Leading manufacturer of Supercomputing Systems in India.

Catering to a diverse clientele including prestigious institutions like IITs and NMDC Data Centre. The Company has designed, developed and deployed some of India’s most powerful Supercomputing systems.

Key Highlights • Number of Installations: Netweb is among the top OEMs in India with over 500 HPC installations. • Technology: Equipped with the Tyrone cluster management suite, Netweb has deployed diverse Supercomputing systems ranging from 10 nodes to 400 nodes and is scalable up to 1,000 nodes. • Revenue Growth: Demonstrated significant growth in revenue, with a CAGR of 166.3% over the period of FY2021-FY2024, reaching ₹ 2,624 Mn in FY2024. • HPC installations and revenue has been steadily rising, reflecting Netweb’s strong foothold in the Indian market. The CAGR of 166.3% over the recent fiscal years is indicative of the growing demand for High-Performance Computing solutions. The High-Performance Storage (HPS) segment focuses on providing advanced storage solutions tailored to enterprise computation needs. Netweb’s offerings in this segment include a range of products designed for high throughput and high IOPs, ensuring reliability and scalability. Unified storage solution Parallel file system storage Cloud native storage Surveillance and object storage 336 FY21 217 FY22 308 FY23 339 FY24

Key Highlights • Technological Edge: Netweb’s HPS Solutions are capable of being integrated into private and public cloud environments with no single point of failure, scalable up to exabytes and built-in high availability. • Performance: Supports up to 10 Mn IOPs and 100 GBps throughput, scalable up to 450 GBps, and designs that can extend up to 1,000 petabytes. • Compliance: Developed in-house and compliant with the “Make-inIndia” policy. • Installations: Deployed at major institutions including Graviton, A.P.T. Portfolio, and INST.

Hybrid cloud solutions

The Software and Service for HCS segment provides a comprehensive private cloud software stack to manage complex workloads. Netweb’s solutions include big data-centric offerings designed to cater to dataintensive distributed applications.

Netweb has shown remarkable growth across its primary segments. The Company’s commitment to innovation and quality, coupled with strategic partnerships and market expansion, has cemented its position as a leader in the technology solutions domain. The promising revenue trends and expanding market presence suggest a bright future for Netweb in the HighPerformance Computing, Private Cloud, HCI, and AI Systems sectors.

Key Highlights • Technological Edge: Private cloud software stack to handle complex workloads, including 5G enterprise cloud, 5G edge compute, private 5G and enterprise IT. • Big Data Solutions: Utilises Tyrone Camarero dense systems, Tyrone Cluster Management Suite, and Tyrone Collectivo range of specialised storage systems. • Installations: Provided to marquee customers like NMDC Data Centre and Graviton. • Revenue Growth: Significant growth from ₹ 25 Mn in FY2021 to ₹ 176 Mn in FY2024, with an impressive CAGR of 91.6%

Data Centre Server

The Data Centre Server segment caters to diverse customer needs with high-end server solutions designed for low latency and better physical space utilisation. Netweb’s portfolio includes over 200 dual-processor server models under the Tyrone Camarero brand. Network and Switches Networking and Switches are crucial components in robust solutions like HPC, HCS, and HCI. With the increasing demand for dense computing hardware and microservices-based deployments, networks are playing an increasingly vital role and are set to claim a larger share of the technology landscape. Netweb offers a range of “Make-in-India” Switches tailored to meet these evolving demands. The Company is committed to expanding this range to ensure delivery of optimal solutions to the customers.

Key Highlights • Technological Edge: Dual-processor configurations enabling multiple operations simultaneously, with features like low rack space consumption, high in-built storage capability (up to 1 petabyte), and high energy efficiency. • Compliance: Designed and manufactured in compliance with the “Make-in-India” policy.

• Installations: Installations done for marquee customers including IIT, JNU and HL Mando.

• Revenue Growth: Strong revenue increase from ₹ 168 Mn in FY2021 to ₹ 337 Mn in FY2024, reflecting a robust CAGR of 26.1%.

