Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

MTAR Technologies – Emerging Midcap

Story – When the going gets tough, the tough get going, wrote American football coach John Thomas in 1953. This axiom today applies to the Hyderabad-based MTAR Technologies too, in more than one way. Old-timers at MTAR recall India’s former President and ‘Missile Man’ Abdul Kalam telling his team during his DRDO days: “If nothing is getting done, go to that Reddy company at Hyderabad.”

In fact, the Reddy duo – Ravindra and Satyanarayana – set up MTAR, to meet a challenge thrown at them by the government, way back in 1970, to make a critical cooling channel for a nuclear reactor.

As global suppliers began tightening their screws on India’s nuclear power ambitions, the government asked HMT to work on the cooling channel. The late Ravindra’s son P. Srinivas Reddy, MD, MTAR, recalls that HMT expressed its inability to do this and the Reddy duo, who were working there, quit and told DAE they would take up the channel challenge.

There are many Proud moments on its journey including

Mangalyan PSLV engine supplied by MTAR to ISRO

GSLV Mark III engine for the Chandrayaan II mission

Base shroud assembly for Agni missiles

Source —BusinessIndia

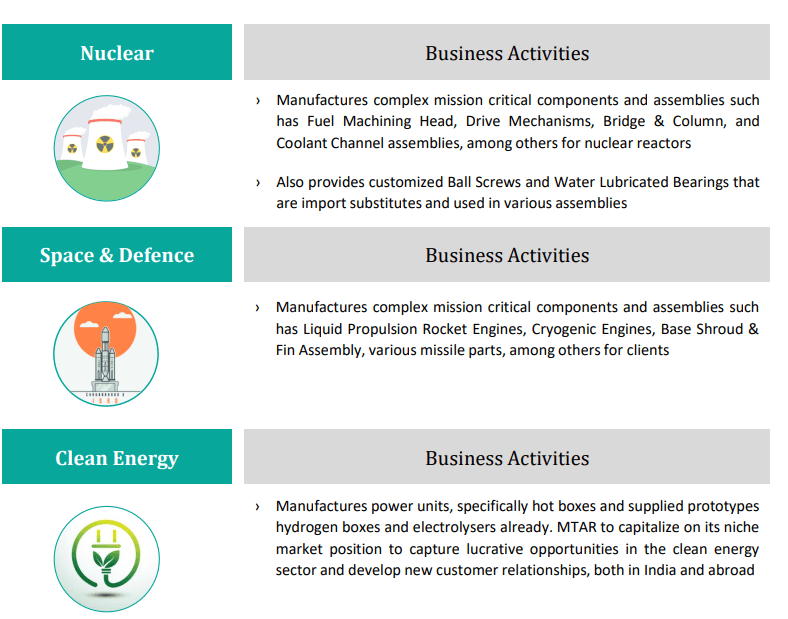

Business Domains

Order Book

Order Book moving to Clean energy over last 2years. Order book at Sep 2022 closure is 1288 cr while Current TTM sales is ~394 cr (till Sep22)

