium to long term, prospects looks ok

Wait for listing to buy at discount to IPO price

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

PLI scheme : Pharma

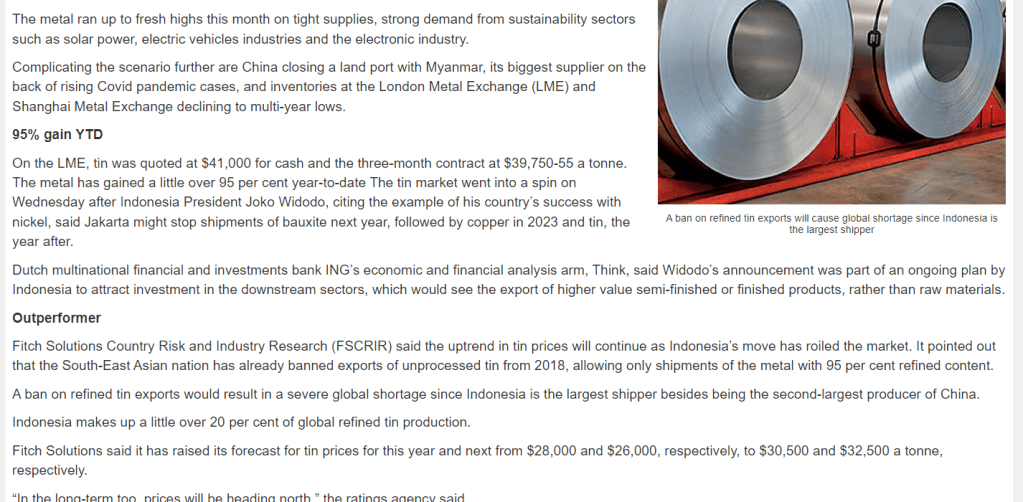

Tin prices : North is the direction

Protected: Session 13

Protected: Session12

DMR Hydro IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

DMR Hydro SME IPO Business — DMR is engaged in providing engineering consultancy and due diligence services to hydropower, dams, roads, and railway tunnels. The services offered by the company include the entire life cycle of projects covering design & engineering, due diligence & regulatory, bid management & construction engineering, and quality & inspection

Key areas of Operation -Company has been working into renewables, water resources, mining, and urban infrastructure domains. The company has a presence across 11 states in India. Internationally the company provides services to over 5 countries including Nepal, Nigeria, Dubai, Germany, and Senegal.

Also READ : NYKAA IPO : SUBSCRIBE OR NOT

Also Read : Latent View IPO : Subscribe or NOT

Offer purpose — The issue consists of a fresh equity issue of 798000 shares and offer for sale of 198000 shares. Offer is to Fund working capital requirements and General corporate purposes

Risks —

SME company so liquidity risk is a major risk

The company is operating in a highly competitive and fragmented segment. There are many big players as well

Strength

Presence in both domestic and international markets

A wide offering of engineering consultancy and due diligence services

Experienced management and dedicated employee base

Catering to diversified sectors

Accredited with various quality certificates

Future

Company is working on areas for consultancy which are kind of good for future. Sustainability of margins could be thing to look for

Valuations

Valuations are reasonable looking at future. In short term, Price looks at par

Should we apply?

For medium to long term, prospects looks ok

People having risk apetite and long term vision can apply if they can held this stock patiently as liquidity can be low after listing

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Protected: Session12

Protected: Session11

Protected: Premium Stocks : 21-nov-21

Protected: Positional Stocks – 21-nov

DRIFE : Blockchain-driven ride-hailing platform

IPO losses on listing day

Mint

Large IPO and Failures : Deadly combo

GoColors IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

GoColors IPO– Incorporated in 2010, Go Fashion (India) Limited is one of the largest women’s bottom-wear brands in India.

Business — The company is engaged in the development, design, sourcing, marketing, and retailing of a range of women’s bottom-wear products under the brand, ‘Go Colors’. The company offers one of the widest portfolios of bottom-wear products among women’s apparel retailers in terms of colors and styles.