Netweb Technologies unveils Advanced Make-in-India Server Systems

● Netweb Technologies unveiled its new series of advanced server systems at Hyatt Regency, New Delhi on August 30, 2024, showcasing its commitment to high-end R&D, in-house design, and indigenous manufacturing. ● The new range of systems offers up to 256 cores, 6TB of memory, extensive I/O, GPU capabilities, and storage options designed for High-performance computing and AI applications.

● The launch underscores Netweb Technologies’ dedication to driving progress in the technology industry while supporting the Make in India initiative.

● The ceremony featured live demonstrations, showcasing the advanced capabilities of Netweb’s new range of AMD EPYC™ CPU-based servers.

Capex and New Facility:

New state-of-the-art, end-to-end, high-end computing server storage and switch manufacturing facility inaugurated in Faridabad.

Focus on advanced manufacturing skills to manufacture high-end computing systems using latest generation chips from technology partners like NVIDIA, Intel, and AMD.

Expected to enhance production process including PCB design, manufacturing, and SMT for servers, storage, and switches.

Incremental revenue of 30% to 35% expected from the Faridabad facility.

Strategic Focus and Future Plans:

Three strategic pillars: High-Performance Computing (HPC), Private Cloud, and AI.

Focus on technological evolution to deliver cutting-edge solutions meeting global businesses’ needs.

Development of servers based on NVIDIA Grace Superchip under the MGX architecture in progress.

Launched Intel Sapphire Rapids and AMD Genova-based high-end computing servers.

Diverse portfolio of products including those utilizing the latest NVIDIA GPUs for AI training and inferencing market.

Strong demand in the India data center market, providing significant opportunities.

Expecting growth at a rate of 30% to 35% CAGR for the next 3 years.

Plans to maintain leadership in technology by focusing on innovation and expansion.

Opportunities in the oil and gas sector with engagements from government PSUs like ONGC.

Progressing well in Middle East and European markets with a focus on Private Cloud, HCI, and AI solutions.

Looking into M&A opportunities in related areas to enhance growth and capabilities.

Margin improvement expected in the future due to operating leverage and volume growth.

Challenges and Market Size:

Slowest quarter in terms of cash flow due to high capex expenditures.

Need to optimize the new SMT facility for full production capacity to improve margins.

Quantum computing development still in early stages, not included in growth guidance.

Market size details for the 3 verticals and products to be shared separately due to complexity.

Disclosure : I am holding it from very low levels, Not added/not sold recently

Keeping in mind the seasonality pattern inherent to our business wherein Q1 is the weakest quarter and the major chunk of revenues are captured in the subsequent part of the financial year. We want to highlight that we have also improved our gross margin significantly, which were primarily driven by continuous improvement in the product mix where the domestic defense business contributed to 65% of the topline, followed by exports whose contribution is around 21% and the space with 11.5% with rest of the business coming in from meterology and other sectors

Employee expenses have slightly gone up because of the increase in the number of skilled and professional employees. This is mainly due to our employee addition at our Bangalore facility. At the end of the quarter, the employees count is close to about 1537, up from 1468 at the end of the financial year.

We have created that Bangalore facility for our systems integration and testing, especially in the radar and electronic warfare domain and we have built up NFTR facility also and also assembly hangers to handle and address the radar systems. And also we have created space division in Bangalore facility. We have incorporated 100% subsidiary unit, Astra Space Technologies Limited and that group is basically going to address all future satellite requirements and they are also working in the same facility.

Objective is to get qualified for satelitte integration and launching business. Own satellite launch is the goal in next 2-3 years with synthetic aperture, radar payload ( ISRO collaboration)

Guidance :

And lastly, for the current financial year, we maintain our target which was given previously for an order book in the range of about Rs. 1,200-Rs. 1,300 crores and the topline in the range of Rs. 1,000-Rs. 1,100 crore with the PBT margin to the tune of about 16%-18% on standalone basis.

