The report highlights the market size, revealing that the online video sector generated an estimated $4.2 billion in 2024. Of this revenue, 75 percent came from advertising, while 25 percent was derived from subscriptions.

According to the report, piracy could cost India’s digital video sector $2.4 billion and lead to a loss of 158 million users by 2029.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Axiscades Technologies Limited

Key Investment thesis –> Company focus on Aerospace, Defense, Semiconductor, Electronic system verticals and gearing up for FY26, FY27

Business

AXISCADES is a leading, end to end technology and engineering solutions provider aiding creation of innovative, sustainable and safer products worldwide. AXISCADES is headquartered in Bangalore with subsidiaries in USA, UK, Canada, Germany, India and China; and offices in Germany, France, Denmark, USA and Canada. AXISCADES has a diverse team of over 3,100 professionals working across 20 locations across North America, Europe, UK and Asia-Pacific, striving to reduce the program risk and time to market.

The company offers Product Engineering Solutions across Embedded Software and Hardware, Digitization and Automation, Mechanical Engineering, System Integration, Test Solutions, Manufacturing Engineering, Technical Publications, and Aftermarket Solutions. The solutions comprehensive portfolio covers the complete product development lifecycle from concept evaluation to manufacturing support and certification for Fortune 500 Companies in the Aerospace, Defense, Heavy Engineering, Automotive, Energy and Semiconductor industries.

Company Portfolio

Current serving Major Industries

Aerospace

Heavy Engineering

Products engineering

Products and Solutions for Defense

AIP and Energy

Semiconductors

Awards

Received 3rd consecutive Diamond supplier award from Bombardier for 2022. This recognition is a testament to our unwavering commitment to excellence, innovation, and delivering with the highest standards of quality.

Opportunities :

Unique positioning with deep domain capabilities ranging across competencies, with respect to – Electronics Products, Engineering Services and Defence

Growth driven by leveraging Digital ER&D and Defence

ER&D Services – A large and underpenetrated market with a Global TAM of ~$1 Tn

Strong Defence-Tech Play with leadership in Radar, Sonar and Electronic Warfare systems

Revenue Breakup

FY24 revenue breakup

Q1Fy25 revenues breakup

Q2Fy25 revenues breakup

Fundamental Ratios, Cash, EBITDA, PAT, SHP

Stable OPM, Stable tax, Quarterly YOY growth in sales and PAT, Borrowing reducing

DE ~0.4 , Free cash flow is good , Pledge is Nil, ROCE < 15 and ROE<10%

Promoter has sufficient skin in game, Cash flows are good, Cash conversion cycle is elongated

Triggers

Macro Trends :

Recent Triggers in last 1 year or so

Appointment of Chairman Mr. Abidali

Appointed Mr. Abidali Neemuchwala as Chairman of the Board and Non-Executive Director at AXISCADES. With a distinguished career spanning over three decades in the technology industry, he has earned enviable reputation for his expertise in aligning organizations, driving business results, and consistently leading transformational initiatives.

Strategic partnerships and Opening Engineering design center

Signed a strategic partnership with with Cantier, a Singapore-based powerhouse in Manufacturing Execution Systems (MES), with a specialization in Industry 4.0 integration to create a synergy that promises to elevate precision, efficiency, and innovation in the manufacturing sector.

Inaugurated Engineering Design Centre in Saltney, UK to serve the long-term requirements of the Aerospace Industry and various promising opportunities in the region.

Signed a strategic partnership with KANZEN Institute Asia-Pacific Pvt Ltd (KIAP), for new age Industry IIoT, Digital Automation and MES 4.0 implementation for delivering enhanced value to our Global customers.

Mergers and Acquisitionsand QIP

Completed the acquisition of add solution GmbH which will strengthen our service offerings and bring opportunities to deliver enhanced value to our combined global client base. . This will provide us with a strategic foothold in the automotive space, with significant offshoring opportunities and access to marquee global automotive OEMs.