Way of Operation – Company has 450 exclusive brand outlets (EBOs) that are spread across 23 states and union territories in India. The company’s distribution channels include large format stores (LFSs) including Reliance Retail Limited, Central, Unlimited, Globus Stores Private Limited, and Spencer’s Retail among others. The company’s LFSs have grown from 925 LFSs in 2019 to 1,332 LFSs in May 2021. The company also sells its products through its website, online marketplaces, and multi-brand outlets (MBOs).

Also READ : Tarsons Products IPO : SUBSCRIBE OR NOT

Also Read : Latent View IPO : Subscribe or NOT

Offer purpose — To part finance its plans for funding roll out of 120 new EBOs (Rs. 33.73 cr.), working capital (Rs. 61.40 cr.) and general corporate purpose, IPO has planned by company

Risks —

Highly competitive business

Third party contracts is a risk

Strength

One of the largest women’s bottom-wear brands in India

Wide, well-diversified, product portfolio and first-mover advantage

Multi-channel retail presence across India

Strong unit economics with an efficient operating model

Extensive procurement base and automated procurement & supply chain

In-house expertise in developing and designing products

Strong financial performance record

Future

Company is a pure long term story considering an expansion plan to increase outlets from 450+ to 2000+ in the coming five to six years plus its association with large format stores will bode well. Third party contracts may remain a risk

Valuations

Valuations are dicey as last two years Covid-19 plays havoc, though company was growing

Should we apply?

One can avoid and wait for company to perform and come back in positive territory

Risk takers can apply for listing gains(if any)

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

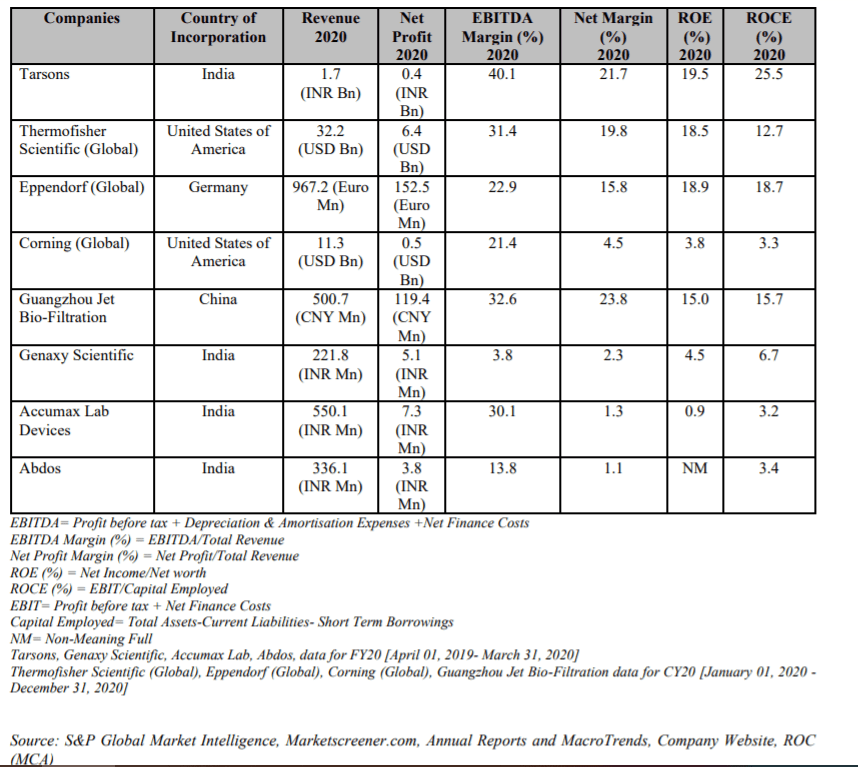

Laboratory equipment Market, leaders, margins : some key charts

Tarsons products IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Tarsons Products IPO– Tarsons Products Limited is a leading Indian life sciences company with more than three decades of experience in the production and supply of labware products.