Import Substitution + Winning Contracts

We made a breakthrough in replacing imported critical wideband receiver for EW project which DPSU has been using for product of foreign make and the DPSU has the production order. Also, we have bagged precision approach radar and repeat order of Doppler weather radars in this quarter. Our anti drone radar is ready for the deployment in the field and we have been responding RFP’s from various agencies.

we define ourselves to be in the IP business. We are in the business of creating IP, enhancing our IP and that can be done both through our own internal efforts as well as collaborations. But eventually we are in the business of monetizing intellectual property. We have embarked on an exercise now aimed at selling out the IP which has been created within the Company and shared to a large extent which we can now either monetize on a standalone basis or combine it with the other IPs which may be available within the Company or externally available to create value. We found that we had multiple products and technologies which had been created and then not acted upon any further post order completion and had just been filed away as the teams got busy in fulfilling other orders. So, taken out of cold storage and updated with the current tech standards, we can productize these technologies on their own, or combine them with other technologies and that is a low hanging route for us. The incremental efforts at making this tech viable and commercial in minimal and offer us easy way to monetize our efforts

Glad to share that two definitive binding term sheets have been signed this past quarter alone, one in the area of chip design services and another in the radar space while discussions have been initiated with multiple companies, both listed space as well as in the smaller unlisted space for enhanced collaboration with the platform, which Astra provides to further enhance our joint intellectual property and create products which are well suited for the future. We are also in a hurry to monetize things at the fastest possible pace and collaborations

Capacity expansion and ability to handle more orders

we enhanced our facility. Recently, we have added auto bonding facility by virtue of which in fact our subsystems that is the tier module of those radars we can produce manifold in the sense about 20 times than what we made it with semi-automatic facility. So, that way we have enhanced our infrastructure, we scaled up our capacity. We are geared up to manufacture as many as numbers as we want.

Order Book

We have crossed the milestone of Rs. 2,000 crores mark this time where the standalone order book as of June 2024 stood at Rs. 2,099 crores and our order wins continues to be healthy. On a consolidated basis, our order book stood at Rs. 2,365 crores as of June 2024. Overall, our order book comprises of 88% of the domestic orders, which are largely BTS, which enjoys good margins and 12% of export, which is a mix of BTP and BTS business. Our consolidated order book consists of Rs. 120 crores worth of service orders, which are typically margin accretive. Our focus remains on getting more orders, which consists of high proportion of complex system projects

Q. top 5 programs that would be critical for our order book accretion and revenue growth in the next 2 years? Management: There are many projects we have been addressing radar and electronic warfare domain especially if you take in the radar, we have been addressing airborne radar and also the ground radars, shipborne radars in all three segments.

Like airborne radars, we have been working for AWC Mk1, Mk1A and also we are waiting for the RFPs for Mk2. . Similarly there is Su-30 opportunities also will come.

Similarly like in the ground segment, there are many radars like we are talking about Tushar like Akash-NG, Akash Prime, WLR repeat orders, these are all which customers DPSS are likely to get. So, we will be getting subsystems from those particular segments.

And shipborne Navy, as I said we are likely to get some repeat orders from Navy.

And in electronic warfare, we have been working for pod jammer for LCA Mk1 as well as we have been working on the ongoing production programs of BEL like Nayan Shakti, Himshakti and all these programs, we are there. And also we are there in the EW programs of like DR118, R118. So, all these programs, we have some orders on hand, and we are likely to get more orders, repeat orders from these customers

Uttam Radar –75% of Radar cost is Antenna –We are supplying exclusively Active Antenna Array units for same. we are expecting around close to Rs. 1,100-1,200 crores worth of business from the Uttam radar in the next 3-4 year’s timeframe

