Energy costs in European Union

BE FINANCIALLY INDEPENDENT

Its a DREAM come true

pwd – platform

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Dreamfolks in India’s Largest Airport Service Aggregator Platform. Company provides clients the option of providing their end consumers different mechanisms to access certain airport-related services like lounges and all the other services

DreamFolks platform is proprietary and has been developed in-house. The platform and the technology is cloud-based and it allows lounges and other operators to check the benefits of the consumers based on the cards, memberships, or vouchers, and also allows access to the different facilities based on the benefits or integration as per our clients, such as banks or networks, processes, and their systems

Company’s platform actually comprises of quite a few components. There is benefit configuration, there is benefit calculation, there’s an entire management engine, there are data exchange, APIs with different banks and networks, and integration options to embed into different mechanisms, including with company partners. Platform also facilitates the use of hybrid access modes depending on the client’s preference, so they can use whichever mechanism that is most beneficial for them. It also facilitates lounge access processes so that consumers benefit such things in real time across various access modes. And that drives accurate accounting and is designed to prevent abuse and denial of services to consumers

Major expenses are linked to employee compensation and in-house R&D expenses. And being an extremely asset-light company with a very lean organizational structure and size, Company don’t have any major capex needs or other outlays and Company seems confident of financing any future scale-up or expansion through internal accruals

Current mix of the lounge versus other services 95% versus 5%, Similar margins

40% to 45% in the first half and rest in the second half of the year, due to the simple reason that the festivals and the holiday season kicks in only starting from August, September.

100% coverage across all 60 Airport lounges operational in India

Market share of ~95% of all India issued card based access to domestic lounges in India (FY22)

68% share of the overall lounge access volume in India (FY22)*

Present currently in 10 railway lounges across the country and witnessed a steep growth rate with our modernization of railway stations happening at great next speed

Golf Games, Lessons and Railway lounges are new categories

This association will give customer access to golf games and lessons at 40+ golf clubs throughout India and 250+ golf clubs and resorts in the Asia Pacific region.

Price Realization on the blended basis is INR 940 approximately. Domestic is close to INR 840-INR 845. And internationally, that would be between INR 1,200 to 1,400.

Client 52 —Employees 60 –Nov 22 update, 64 employees Feb23

Touchpoints 1450 in Nov 22, 1486 in Feb23, might cross 1500 by Apr23

Touchpoints refer to a service fulfilment point at Airports across India and overseas owned by service providers with whom Dreamfolks has a contractual arrangement

Next phase of growth is centered upon three levers;

Cross-selling and up-selling to existing clients,

Acquiring new clients in existing and new sectors and

Via geographic expansion from a purely domestic focus currently to an international focus in pre-determined geographies.

With the existing clients, we aim to increase wallet share and expand our association beyond airport lounge services to include F&B, spa, meet and assist.

As regards new clients, we aim to expand into new sectors to create customer engagement and provide loyalty management solutions. Another focus area is to focus on customer engagement and loyalty solutions for corporate clients and build specific solutions for loyalty companies, ecommerce companies, new age digital companies, hospitality sector companies, and neo banks amongst others

Replication of similar successful operating model by leveraging deep knowledge of industry, technology innovation, process expertise and business model across new high growth markets which include Central and Eastern Europe, Middle East, Africa and Southeast Asia.

Recent developments

ASPIRE Lounges Australia – Delighted to tie up with ASPIRE Lounges Australia. With this partnership, air travelers can now experience exclusive luxury lounge access in Sydney, Melbourne, Perth and Brisbane as part of 66 Aspire Branded Lounges globally.

Dhanlaxmi Bank – Tie-up for access to Indian Lounges for their customers

FCM Travel – Corporate tie-up to provide their customers with domestic lounge access, Meet & assist and Airport Transfer Services

Onboarded 5 New Clients Including Akasa Air, one of the newest LCCs in India

Lounge area and capacity expansion at T3 Indira Gandhi International Airport, Delhi from 2,500 sq ft to 10,000 sq ft.

Added Lounge at Bengaluru’s KempeGowda International Airport, T2

Strategic tie-up with the leading Golf Service provider for access to golf games and lessons at 40+ golf clubs throughout India and 250+ golf clubs & resorts in the Asia Pacific region.

Company is is getting into exclusive contracts with the lounges.