Business — The company manufactures a range of quality labware products that helps advance scientific discovery and improve healthcare systems. The company’s product portfolio is classified into three broad categories including consumables, reusables. These Products are used in various laboratories across research organizations, academic institutes, pharmaceutical companies, Contract Research Organizations (CRO), diagnostic companies, and hospitals.

Region of Operation -Company has 5 manufacturing facilities located in West Bengal spread across approximately 20,000 sq. mts of area. The company has a strong distribution network across India comprising of over 141 authorized distributors as of March 31, 2021 and supplies its products to more than 40 countries.

Also READ : NYKAA IPO : SUBSCRIBE OR NOT

Also Read : Latent View IPO : Subscribe or NOT

Offer purpose — The IPO comprises a fresh issue of equity shares up to ₹150 crore and an offer for sale (OFS) of ₹850 crore by existing shareholders and promoters. Company is planning to use IPO for Repayment/prepayment of all or certain of company’s borrowings; Funding a part of the capital expenditure for new manufacturing facility at Panchla, West Bengal (proposed expansion) and General corporate purposes

Risks —

High Import dependency

Competition with MNC players

Environmental concern on Plastics

Regional concentration of plants

Strength

Leading supplier of life sciences products

Extensive product offering

Large addressable market of life sciences industry

Well-equipped and automated manufacturing facilities

Strong sales and distribution network

Experienced Promoter backed by a strong management team

Future

Company is vertically integrated and equipped with automated support systems that help the company in maintaining quality, increasing productivity, and reducing costs. Its key manufacturing facilities are ISO 9001:2015 and ISO 13485:2016/NS-EN ISO 13485:2016 certified. Company is poised for bright prospects ahead. It is expanding to meet the rising demand for its products.

Valuations

Valuations are reasonable looking at future. In short term, Price looks expensive

Should we apply?

For medium to long term, prospects looks bright with good set of customers and looking at no listed peers, may be advantage to subscribe

One must apply if they can held this stock patiently and not looking for immediate returns