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

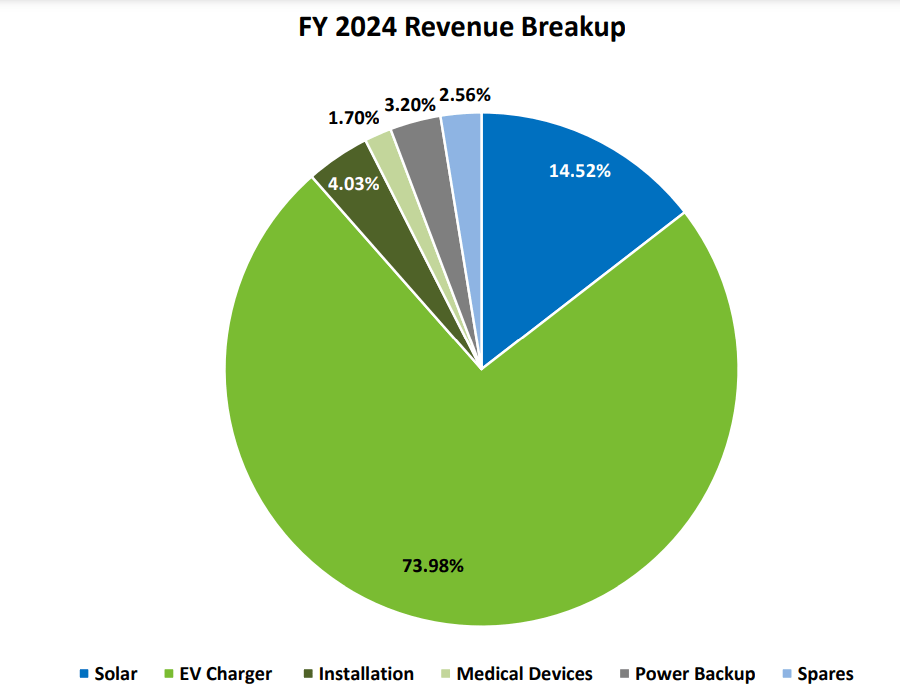

Servotech Power

Key Investment thesis –> Developing EV charging Infra and Delivering Solar Rooftop solutions across India. Key Business wins for EV charging Infra, Association with key businesses B2B

SPSL is in the business of high-end solar products and EV chargers. It develops ultra -fast DC chargers and Home AC chargers, and has installed over 2400 EV chargers in collaboration with oil marketing companies

Product Profile: a) EV Charger: Electric Vehicle Charging Station, AC Charger, DC Charger b) Solar Products: Solar Inverter, Solar Panels, Solar Batteries, ServPort, SMU c) Power & Backup: Battery, Servo Stabilizer, etc. d) LEDs: Domestic LED, Commercial LED e) Oxygen Concentrator: Oxygen Concentrator 5L and Oxygen Concentrator 10L f) UVC: UV-C Handheld Disinfection Lamp – 6W, Portable UV-C Disinfection Lamp – 36W (Sensor Equipped), Portable UV-C Disinfection Lamp – 38W, UV-C Disinfection RoboTruk – 150W, UV-C Sterilization Bag, UV-C LED Sterilization Box with 10W Wifi Charger, UV Sterilization Box with Charger, UV-C Car Intelligent Sanitizer, Car Air Sanitizer, UV Air Purifier, FAR UV-C Digital Sanitizer