In terms of the technology company is deeply integrating with banking partners. So that is one of the strong points because the step of integrating with these clients itself is a very long process, And there are a lot of compliance as well.

Value added services:- airport meet, assist in transfer, golf, railway lounges not easy to start and pickup by competition

Amazing aspect is almost Nil CAC

RBI may reduce the MDR rates on credit card companies so going forward, what credit card companies also have indicated that if this were to happen, and they will reduce rewards and services they offer to protect their margins – that will negatively impact company business in short term

International lounge vs domestic lounge traffic can change margin profile on either side

Any situation like Covid can again lead to bad times for company

UPI payments can pose a small risk

Competition like Priority Pass etc –this risk is somewhat mitigated as competition have been in this market and they

have been the global player across for more than 30 years now. So, in their presence, Company have actually taken away the India share from them

IMAGES FROM INDIAN AIRPORTS over last 10 months showing lounges are high in demand, runway are back to back lined up with airplanes signifying air travel increasing and travellers interest in lounges also increasing–so Increase in travelers and increase in interest of traveler for lounges can be huge tailwind in coming decade 2023-2033

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Charts are shared for educational/Study purposes

Do your own due diligence before buying selling

Sample is shown below

Those who want to get associated for short term or long term for such QUALITY TECHNICAL SETUPS can drop me a message on alphaaffairsf2f@gmail.com

or followme on Twitter @alphaaffairsf2f

Approximate commitment of 20 high quality bullish setups every month (approx 4-5 every week)

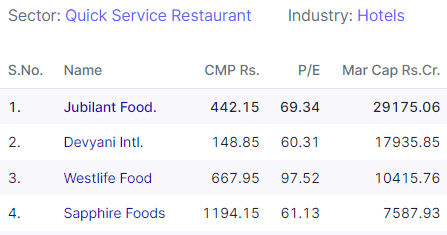

Looks better to stay away from QSR companies like Sapphire, Devyani, Zomato, Jubilant food

Dated 25-feb-23

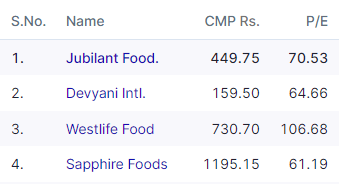

Dated 25Apr-23 –Decision paid off well –even in the recent rally , these stocks did not run

Time is coming to accumulate slowly after one correction

Biofuel, Decarbonization, Aviation, Import saving, greenhouse gases, SAF

So simple yet so deep message!!

Deals, Mergers, acquisitions look lucrative but actuality comes when its done. Similarly as an investor you learn more about a company after buying a good quantity of shares. You have skin in the game once you do that.

I believe in this concept from Day1 , only advantage we have is we can divorce a stock

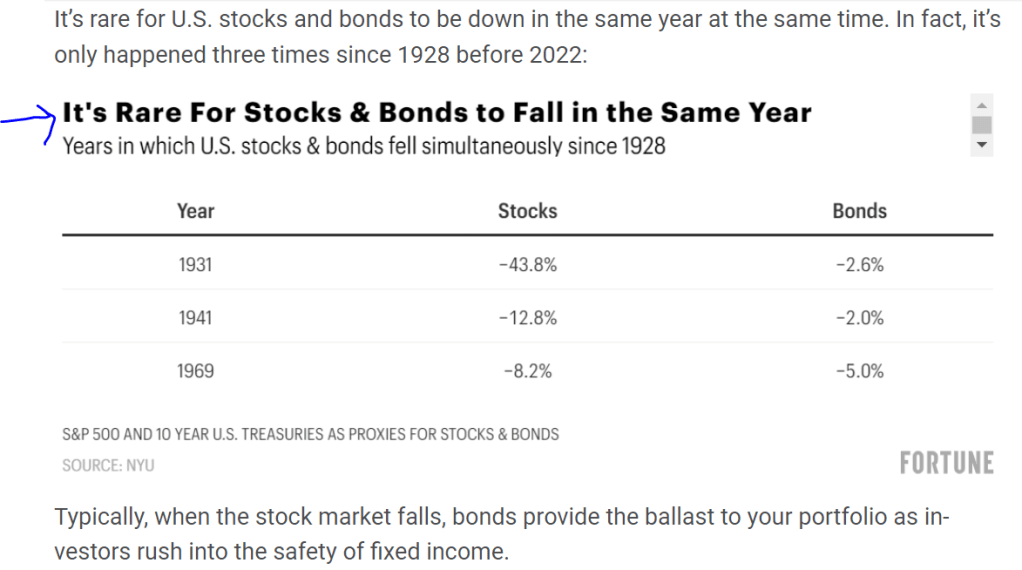

With inflation still high and central bank rates set to rise further, demand is expected to remain weak for the rest of the year.