The board has also approved the acquisition of EPCOGEN., a niche service provider in Energy space, specializing in engineering design and solutions. This proposed acquisition will strengthen our presence in energy vertical, provide access to Middle East and North American Energy markets

QIP in Jan2024 at 657Rs/share — The Company successfully concluded the Equity Raise of INR 220 Crores in January 2024, with marquee Institutional Investors subscribing to the issue. This will strengthen the balance sheet and improve profitability, Reduction in Net Borrowings by 60% from INR 214 crores to INR 85 crores, which will significantly reduce Finance Cost

Deal Wins

Deal win with Aerospace OEM with TCV of $ 18 Mn in the areas of in-service repair and manufacturing support

Design and prototype wins in several defense programs, such as HISAR, next generation ERP for combat aircrafts, Intel based SBC, DEAL satellite terminal design, DF for Naval program, adding to the production order pipeline

Digital Team ramped to 75+ FTEs with deep competencies in automation, AI/ML and robotics, with complete digital project execution capabilities

Acquisition of add-solutions GmbH and EPCOGEN, opens new vistas in Automotive and Energy Space, adding strategic logos and competencies

Q4FY24 updates

Revenue from new customer logos grows to Rs.69 crores, a growth of 5 Times over the previous year

Deal win with Aerospace OEM with TCV of $ 18 Mn in the areas of in-service repair and manufacturing support

Defense Production Revenues in Mistral triples from Rs.39 crores to Rs.112 crores, with Rs.272 crores in executable production orders

Commencement of delayed delivery of Man Portable Counter Drone System (MPCDS) to the Indian Army, with significant addressable

market in Indian Defense and Global Markets

Design and prototype wins in several defense programs, such as HISAR, next generation ERP for combat aircrafts, Intel based SBC, DEAL satellite terminal design, DF for Naval program, adding to the production order pipeline

Digital Team ramped to 75+ FTEs with deep competencies in automation, AI/ML and robotics, with complete digital project execution capabilities

Advanced level discussions with leading helicopter manufacturer for engineering and design support

New opportunities in counter drone system over next 5 years are highly promising with addressable market more than INR 3,000 Cr. 40 Nos of one of a kind Man Portable Counter Drone System (MPCDS) cleared for dispatch to the Indian Army. Balance 60 Nos under production.

Onboarded world’s largest phone and consumer electronic manufacturer as a customer with clear glide path on engagements into FY25

Order book at 30th Ap24 — 749Cr

Q1FY25 updates

Mistral Solutions received order of ₹90 crores from BEL for supplying Radar Processing Systems

Ramp up in aerospace with European OEM focused on production and plant migration efforts

Ramp up in high end cybersecurity solutioning with UK automotive manufacturer.

Onboarded an EPC major from Middle East as our customer with long term contract

Completed second tranche of delivery of Man Portable Counter Drone System (MPCDS) to the Indian Army

Expenses hit in past Q3/Q4 Fy24

Increase in finance cost due to debt funding for Mistral acquisition . In Q2 FY24, the material cost has increased due to increase in production orders in Mistral and increase in employee expenses on account of annual increments and investments in building competencies in Embedded and Digital for future growth

Q2FY25 Update

Defence revenues grew by a healthy 73% QoQ, with Defence production revenues surging by 84% QoQ, bolstered by a significant order backlog set for execution in fiscal years 2025 & 2026. With a healthy pipeline and focused approach, over the next 12-18 months, we aim the defence revenue to reach around 60% of the overall company’s revenue

Management commentary With latest focus areas

Unmanned combat, we are having anti-drone, drones, and drone controllers

Foreign OEMs, we have a three-pronged, that is, weapon package, submarine, and avionics. preferred offset partner for the weapon system, weapon package

new programs, all our missile programs, one is the largest missile program in India, another is an upgrade of the existing missile program, another is ground system for key programs

Product focus : particular product direct RF. Then there is, of course, our product X-band radar, which is primarily used in the submarine and marine systems.

Airbus, we have major programs running in India. C295, MRTT, Multi Role Transportation Tanker, which is going to be 330 based, And AVEX, of course, 319 based.