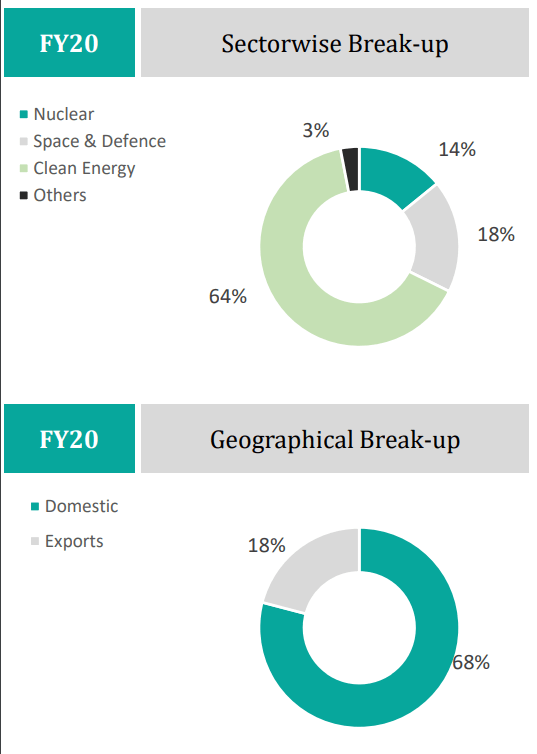

Sector wise and Geographical Break up of Orders

Company is export oriented–trend is almost same in last 3 years

Clean energy orders constitutes almost more than 50% order book every year

Space and Defense Constitutes between 18-26%

Nuclear constitutes 14-22% order book

Other segments growing fast and now at 5.7%

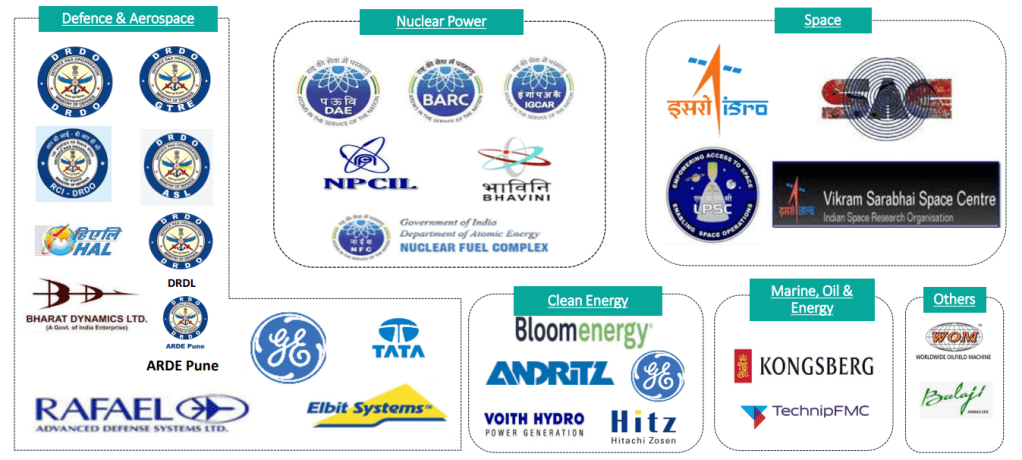

Customers

Strengths

High Entry Barriers and Increased customer dependency on Mtar

Strong Order Book Position and Strong repeat business due to MTAR’s engineering capability

Advanced and End to End Manufacturing Capabilities

Strong Diversified portfolio of critical and differentiated engineered products in emerging domains of Nuclear, Space,Defense, Clean energy , fuel cell etc

Manufactures import substitute products like Roller screws, ball screws. MTAR will be the first manufacturer of roller screws in India and the product will be used for a wide variety of applications in the nuclear, space and defence sectors

Manufactures precision machined components

Strong association with Exiting Customers & new Customers in Pipeline

Stringent Quality checks –Company uses high precision quality inspection equipment such as 3D co-ordinate measuring machines (CMM), laser measuring, optical alignment instruments, non-contact measuring and other such non-destructive testing equipment, to ensure ideal quality. “MTAR enjoys an unblemished record of quality for its product range”

Capability of making —

- Low volume R&D to high volume production products

- Regular to complex products

- Low weight to high weight products

- Export oriented to import substituition products

Experienced Board of Directors & Well Qualified Management Team

Certifications and Awards

Developed global supplier base over the years &procures materials from US, Brazil, among others, Low supplier dependency which also enables negotiation of favorable terms. Global network provides the option to take advantage of better pricing as available in a particular market

Triggers

Strong growing order book –Currently ~1300cr order book giving revenue visibility of 2+ years

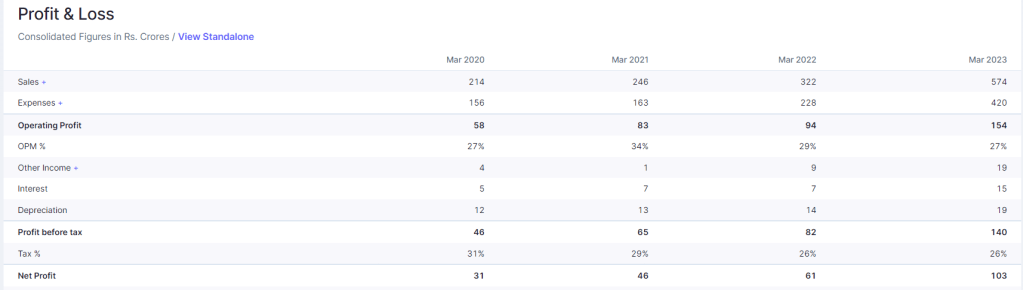

Strong Net profit margins with company growing at 30% CAGR. FY23 and FY24 expected to grow similarly or better

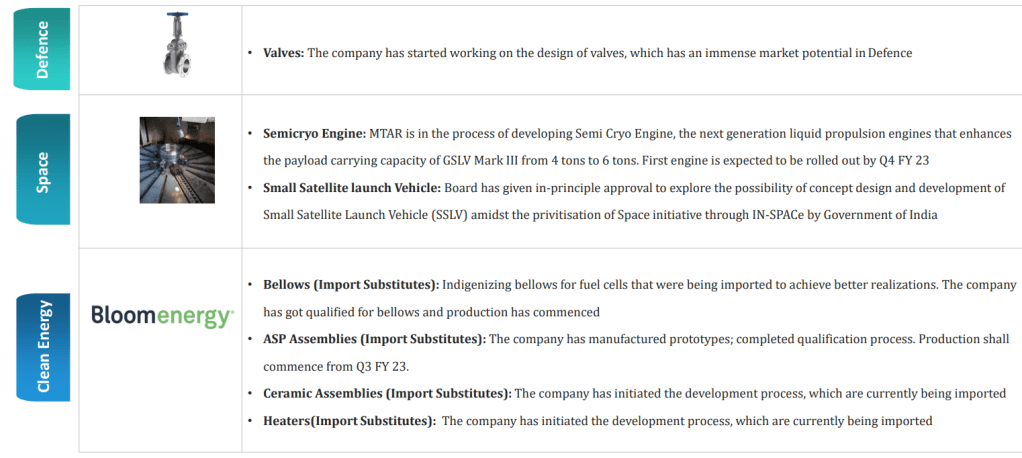

The company has got the in principle approval from the board to establish electronics manufacturing in-house and started working on it