Shipping group Maersk predicts that demand for containers — a proxy for trade — will fall by 2.5 per cent this year.

The S&P monthly survey of purchasing managers indicated that new export orders contracted across the world throughout the second half of last year and in January. Last month, the IMF forecast that global trade growth would decline to 2.4 per cent this year, from 5.4 per cent in 2022.

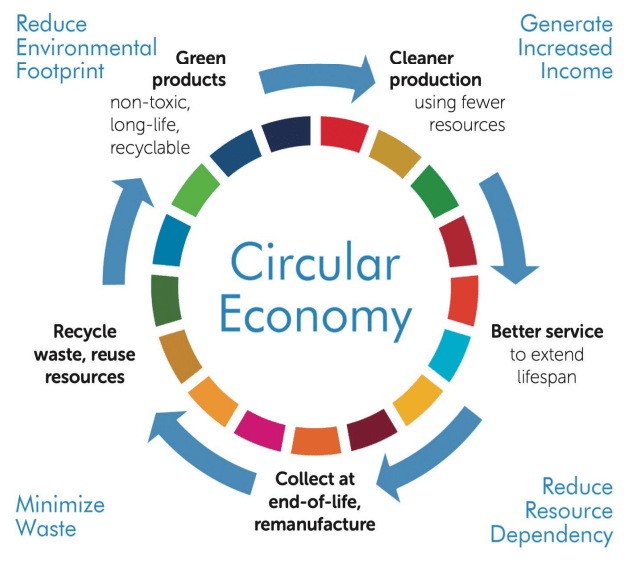

Recycle, Reduce, reuse, green products, carbon footprint

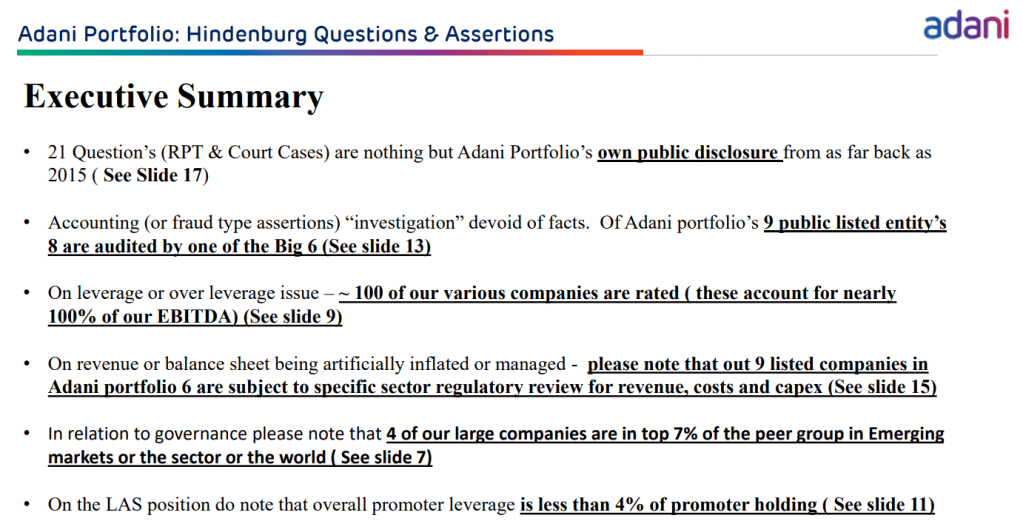

413 page response by Adani

Hindenburg response to Adani group here

To understand better on the stock, follow below links

The Pomodoro Technique is very popular. The steps are easy:

https://hindenburgresearch.com/adani/ –full report here

Answers by Adani to report here

Snippets of report –focus is questions

Given Gautam Adani’s claims to welcome criticism and embrace transparency, we hope the Adani Group will be pleased to answer the following 88 questions:

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Story – When the going gets tough, the tough get going, wrote American football coach John Thomas in 1953. This axiom today applies to the Hyderabad-based MTAR Technologies too, in more than one way. Old-timers at MTAR recall India’s former President and ‘Missile Man’ Abdul Kalam telling his team during his DRDO days: “If nothing is getting done, go to that Reddy company at Hyderabad.”