Tying with AgniKul, having an MOU with them, and approaching the ISRO, ISRO and other space agencies for two major things, NGLV, New Generation Launch Vehicle, and Bharatiya Space Station. So we want to add value to them significantly, and there could be opportunities in 3D additive manufacturing, and designing of certain subsystem blocks, etcetera. Then there is also chances for electronics-based algorithms and advanced systems, and for the guidance and navigation, that product we’ll be able to make. The third one is AI-based anomaly detection in the launching

Capturing some discussions from Dec24 confcall

C2P strategy, that is, chip to product. That is Mistral’s non-defense activity, or our group’s non-defense activity., we are shifting the center of gravity of C2P to US. Basically it will be driven out of US. We’ll have a small team there and driving the offshore team here. That’s the strategy

We are a very, very good RF in RF. We consider we are among the best in India for RF. RF and RF activities. Second is probably we are one of the best in handling mixed signals. We can handle analog, digital, RF, everything together. That is one of our forte. Third is sensor fusion. We can handle multiple sensor. Sensor fusion comes very, very handy when you deal with multiple sensor in a new AI environment, in new robotics or auto-driven and those kinds of things. We are extremely good in both. Then we are very good in ruggedization. We are especially because we are very defense focused. We can ruggedize any product and do that. And finally that we are very good in the chip, chip level, post-silicon, whatever it is, validation, verification, and take the chip to the product and then product to the customers

Continuous Hiring of Talent

Orders winning, Expansion in Middle east and Outlook for different segments by Management

Added this latest development on 17Jun25

INDRA SIGNS AGREEMENT WITH AXISCADES TO BOOST PRODUCTION OF CUTTING-EDGE SYSTEMS IN INDIA

Indra, a European-based global leader in defense, aerospace, and strategic systems, and AXISCADES a prominent technology solutions provider in defense, aerospace and strategic electronics, are proud to announce a strategic alliance.

Indra is keen to acquire defense-related products and services from AXISCADES, which will be delivered through AXISCADES’ comprehensive design, development, production, and supply chain center.

Both companies are actively exploring joint product development for the Indian and global markets, potentially adapting existing Indra products or creating new ones specifically tailored to meet customer needs.

TechnicalChart

Technical chart on 15-dec24

Technical chart on 29-dec24

Risks

Highly competitive industry

Acquisitions dont play out as anticipated

Customer concentration risk – On a consolidated basis, ~26% of ACTL’s revenues in FY23 were from its top two clients (35% in FY22).

Slowdown in Europe impacting automotive revenues

Heavy Engineering vertical remains a drag for few more qtrs although optimization work going on

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

The post discusses PLI schemes in the Electronics System Design and Manufacturing (ESDM) sector, which are part of India’s initiative to boost domestic electronics manufacturing. The schemes aim to incentivize production and attract investments, aligning with the government’s goal to make India a global hub for electronics.

The PLI schemes mentioned are part of a broader strategy under the National Policy on Electronics 2019 to overcome domestic manufacturing disadvantages like inadequate infrastructure and high finance costs, aiming to position India competitively in the global electronics market.

The thread includes technical charts for various stocks related to the ESDM sector, which could be analyzed for investment opportunities, reflecting the sector’s growth potential and market interest due to these government incentives.

Impact Of Data Localisation Laws The Indian government’s push for data localisation, under policies like the Digital Personal Data Protection Act, has accelerated the establishment of data centres. Global players such as AWS, Microsoft, and Google are investing heavily to comply with these regulations, while Indian companies like Jio and Yotta Infrastructure are scaling up their capacities.

Green Data Centres On The Rise Sustainability is a key focus for Indian data centres in 2025. Operators are investing in renewable energy sources like solar and wind to power facilities, with states such as Rajasthan and Gujarat leading in renewable energy adoption. Innovative cooling technologies, including liquid cooling and the use of natural resources for temperature management, are becoming standard practices to enhance energy efficiency.

Edge Computing And Regional Growth India’s shift towards edge computing is transforming data centre architecture. With the rollout of 5G and the proliferation of IoT devices, smaller edge data centres are being established closer to users in Tier 2 and Tier 3 cities.

Expansion Of Colocation And Hyperscale Facilities By 2025, colocation and hyperscale data centres will dominate the Indian market. Colocation facilities, which allow multiple organizations to share infrastructure, are becoming the preferred choice for startups and small businesses due to cost efficiency. On the other hand, hyperscale data centres, built to support massive data volumes for global giants like Amazon and Google, are rapidly expanding to cater to India’s growing digital needs.