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Protected: Session11

Protected: Positional Stocks – 14-nov

Protected: Session10

IPOs Top draws

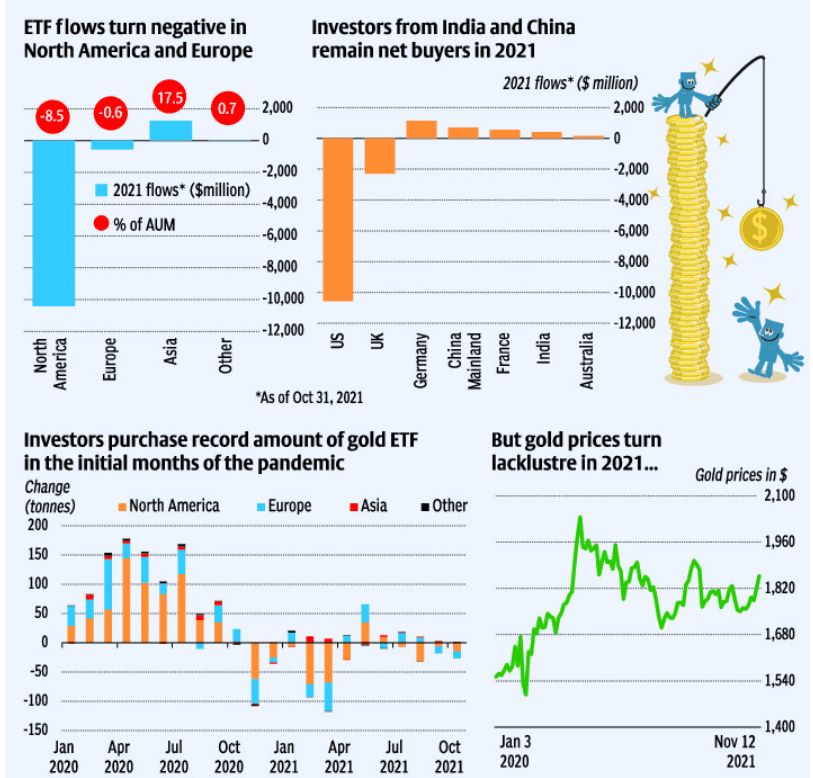

Gold ETF demand

Short term vs Long term

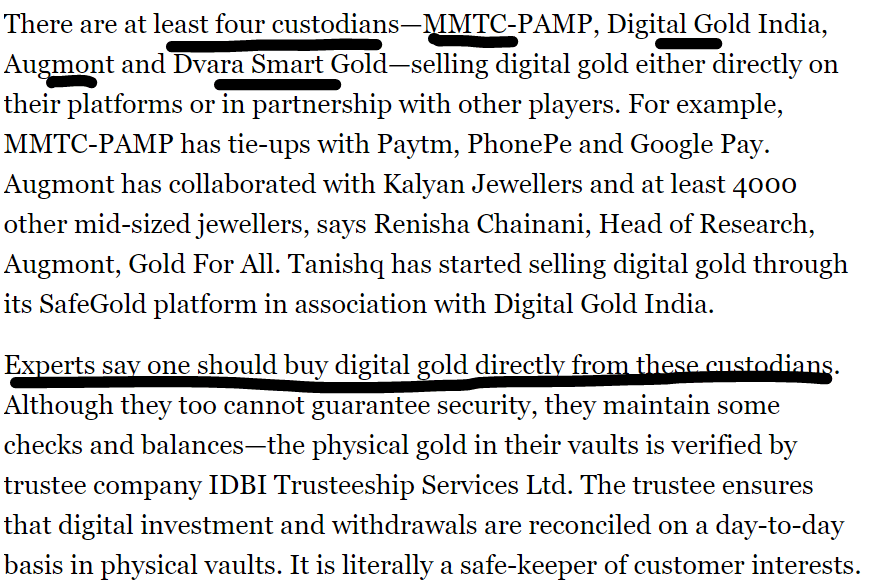

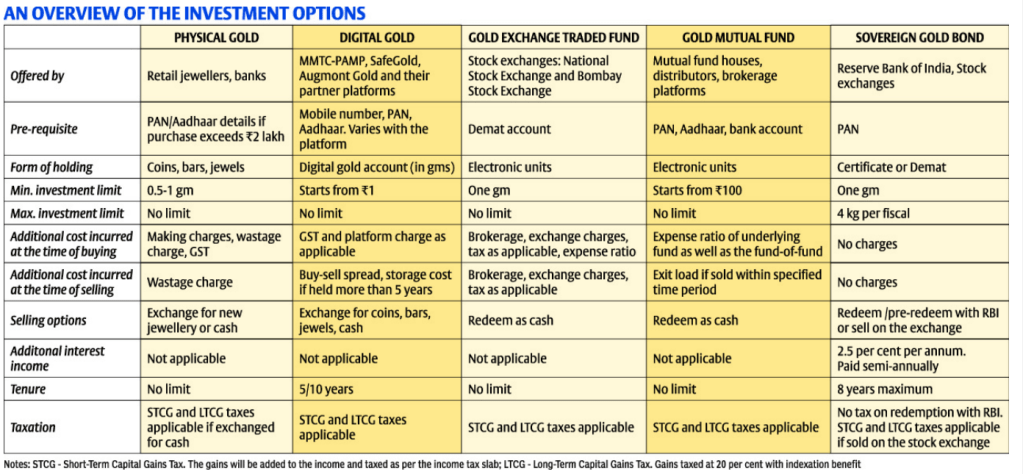

Digital Gold : BEWARE or BE AWARE

Covid-19 to INFLATION : Times are changing

Sapphire Foods IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Sapphire foods IPO-Sapphire Foods India is YUM brand’s largest franchise operator in the Indian subcontinent in terms of revenue as of FY’20. It is also Sri Lanka’s largest international QSR chain in terms of revenue for FY’ 2021 and the number of restaurants operated as of March 31, 2021. .