In fact, the Reddy duo – Ravindra and Satyanarayana – set up MTAR, to meet a challenge thrown at them by the government, way back in 1970, to make a critical cooling channel for a nuclear reactor.

As global suppliers began tightening their screws on India’s nuclear power ambitions, the government asked HMT to work on the cooling channel. The late Ravindra’s son P. Srinivas Reddy, MD, MTAR, recalls that HMT expressed its inability to do this and the Reddy duo, who were working there, quit and told DAE they would take up the channel challenge.

There are many Proud moments on its journey including

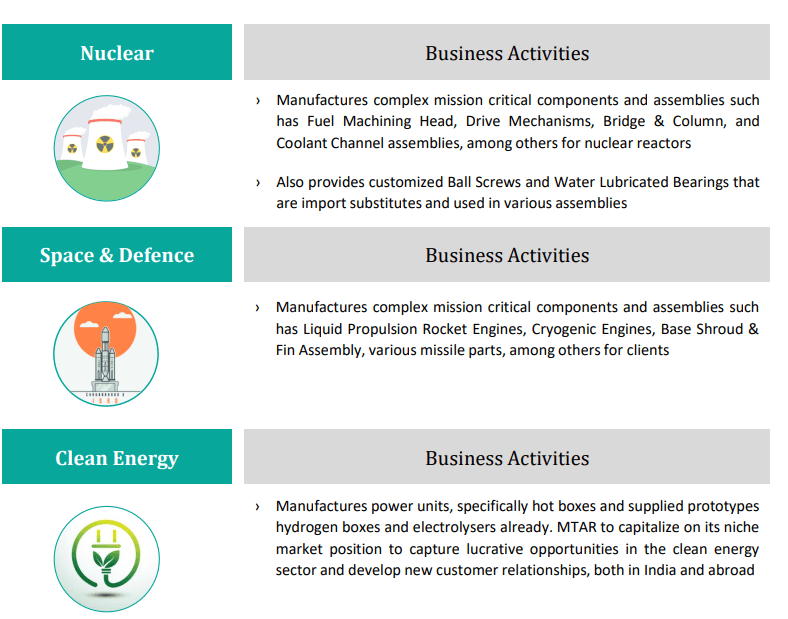

Mangalyan PSLV engine supplied by MTAR to ISRO

GSLV Mark III engine for the Chandrayaan II mission

Base shroud assembly for Agni missiles

Source —BusinessIndia

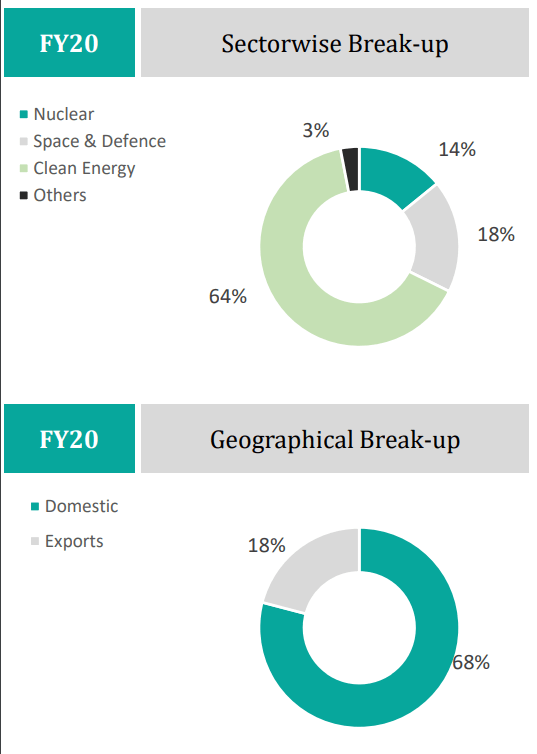

Order Book moving to Clean energy over last 2years. Order book at Sep 2022 closure is 1288 cr while Current TTM sales is ~394 cr (till Sep22)