Indigenization of Roller Screws done, Executed the FAI orders

The company has also initiated the development of Electromechanical actuators, which find application in Space and Defense sectors

Specialized fabrication facility to be functional soon, The new capabilities are expected to bring in lot more customers. Sheet metal manufacturing facility at Adibatla, Hyderabad has become operational in Fiscal 2023 to undertake sheet metal jobs for ISRO, Bloom Energy and certain other customers. This business expected to generate 100 cr revenue in FY24. Commenced shipments to South Korea and USA; supplied Rs. 11.8 Crs worth of sheet metal orders for Clean Energy sector in Q2 FY 23

Upgrade existing facilities by implementing new technology and releasing release bottlenecks in production capacity

Expanding Product Portfolio and CAPEX ongoing along with IMPORT SUBSTITUITION

Increasing employee strength in last two years as order book increasing continuously

In discussion with below customers to reduce dependency on existing clients

MTAR is developing the following products in collaboration with Bloom to expand its product portfolio in clean energy sector:

Hydrogen boxes- Use Hydrogen to generate power

Electrolyzers – generate green hydrogen from water that shall be used in power units to generate power with zero carbon emissions

(Bloom is one of the largest and the fastest growing player globally in the stationary hydrogen fuel cell segment and has 70% of its revenues

coming from products segment and balance from services)

Opportunities in each business domain due to Indigenization policies in defense, Aatmnirbhar Bharat policies in different sectors, demand of fuel cells and growing maintenance market

Exponential growth expected for Indian players in Space sector given ISRO’s plan to commercialise the Indian space sector

and offer its products and services to other countries

Opportunities in defence offset partnership with certain global OEMs

14 New reactors planned and tenders to be released, one recator have equipments worth ~2200 cr Rs where MTAR is focussing on. Long term relationship with NPCIL can help MTAR to grab that opportunity

Green Hydrogen push by Government brightens prospects further. A capital outlay of Rs75,000 crore (US$9.4 billion) over the next three years to develop manufacturing capacities for clean energy technologies, which include electrolysers to produce green hydrogen. NTPC is already walking the talk on green hydrogen. The company is developing India’s first hydrogen-to-electricity project using US-headquartered Bloom Energy’s solid-oxide electrolysers and fuel cell technology. NTPC’s floating solar plant will power the electrolysers to produce green hydrogen. Bloom Energy’s hydrogen fuel cell technology will convert the hydrogen into carbon-neutral electricity without combustion to power NTPC’s Guest House in Simhadri, Visakhapatnam.

Risks

No long term contracts with suppliers, though risk is mitigated with enough suppliers on board

Client concentration risk –Bloom energy almost constitutes 50% of orders–Company is trying to get more clients onboard to mitigate this risk

Valuations seems a bigger risk than above mentioned ones. If orders/Profit don’t materialize on expected lines, stock can easily correct to 900-1200 zone or It can happen that stock may not fall much , but may remain stagnant between 1200-2000 range for long leading to opportunity loss

Any policy changes can delay the expected outcome

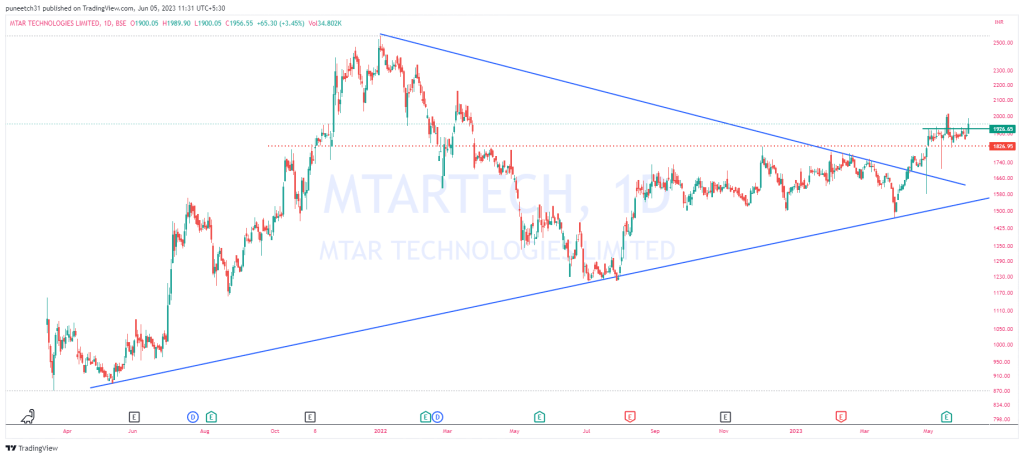

Technicals

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Discover more from ALPHA AFFAIRS

Subscribe to get the latest posts sent to your email.

it is very informative .. It builds more confidence to invest for long run.. Thanks for sharing

LikeLike