Advances In Security And Automation With increasing cyber threats, Indian data centres are integrating advanced security measures such as Zero Trust Architecture, AI-powered threat detection, and biometric access controls. Automation is playing a vital role in optimizing operations. AI systems are managing energy consumption, predicting maintenance needs, and ensuring seamless uptime, reducing operational costs while improving efficiency.

Government Support And Policy Initiatives The Indian government’s initiatives, such as the National Policy on Software Products and state-level incentives, are creating a favourable ecosystem for data centre growth. Many states are offering subsidies on land, power tariffs, and taxes to attract data centre investments.

Opportunities In Tier 2 And Tier 3 Cities As data consumption grows beyond urban centres, data centre operators are expanding into Tier 2 and Tier 3 cities. These locations offer lower operational costs, ample land availability, and growing demand for digital services, making them attractive for future investments.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Jash Engineering

Key Investment thesis –> Increasing Demand of Water Intake Systems, Water and Waste Water Pumping Stations and Treatment Plants, Storm Water Pumping Stations, Water Transmission Lines, Consistent Business and Order book

Jash engineering is dedicated to offering varied products for use in Water and Wastewater Pumping Stations and Treatment Plants, Storm Water Pumping Stations, Water Transmission Lines, Desalination, Power, Steel, Cement, Paper & Pulp, Petrochemicals, Chemicals, Fertilizers and other process plants. Headquartered in Indore – India, Jash has six well-integrated state-of-art manufacturing facilities, four in India and one each in the USA & UK. Global presence with bases in India / USA / Austria / Hong Kong / UK

Employees > 1075, Countries served 45+, Manufacturing units 6, Capacity utilization 70% approx

Company has many accolades, and technical collaborations

Joint Venture with Invent , Germany to manufacture their range of aeration and mixing equipment.

Technical & Financial collaboration with Schuette, Germany for Bulk solids valves

Technical Collaboration with Invent, Germany for Disc Filter

Technical collaboration with Rehart, Germany for Archimedes screw pumps & hydro power generation.

Technical collaboration with Weco Armaturen, Germany to offer its range of Valves in Asian market

Business Segments and Revenue Contribution and Products

Domestic 40%, Exports 60%

Water control gates –60% (FY24) 49%(Q1Fy25)

Valves -15% FY24, 13% Q1FY25

Screening equipment 15% FY24, 31% Q1FY25

Hydropower and pumping solutions 10% FY24, 7% Q1FY25

Clientele

Strengths :

Long standing relationships with domestic marquee customers.

Efficient business model

Strong project execution capabilities

Diversified geographical presence in India and world

Strong Technical Qualification to bid for new projects

Highly experienced Management Team

Fundamental Ratios, Cash, EBITDA, PAT

ROCE>25% and ROE> 22%, DE ~0.23 , Free cash flow is good , Pledge is Nil

Net Profit went 67X+ in 10 Years, Consistent Dividend Payout

Consistent Profit growth, sales growth, ROE over 3 years, 5 years, 10 Years

Triggers

Expanding presence and Acquisitions

Acquired Waterfront Fluid Controls Ltd, UK in 2023.

WATERFRONT UK PLANT & OFFICE INAUGURATION After successful acquisition of Waterfront Fluid Controls Ltd, UK, the company has taken manufacturing plant on lease which is adjoining shed to the present Waterfront’s shed. This plant was commissioned on 31st May 2024.

A new plant for manufacturing process equipment is under construction in Chennai. This plant will be commissioned in December 2024/Feb25. This facility is being built at an approximate cost of Rs. 20 crores and this will start contributing to improvement in revenue from April 2025 onwards. This facility at its peak production capacity will contribute up-to Rs. 100 Cr to company revenue.

A new land has been acquired for expansion of Unit 4 (Fabricated Products Plant), SEZ Unit. This new plant of ~ 55000 sq. ft. will be commissioned in FY 2025-26. Manufacture Stainless steel products for the growing export market. The construction of this plant will start in October 2024 and the plant will be commissioned by year end 2025. This plant will be constructed at a tentative cost of Rs 22-23 crores inclusive of land and at its peak production capacity will contribute up-to Rs. 100 Cr to company revenue.