Company is export oriented–trend is almost same in last 3 years

Clean energy orders constitutes almost more than 50% order book every year

Space and Defense Constitutes between 18-26%

Nuclear constitutes 14-22% order book

Other segments growing fast and now at 5.7%

High Entry Barriers and Increased customer dependency on Mtar

Strong Order Book Position and Strong repeat business due to MTAR’s engineering capability

Advanced and End to End Manufacturing Capabilities

Strong Diversified portfolio of critical and differentiated engineered products in emerging domains of Nuclear, Space,Defense, Clean energy , fuel cell etc

Manufactures import substitute products like Roller screws, ball screws. MTAR will be the first manufacturer of roller screws in India and the product will be used for a wide variety of applications in the nuclear, space and defence sectors

Manufactures precision machined components

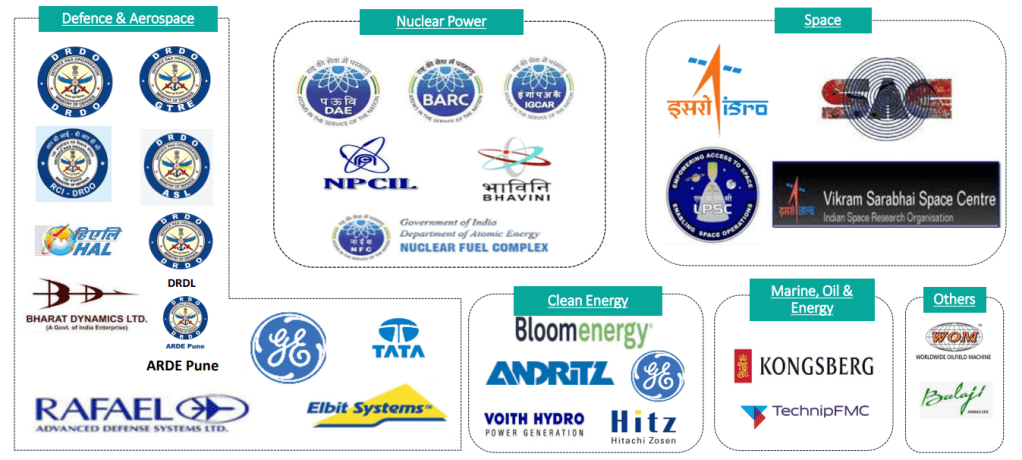

Strong association with Exiting Customers & new Customers in Pipeline

Stringent Quality checks –Company uses high precision quality inspection equipment such as 3D co-ordinate measuring machines (CMM), laser measuring, optical alignment instruments, non-contact measuring and other such non-destructive testing equipment, to ensure ideal quality. “MTAR enjoys an unblemished record of quality for its product range”

Capability of making —

Experienced Board of Directors & Well Qualified Management Team

Certifications and Awards

Developed global supplier base over the years &procures materials from US, Brazil, among others, Low supplier dependency which also enables negotiation of favorable terms. Global network provides the option to take advantage of better pricing as available in a particular market

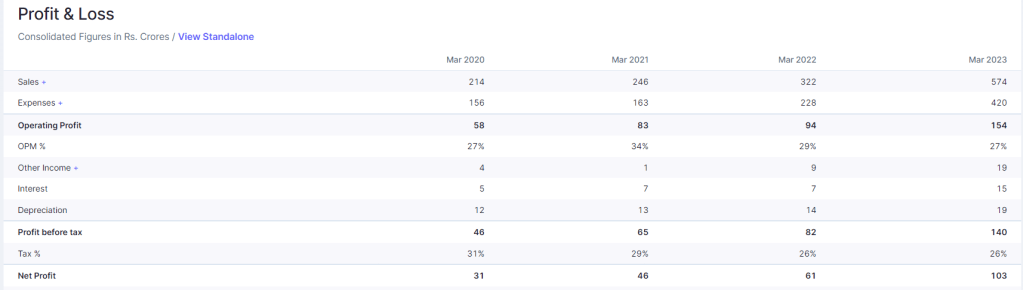

Strong growing order book –Currently ~1300cr order book giving revenue visibility of 2+ years

Strong Net profit margins with company growing at 30% CAGR. FY23 and FY24 expected to grow similarly or better