Covered the thesis here in quick 12 min Video

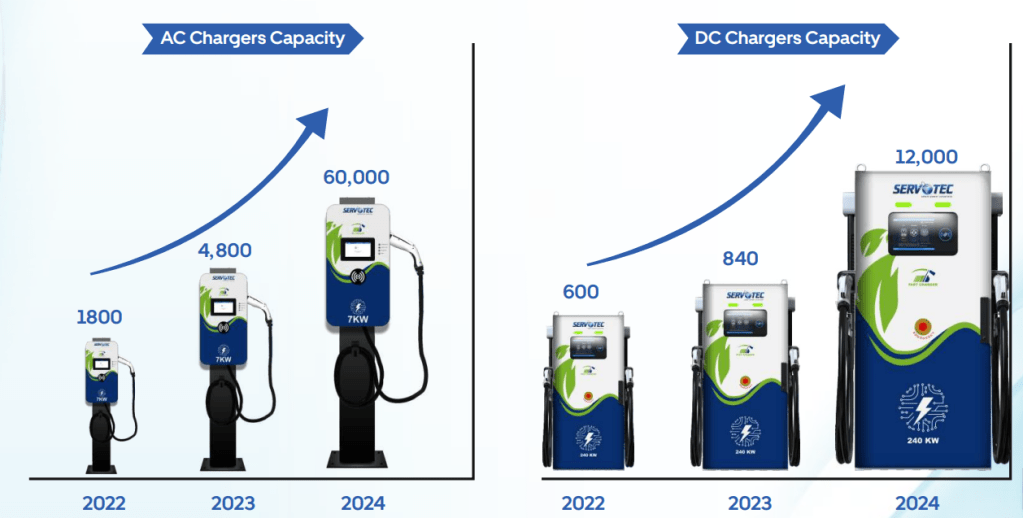

Well-equipped 2 manufacturing facilities spanning over 80,000 sq. ft. and 1,44,000 sq. ft. respectively in Sonipat, Haryana

Capacity to manufacture 30,000 AC EV Chargers and 12,000 DC EV chargers annually

The company is majorly into B2B operations and having Marquee clientele comprising of BPCL, IOCL, HPCL, Nayara Energy, UPNEDA and others

Employee strength -500+

Revenue Breakup

Range of EV AC AND DC chargers

DC chargers have amazing features on fast port, advanced connectivity and user friendliness

Range of Solar solutions

Solar panels, Solar Inverters, Solar Batteries

ESS : Energy storage system (Major tailwinds may appear here)

Solar Street light (too much commodity)

Solar charge controller

EV CHARGER Components

Another interesting solution is Servport

Fundamental Ratios, Cash, EBITDA, PAT

ROCE and ROE > 10%, Pledging 0%, Debt to equity under control

High TTM PE and PB ratio

12X Sales and 12X PAT in 10 Years, Stable EBITDA numbers, Improving NPM

Promoter has good skin in game at ~60% shareholding, FII holding 5% approx

Cash conversion cycle have improved in recent years

Triggers

Macro Trends :

Developing EV charging Infra and Solar Rooftop solutions Infra across India

Journey and recent forays

Government subsidies & policies promoting local manufacturing of EV Components and sustainable energy resources

Growing need for carbon neutral has increased the demand forsustainable energy solution

Increasing demand for EV charging stations with healthy traction in order pipeline in addition to a sizable order backlog. Govt. allocate subsidies of INR 800 Cr to set up 22,000 fast chargers at various fuel pumps across India. The government has sanctioned 2,877 such charging stations across 68 cities in 25 states and UTs. In addition, 1,576 charging stations on nine expressways and 16 highways have also been sanctioned.

Projections indicate that fast-charging stations will witness a CAGR of over 40% by 2025.

New additions in budget 2024 like Pumped Storage Policy and exemption of customs duty on lithium will incentivize renewable energy integration and adoption

Rising urbanization and awareness of climate change have led to increase in demand for cost-efficient products

PM Suryodaya Yojana to solarize 1 Cr Households. 50 solar parks with an aggregate capacity of 37.49 GW have been approved in India

Company has worked on Capacity Expansion

Preferential shares allotment and warrants issued at 83 Rs (approx raised 74cr)

Backward integration efforts for key components (control set and power module) are on track, with the control set already being manufactured in India.

Solar Segment:

Regular monthly sales of ₹8-10 crores in the solar segment, targeting a total of ₹100-150 crores annually.

Plans to expand presence in 20-21 states within two months to leverage government schemes for household electricity.

International Expansion:

Export business is expected to grow, with previous year’s revenue at approximately ₹40 crores and positive momentum for future exports.

Attending international exhibitions and establishing a dedicated export team.

Patents; Innovation and Leadership

51% Growth in the Dealer & Distributor Network

Hired 128+ employees in Q1

Coninuous order wins from Major OEM’s —Current order book stands at approximately 8,000-8,500 pieces of DC chargers, indicating strong demand.

Order win from BPCL worth ₹120 Crs for the supply of 1,800 DC EV chargers

Order win from IOCL and other EV Charger OEM’s worth ₹111 Crs for the supply of 1,400 DC EV chargers

Order win from BPCL for the supply of 2,649 AC EV chargers

Order win from HPCL and other EV charger OEM’s worth ₹102 Crs for the supply of 1,500 DC EV chargers

Signed a contract with Adani Total Energies E-Mobility Ltd. (ATEL) for the supply of AC EV chargers

SPSL will be responsible for manufacturing, supplying and Installing AC EV Chargers at different Airports and other said locations

Collaborated with an international company to enhance its in-house components manufacturing.