Business — Company owned and operated 204 KFC restaurants in India and the Maldives, 231 Pizza Hut restaurants in India, Sri Lanka and the Maldives, and 2 Taco Bell restaurants in Sri Lanka.The company has an in-house supply chain function and works with vendor partners for food ingredients, packaging, warehousing, and logistics. The company operates warehouses across 5 Indian cities and has invested in building technology solutions in their restaurants. The company operates its restaurants at high traffic and high visibility locations in key metropolitan areas and cities across India and develop new restaurants in new cities as part of its expansion strategy.

Region of Operation -It serves clients in India and Srilanka with KFC, Pizza hut and Taco bell outlets

Also READ : Latent View Analytics Limited IPO : Subscribe or NOT?

Offer purpose — The IPO comprises a complete offer for sale of 2000 cr. Proceeds will not go company

Risks —

Decreasing revenues from same stores

Operating losses continuing

High competition

Strength

One of India’s largest restaurant franchisee operators and Sri Lanka’s largest international QSR chain

YUM’s largest franchise operator in the Indian subcontinent in terms of revenue

Focus on delivering excellent customer experience

Quality control and operational excellence

Scalable business model

Experienced management team with robust corporate governance practices.

Future

Company has been working to reduce costs on multiple fronts like store size etc which is yet to show up in financials. Similarly Increasing delivery revenues and opening new stores, driving same store sales growth is a work in progress. Model is scalable and with demographic advantage, it should be able to sustain and turnaround over a long period

Valuations

Valuations are comparable to peers and lower wrt some peers in this bull marlet. Looking in isolation, valuations are not attractive though

Should we apply?

Long term investors need to wait and watch company progress before investing.

Risk takers can apply for IPO and exit on listing gains if any

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Alpha Bravo Charlie

Protected: Alpha Session10

Protected: Positional Stocks – 7-nov

One97 Communications IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

One97 Communications IPO– Incorporated in 2000, One 97 Communications Ltd is India’s leading digital ecosystem for consumers as well as merchants. As of March 31, 2021, the company has a 333 million+ client base and 21 million+ registered merchants to whom it offers payment services, financial services, and commerce and cloud services

Business — The company offers an entire digital ecosystem for its customers and merchants –ranging from payment services (money transfers, in-store payments, recharge, and bill payments), and financial services (digital banking including FASTag, PayTM Wallet and deposit accounts, loan or BNPL referral, wealth management and insurance). Generating revenue in the form of transaction fee, consumer convenience fee, and recurring subscription fee (from merchants), payment services comprises 62 per cent of the company’s consolidated revenues in FY21 and 4 per cent comes from cross selling financial services

Also READ : Latent View IPO : SUBSCRIBE OR NOT

Offer purpose —

- Growing and strengthening Paytm ecosystem, including through acquisition and retention of consumers and merchants and providing them with greater access to technology and financial services – ₹ 4,300 Crores, Investing in new business initiatives, acquisitions and strategic partnerships – ₹ 2,000 Crores and General corporate purposes

Risks —

Revenue scalability is the biggest risk as the RBI has restricted the transaction fees and commissions on various payment services to less than 1 percent. Already revenue drop is happening compared to last few years

Lot of uncertainty in digital share with lot of big players also joining the league ( like google, whatsapp etc)

Over diversified –Kind of deworsefication by company–not a clear path which will bring profit

Strength

India’s leading digital payment service platform.

Strong brand identity with a brand value of US$6.3 billion.

Large customer base with 333 million total customers, 114 million annual transacting users, and 21 million registered merchants.