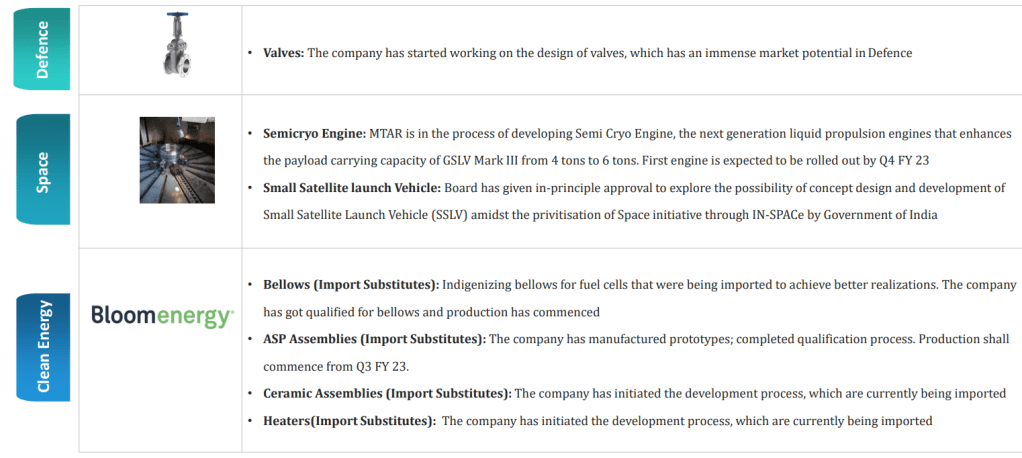

The company has got the in principle approval from the board to establish electronics manufacturing in-house and started working on it

Indigenization of Roller Screws done, Executed the FAI orders

The company has also initiated the development of Electromechanical actuators, which find application in Space and Defense sectors

Specialized fabrication facility to be functional soon, The new capabilities are expected to bring in lot more customers. Sheet metal manufacturing facility at Adibatla, Hyderabad has become operational in Fiscal 2023 to undertake sheet metal jobs for ISRO, Bloom Energy and certain other customers. This business expected to generate 100 cr revenue in FY24. Commenced shipments to South Korea and USA; supplied Rs. 11.8 Crs worth of sheet metal orders for Clean Energy sector in Q2 FY 23

Upgrade existing facilities by implementing new technology and releasing release bottlenecks in production capacity

Expanding Product Portfolio and CAPEX ongoing along with IMPORT SUBSTITUITION

Increasing employee strength in last two years as order book increasing continuously

In discussion with below customers to reduce dependency on existing clients

MTAR is developing the following products in collaboration with Bloom to expand its product portfolio in clean energy sector:

Hydrogen boxes- Use Hydrogen to generate power

Electrolyzers – generate green hydrogen from water that shall be used in power units to generate power with zero carbon emissions

(Bloom is one of the largest and the fastest growing player globally in the stationary hydrogen fuel cell segment and has 70% of its revenues

coming from products segment and balance from services)

Opportunities in each business domain due to Indigenization policies in defense, Aatmnirbhar Bharat policies in different sectors, demand of fuel cells and growing maintenance market

Exponential growth expected for Indian players in Space sector given ISRO’s plan to commercialise the Indian space sector

and offer its products and services to other countries

Opportunities in defence offset partnership with certain global OEMs

14 New reactors planned and tenders to be released, one recator have equipments worth ~2200 cr Rs where MTAR is focussing on. Long term relationship with NPCIL can help MTAR to grab that opportunity