Good execution and order book and Consistent new orders

946 cr order book on 1st sep24, 74cr orders in pipeline, negotiation

FY25 guidance ~675cr

New Product developments

First Vortex Grit Mechanism with Grit Classifier For 26 MLD STP Jhansi, UP Jal Nigam

Combined Screening & Grit Removal System-1MLD (PTU) for Enviro-Infra, Bareilly, UP

First set of Bladder Vessel 9 m3 x 3, 1 m3 x 3 supplied to Varanasi WSP Project

3 Wheel Sealed Version Disc Filter for 6 MLD capacity for Delhi Jal Board

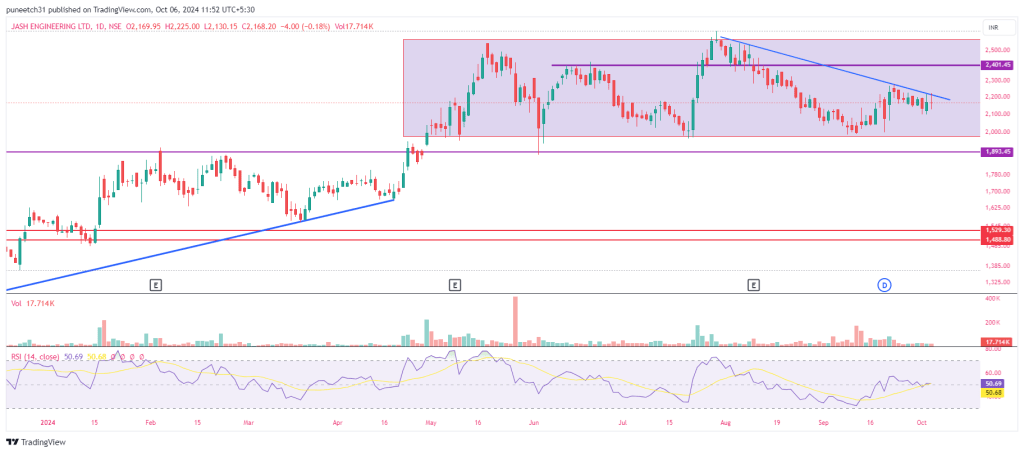

Technical chart on 6 Oct 24

Risks

Large working capital requirement, cash conversion cycle is bit high Trade receivables and Inventory on higher side Rising raw material and commodity costs Increase in competitive bids for procuring the projects

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Likhitha Infra Limited (LIL)

Key Investment thesis –> Increasing Demand of Gas pipeline Infra, City Gas distribution and National Gas policy 2030, Expanding Geographically, Consistent Business and Order book

LIL was incorporated in 1998 and is engaged in the business of pipeline laying providing comprehensive erection, testing, and commissioning of Oil and Gas pipelines, city gas distribution projects, tankage and operations and maintenance services. It is based in Hyderabad, Telangana.

Company has two (02) Joint Ventures viz., CPM-Likhitha Consortium, India and Likhitha Hak Arabia Contracting Company, Kingdom of Saudi Arabia. In addition, Company held 60% equity share capital in Likhitha Hak Arabia Contracting Company, and consequently, now it became a subsidiary of the Company

Has successfully laid over 1500 km of steel pipelines and over 1500 km of MDPE of oil & gas pipelines in the past years. Additionally, the company is laying approximately 1000 km of oil & gas pipelines for the ongoing projects Executed the First Trans-National cross-country pipeline of South-East Asia connecting India to Nepal in the year 2019, for the supply of petroleum products

Strong presence in more than 20 states and 2 Union Territories in India.

Business Segments:

a) City Gas Distribution Projects: This Involves laying of steel and MDPE pipelines for consumers across domestic, commercial and industrial sector, creating a network of pipelines along with associated facilities, Last Mile Connections, CNG Stations b) Cross Country Pipeline Projects: Laying of Cross Country Pipeline projects along with piping, civil, electrical, instrumentation and other associated works c) Operation & Maintenance Services: O&M services include providing skilled manpower, executing emergency repairs, overhauling, scheduled maintenance activities and operation of the network d) Tankage: Construction of fuel depots including storage tanks, Combined Station Works, mechanical, instrumentation, electrical, civil works, F&G system, and other associated facilities

Strengths :

Long standing relationships with domestic marquee customers.