Paytm Super-app to access a wide range of digital payment services over mobile phones.

Future

Company has been into multiple segments and can grow with digital payments and PayTM payments bank, MF business as well. But due to this scattered approach, no clear visibility which path company is taking. Road is long and uncertain.

Valuations

Valuations are extremely high, Founder skin in the game is really low

Should we apply?

AVOID

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

One97 Communications vs Foreign peers

Magical Central Bank

Latent View Analytics Limited IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Latent view IPO– Latent view is incorporated in 2006, Company provides services ranging from data analytics consulting to business analytics and insights, advanced predictive analytics, data engineering and digital solutions to companies in technology, BFSI, CPG and retail, industrials and other industries.

Business — Four Major domains -> (i) Consulting services (ii) Data engineering (iii) Business analytics (iv) Digital solutions

Region of Operation -It serves clients across the US, Europe, and Asia through its subsidiaries in the US, Netherlands, Germany, UK and Singapore.

Also READ : NYKAA IPO : SUBSCRIBE OR NOT

Offer purpose — The IPO comprises a fresh issue of equity shares up to ₹474 crore and an offer for sale (OFS) of ₹126 crore by existing shareholders and promoters. Company plans to use about ₹148 crore to fund inorganic growth initiatives, ₹130 crore for investment in subsidiaries and the remaining to fund working capital and general corporate purposes.

Risks —

Client Concentration

Regional Concentration

Technology disruption Risk

Strength

- One of the leading pure-play data analytics companies in India

- Extensive experience across a range of data and analytics capabilities

- Blue-chip clients across industries and geographies

- Focus on innovation and R&D

- Scalable and attractive financial profile

- Strong, experienced leadership team

Future

Company has created a niche place in data analytics services globally and It caters to Fortune 500 companies with long term relationships and it is also able to maintain healthy margins on its contracts

Valuations

Valuations are high

Should we apply?

Looks almost priced in at IPO price but for medium to long term, prospects looks bright.

One can apply if can held this stock patiently and not looking for immediate returns

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Non-Fungible Tokens : New Trend : Bachchan’s Edition

Its GOLD!!

SJS enterprises IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

SJS enterprises IPO –SJS is one of the leading players in the Indian decorative aesthetics industry. The company is a ‘design-to-delivery’ aesthetics solutions provider with a diverse product offering for the automotive and consumer appliance industries.

Business — The company’s product offerings include – decals and body graphics, 2D appliques and dials, 3D appliques and dials, 3D lux badges, domes, overlays, aluminum badges, in-mold labels, or decoration parts, lens mask assembly, and chrome-plated printed, and painted injection moulded plastic parts. The company’s subsidiary, Exotech, caters to requirements in the two-wheelers, passenger vehicles, consumer durables/appliances, farm equipment, and sanitary ware industries for chrome-plated, printed, and painted injection moulded plastic parts.

Offer purpose —

An offer for sale of Rs. 800 cr from existing promoters and stakeholders

Risks —

Massive dilution in IPO as offer of sale does not bode well

Maximum revenue coming from few client posing concentration risk

Short term revenue and profit risk is there

Also READ : Fino Payment Bank IPO : SUBSCRIBE OR NOT

Strength

Leading decorative aesthetics supplier with a wide portfolio of premium products

Strong manufacturing capabilities and established supply chain network

Innovative product designing capabilities

A strong relationship with global Tier-1 companies

Strong financials

Experienced and qualified management team

Future

SJS is a leading player in the Indian decorative aesthetics industry and scope of growth is there.

Valuations

The issue looks fully priced discounting all near term positives

Should we apply?