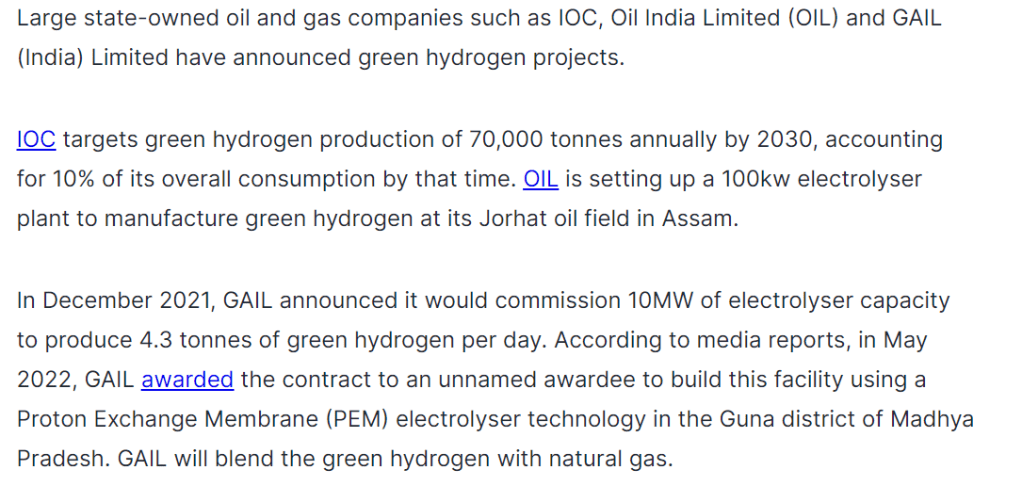

Green Hydrogen push by Government brightens prospects further. A capital outlay of Rs75,000 crore (US$9.4 billion) over the next three years to develop manufacturing capacities for clean energy technologies, which include electrolysers to produce green hydrogen. NTPC is already walking the talk on green hydrogen. The company is developing India’s first hydrogen-to-electricity project using US-headquartered Bloom Energy’s solid-oxide electrolysers and fuel cell technology. NTPC’s floating solar plant will power the electrolysers to produce green hydrogen. Bloom Energy’s hydrogen fuel cell technology will convert the hydrogen into carbon-neutral electricity without combustion to power NTPC’s Guest House in Simhadri, Visakhapatnam.

No long term contracts with suppliers, though risk is mitigated with enough suppliers on board

Client concentration risk –Bloom energy almost constitutes 50% of orders–Company is trying to get more clients onboard to mitigate this risk

Valuations seems a bigger risk than above mentioned ones. If orders/Profit don’t materialize on expected lines, stock can easily correct to 900-1200 zone or It can happen that stock may not fall much , but may remain stagnant between 1200-2000 range for long leading to opportunity loss

Any policy changes can delay the expected outcome

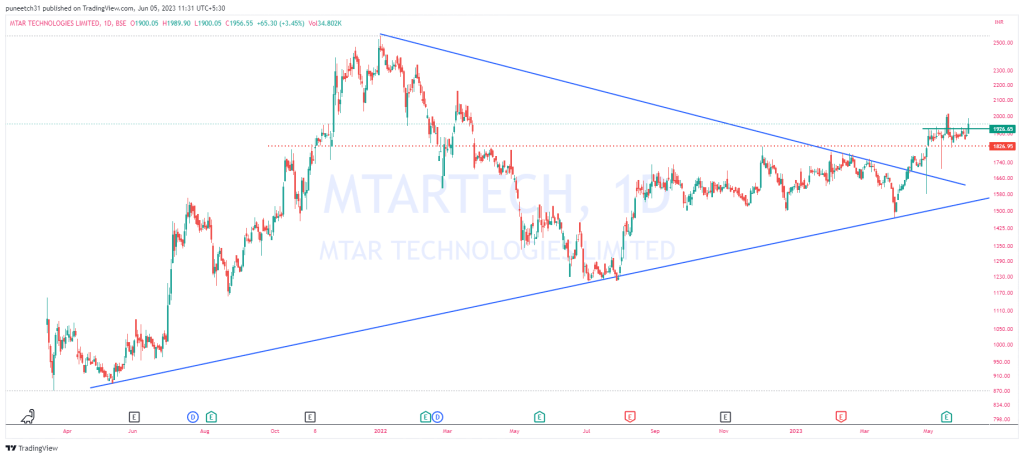

Technicals

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Key takeaways from Q3FY23 IT services

1. Demand remains strong for cloud and automation

2. Indian IT companies are benefiting from clients looking to consolidate their vendors

3. Attrition is stabilising

4. Employee addition slowed significantly in Q3

5. A slowdown is imminent, and some tech spending will be delayed

Sources : Forbes

Will keep updating this Hashtag, follow closely to cancel out noise and focus long

Most clicks on alpha-affairs.com in 2022

And

Book Summary : The Little Book That Builds Wealth by PAT DORSEY