Efficient business model

Strong project execution capabilities

Diversified geographical presence in India

Strong Technical Qualification to bid for new projects

Strong promoter holding showing skin in game

Strong Order Book 1500cr in Jun24

Highly experienced Management Team

Credit ratings –>Long term facilities A/Stable and Short term facilities A1

ROCE>30% and ROE> 20%, DE ~Nil , Free cash flow is good , Pledge is Nil

Stable OPM, Net Profit went 33X+ in 10 Years, Consistent Dividend Payout

Consistent Profit growth, sales growth, ROE over 3 years, 5 years, 10 Years

Promoter has sufficient skin in game at 70% shareholding

YouTube link

Triggers

Macro Trends :

India has set a target of increasing the share of natural gas in the overall energy mix to 15% from present 6.7%.

As per the Government policies, PNGRB has increased the number of Geographical Areas (GAs) to 228 comprising of 402 districts spread over 27 States and Union Territories, covering 70% of Indian population and 53% of its area. These recent Government initiatives have provided lucrative opportunities for Oil & Gas infrastructure service providers

Recent policy moves, including a wide-scale rollout of CNG and the expansion of gas infrastructure including LNG terminals, long-distance transmission pipelines and city gas distribution networks, will help drive 30bnm³ of gas demand growth over the next decade through fuel switching away from coal and oil. A recent switch to CNG from coal in India’s brick industry is encouraging greater gas use.

India is set to dominate the number of trunk/ transmission pipeline projects that are expected to start operations in Asia during 2024-2028, contributing about 43% (62 projects) of the region’s total projects count by 2028. The transmission pipeline length of 29,800 kms is expected to be added, says GlobalData, a leading data and analytics company.

The gas pipeline infrastructure has been seeing intense development activity. The Government of India has set a target to reach 34,500 km by 2024-25 end from 22, 335 km as on January, 2023. Furthermore, plans to connect states with the trunk natural gas pipeline network by 2027 are gathering momentum.

In terms of investments, the Petroleum and Natural Gas Ministry said about ` 41,000 crore ($4.95 billion) are expected from companies to build natural gas pipeline infrastructure in the northeastern states and northern federal territories of Kashmir and Ladakh. The thrust on natural gas and government policy initiatives are in line with India’s global commitments to boost the use of cleaner fuels and cut carbon emissions with the ultimate goal of achieving net zero carbon emissions by 2070.

Expanding presence

In line with growth strategy, Company has entered new markets such as the Kingdom of Saudi Arabia and the United Arab Emirates, where we see substantial opportunities in the oil and gas infrastructure sector. The company has been exploring growth opportunities beyond India. We have formed a joint venture firm in Saudi Arabia and have opened a branch office in Abu Dhabi, UAE to explore business prospects in the Middle East markets which promise long-term growth for pipeline infrastructure development.

The Indian government’s continued emphasis on expanding the oil and gas transportation network and promoting city gas distribution projects provides us with a steady stream of contracts.

India’s energy consumption is on the rise, with the country consuming 19.9 million metric tonnes of petroleum products and 5.51 BCM of natural gas during FY 2023-24. As the world’s third-largest consumer of energy, India’s demand for natural gas is expected to grow fivefold by 2047, in line with the nation’s vision of becoming a developed nation by its centennial year

Good execution and order book and Consistent new orders

Technical chart on 21st Sep24

Risks

Large working capital requirement, cash conversion cycle is bit high Trade receivables and Inventory on higher side Any change in CGD policy Rising raw material and commodity costs The Company is deriving significant portion of orders from major Oil & Gas distribution companies inducing a client concentration risk Increase in competitive bids for procuring the projects

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

A dark store is a small warehousing urban distribution centre exclusively for online shopping with an area ranging between 3,000 to 8,000 sq ft located close to densely packed residential areas to meet quick delivery requirements, Srinivas N, Managing Director, Industrial and Logistics, Savills India said.

Dark stores stock a variety of products and operate around the clock. This enables quick access to inventory, reduces transportation costs, has a quick turn-around time, and improves last-mile delivery capabilities.