Avoid and wait for results for next 2-3 qtrs to see if company is able to perform as anticipated

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

PB Fintech IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

PB Fintech IPO– PB Fintech is India’s leading online platform for insurance and lending products. The company provides convenient access to insurance, credit, and other financial products

Business — Policybazaar is an online platform for consumers and insurer partners to buy and sell insurance products. 51 insurer partners offered over 340 term, health, motor, home, and travel insurance products on the policy bazaar platform, as of March 2021. Policybazaar offers its users with i) pre-purchase research, ii) purchase, including application, inspection, medical check-up, and payment; and iii) post-purchase policy management, including claims facilitation, renewals, cancellations, and refunds. The company has partnered with 54 large banks, NBFCs, and fintech lenders offering a wide choice of products to consumers across personal credit categories, including personal loans, business loans, credit cards, home loans, and loans against property.

Also READ : NYKAA IPO : SUBSCRIBE OR NOT

Offer purpose —

- For enhancing visibility and awareness of company’s brands, including but not limited to “Policybazaar” and “Paisabazaar”

- New opportunities to expand company’s consumer base including offline presence

- Funding strategic investments and acquisitions

- Expanding presence outside India and

- General corporate purposes.

Risks —

Till date the company has been posting negative earnings and can continue to do so in near term

Strength

Providing a wide choice and transparency to customers to research and select insurance and personal credit products.

Proprietary Technology helps in superior data intelligence and customer service.

Collaborative partnership with various companies for insurance and lending products.

Strong network effects for Policybazaar and Paisabazaar platforms.

High renewal rates.

Capital efficient model with low operating costs.

Experienced Founders and management.

Future

PBFL has two verticals of online business i.e. Policybazaar and Paisabazaar. With its novel technology-based initiatives, it has created a niche place. With network effects, company has a good scope to scale its business

Valuations

Valuations are really high and no listed peers to compare with as well

Should we apply?

Risk takers can put in IPO and exit with listing gains if any. Wait for significant dip to enter for long term as long term prospects are bright

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Protected: Positional Stocks – 31 Oct 21

Protected: Premium Stocks : 31-oct-21

FSN E-commerce Ventures (Nykaa) IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

FSN E-commerce Ventures (Nykaa) IPO –Incorporated in 2012, FSN E-commerce Ventures, the parent company of Nykaa, is a native consumer-technology company involved in selling beauty, wellness, personal-care and fashion products

Business — FSNEV has a diverse portfolio of beauty, personal care and fashion products, including owned brand products manufactured by it. As a result, the company has been established not only as a lifestyle retail platform but also as a consumer brand. It offers consumers an Omnichannel experience with an endeavour to cater to the consumers’ preferences and convenience.

Offer purpose —

Fresh equity issue worth Rs. 630.00 cr. and an offer for sale of Rs. 5351.92 cr,To meet its requirements of funds for investment in subsidiaries (Rs. 42.00 cr.), capital expenditure (Rs. 42.00 cr.), repayment/prepayment of certain borrowings (Rs. 156.00 cr.), brand visibility and awareness (Rs. 234.00 cr.) and general corporate purpose

Risks —

High competitive landscape and on top of that unorganised market also poses a challenge

Maximum revenue coming from few client posing concentration risk

Any negative publicity in today digital marketing can have significant impact on company revenues

Also READ : Fino Payment Bank IPO : SUBSCRIBE OR NOT

Strength

Association with National and international brands

Omnichannel presence

India’s leading beauty and personal-care companies in the organised space and enjoys strong brand awareness

Strong supply-chain capabilities with around 20 warehouses throughout the country

Stringly technological driven business

Future

The company has a relatively asset-light business. With significant spending on marketing to attract new consumers and subsidiaries to open new retail stores, it will be able to scale up its business.

Valuations

Valuations are really astronomical and looks like promoters encashing the bull market leaving little on table

Should we apply?

One can avoid and wait for significant dip to enter. Long term story remains intact

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Fino Payments Bank IPO : Subscribe or NOT?