However, unlike warehousing, dark stores maintain a limited inventory, often with products having a shelf life of less than 24 hours. In contrast, warehouses store a wide variety of materials in bulk quantities, without the same time constraints on product freshness or expiration.

“The current requirements from quick commerce necessitate dark store spaces of 5,000 square feet or larger. The evolution of quick commerce has managed to establish a firm foothold in the market, which indicates a likely increase in the number of these larger stores moving forward,” Abhishek Bhutani, Managing Director, Ahmedabad and Logistics & Industrials, Cushman & Wakefield said.

Where are dark stores usually located?

A 2021 study by JLL showed that in the e-commerce sector, about 10-15 percent of total kilometres travelled in urban areas contributed to 47 percent of total transportation costs.

This brought dark stores closer to the dense residential areas to ensure efficient and timely delivery. However, real estate costs in urban locations cannot meet retail rental expectations. Therefore, dark stores are usually located in smaller commercial building basements, parking spaces, and defunct facilities in the bylanes or alleyways.

Additionally, these stores are not visited by customers. So, low-cost space is most functional for a dark store.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Aeroflex Industries

Key Investment thesis –> Increasing Demand of HVAC system, Large Scale Industrialization, Modernization in Agriculture and Demand from new edge industries like Aerospace, Satellite, Solar and Robotics

Company is one of the leading Indian manufacturers of metallic flexible flow solutions made with stainless steel used for controlled flow of all forms of substances including Solid, Liquid, and Gas. Incorporated in 1993, co. is part of Sat Industries Limited.

Product Profile: Braided hoses, unbraided hoses, solar hoses, gas hoses, vacuum hoses, braiding, interlock hoses, hose assemblies, lancing hose assemblies, jacketed hose assemblies, exhaust connectors, exhaust gas recirculation (EGR) tubes, expansion bellows, compensators, and related end fittings.

Exports to 89 countries across Asia, Americas, Europe and Africa, through a diversified go-tomarket model

Scalable and Customized flexible flow solution products

Current serving Major Industries

Steel & Metal

Oil & Gas

Chemicals

Sea Port Terminal Handling

Paper & Pulp

Pharmaceutical

Strengths :

Extensive Promoter experience

Employee strength -500+

The company has 2500+ SKUs

Strategically Located Near JNPT Port

80+ machine lines

72+ Products across various stages of Research and Development

14 Qualified R&D Team

NABL Accredited Lab

ISO 9001:2015, ISO 45001:2018 and ISO 14001:2015 certified;

Adherence to global standards

Revenue Breakup

Fundamental Ratios, Cash, EBITDA, PAT

ROCE asnd ROE> 20%, DE ~Nil , Free cash flow is good , Pledge is Nil

Stable OPM, Net Profit went 8X+

Promoter has skin in game + Big Shark Ashish Kacholia holding 3.6%

Triggers

Macro Trends :

▪ Global market for SS flexible hose has grown at a CAGR of 8.2% to value at approximately USD 3.3 Bn in 2022 ▪ Traditionally, the demand for Flexible Flow Solutions made with Stainless Steel Corrugation was largely driven by the industrial sector – manufacturing plants and manufacturing products from chemicals to paper ▪ Between FY’18-9M FY23, over 1,840 projects (brownfield and greenfield) were completed in the manufacturing ▪ With Flexible Flow Solutions made with Stainless Steel Corrugation application being universal, this large base is believed to have supported a strong demand for the product ▪ Given the increasing preference for Flexible Flow Solutions made with Stainless Steel Corrugation in place of rubber / PTFE / polymer hoses, the demand for the former from the industrial sector would be stable

Company has worked on Capacity Expansion, value added products

Expanding our presence to:

Electric Mobility

Fire Sprinklers

Solar

Robotics

Semiconductors

Aerospace and Satellite

Management commentary in Q1Fy25 results

Increasing margins possibilities, Increasing orders from assemblies, Focus on value added offerings, possible inorganic Way of expansion, Acquisition

Technicals

Technical chart on 8th Sep24

Risks

PE is bit high in short term

Large working capital requirement, cash conversion cycle is bit high

Exposure to volatile raw material price

Acquisitions dont play as anticipated

Demand dont originate as anticipated

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.