The data has been compiled from various sources and might have small difference but overall theme is to subscribe or not — we will focus on that

Fino Payments Bank IPO– incorporated in 2007 and it offers a diverse range of financial products and services that are primarily digital and have a payments focus. The company is a fully-owned subsidiary of Fino Paytech. It is backed by investors like Blackstone, ICICI Group, Bharat Petroleum and International Finance Corporation (IFC).

Business — The company has a pan-India distribution network and its’ major products and services includes:

• Current accounts and Savings accounts (CASA),

• Issuance of debit card and related transactions,

• Facilitating domestic remittances,

• Open banking functionality (through their Application Programming Interface),

• Withdrawing and depositing cash (via micro-ATM or Aadhaar Enabled Payment System (AePS) and

• Cash Management Services (CMS).

The company’s merchants facilitate them in cross-selling their other financial products and services such as third-party gold loans, insurance, bill payments and recharges. Fino Payments also manages a large BC (Business Correspondents) network on behalf of other banks.

Also READ : NYKAA IPO : SUBSCRIBE OR NOT

Offer purpose —

300 cr of fresh equity and 900 cr of offer for sale of existing shares. Augmenting Bank’s Tier – 1 capital base to meet its future capital requirements.

Risks —

High competitive landscape

Payments banks cannot undertake lending activities restricting their growth, They can accept only savings and current deposits. The aggregate limit per customer is Rs 2,00,000. They are required to have a minimum of 25 per cent of their physical access points in rural areas.

Geographical concentration also poses a risk

Strength

Unique DTP (Distribution, Technology, Partnership) network helps in better customer servicing

Focus on technology development and in-house technological expertise

Customer centric and innovative business model

Highly experienced management team

Vision of socially inclusiveness and empowerment

High market share in the Micro-ATM segment

Future

The bank’s unique DTP (distribution, technology and partnership) framework, technological expertise and merchant-led distribution model enable it to reach a vast number of customers in under-penetrated markets while keeping its costs low.

Valuations

Valuations are really high and looking at growth prospects , it will take time for valuations to become reasonable

Should we apply?

One can avoid and wait for significant dip to enter. Also keep in mind better choices available in market for investment

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Protected: Session9

Biggest Marketing Bargain : Customer Service

Online needs offline to scale up!!

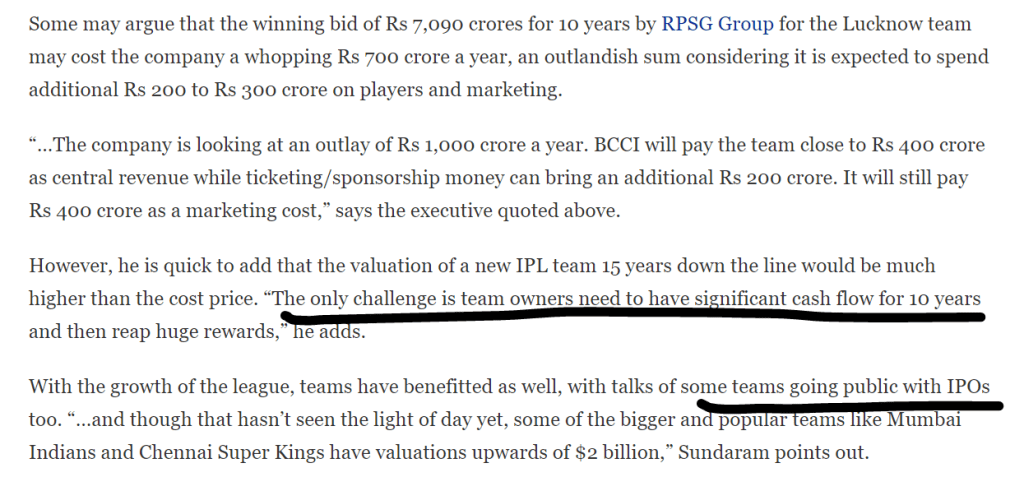

IPL and CASH FLOWS

E 3W HiLoad -Lightening charge : Playground is Changing

BOLT @ 1