SPSL will be constructing a cutting-edge manufacturing facility focused on the production of Power Modules, Control Circuits, and PLCs. The new plant will have an initial annual production capacity of 24,000 power modules & will ramp up its production capacity to 2.4 lakh power modules annually

Solar energy storage

Servotech Secures Order of around 1.2 MW Solar Energy Storage and Grid Connected Systems from Rural Development Department and UPNEDA. Servotech will be responsible for installing multiple 75kW solar-based energy storage systems, designed to provide reliable and uninterrupted power supply across Uttar Pradesh. Additionally, the company will also be designing, manufacturing, supplying, erecting, testing and commissioning 20 kW and 40 kW grid-connected solar power systems, contributing to the state’s renewable energy goals. This order will prove to be essential for overcoming geographical and infrastructural challenges in areas of Uttar Pradesh by enabling a broader reach of sustainable energy solutions and ensuring the penetration of renewable energy into the grid.

Creating new subsidiary “Servotech Sports and Entertainment Pvt. Ltd.”

Servotech aims to capitalize on the sporting fervor, its immense popularity, and global appeal to strengthen its brand presence and connect with a wider audience base. This strategic alignment presents an exciting opportunity for Servotech to extend its reach beyond its industry boundaries and tap into new avenues of success and engagement, establishing itself as not just a leader in the EV charging and solar energy sectors, but also as a prominent player in the sports industry.

Technicals

Technical chart on 21st Aug24

Risks

Consistent Equity dilution, consistent increase in borrowing and Negative cash flows poses risk to company business growth

PE is high and any 2 bad qtrs can screw the returns profile from the current levels

Large capital working requirements is another thing to watch out for

Highly competitive industry both in Solar and EV industry

Delay in projects due to Govt policies or Land acquisition issues

Components import is another risk

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Time technoplast Became 5X for me in 2 Years approximately

Business :

🦕Continued focus on growth, cost reduction by automation and re-engineering of machineries and moulds, etc. and improvement in working capital cycle which will ultimately enhance net earnings and ROCE… pic.twitter.com/PfDRTvE8Wu

Optiemus Boosts Atmanirbhar Bharat with foray into Telecom Equipment Manufacturing

As India moves into the next phase of its telecom and electronics manufacturing revolution, Optiemus Electronics today announced that it has forayed… https://t.co/4k8bkcJFYPpic.twitter.com/n6oPitBa5r

Genus Power Infrastructures Limited’s wholly owned subsidiary has received three Letter of Awards (LOA) worth totaling to Rs. 2,925.52 crore (net of taxes) for appointment of Advanced Metering Infrastructure Service Providers (AMISPs) including design of Advance Metering… https://t.co/MUYjD5KCnfpic.twitter.com/HMk3jOkvPz

🦕Advait Infratech Limited (AIL) has successfully achieved a significant milestone under our strategic alliance with Guofu Hydrogen Energy Equipment Co., Ltd. (Guofu Hydrogen).

🦕This partnership was formalized in 2024 through an agreement signed by both parties. Under the… pic.twitter.com/780gmF05rT

Some Updates from recent Quarterly results INOX INDIA

💠Order received from one of the Indian PSU for 10 Nos LNG Fuelingstation 💠Additional order for Vacuum Vessel Thermal ShieldrepairforITER Project 💠Further bulk order is received from emerging LNG truck mfg. company for… https://t.co/J6GuE5Wowe

🔯HPC 💚Leading manufacturer of Supercomputing Systems in India. 💚Catering to a diverse clientele including prestigious institutions like IITs and NMDC Data Centre. The Company has designed, developed and deployed some of India’s most powerful Supercomputing… pic.twitter.com/HGaPaJYmEW

Indian equity market is now at a point where every theory, thesis, formula and literature about stock markets, stocks and investments, has been run over by a king size bulldozer, and whatever remained has been burnt with a flamethrower.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

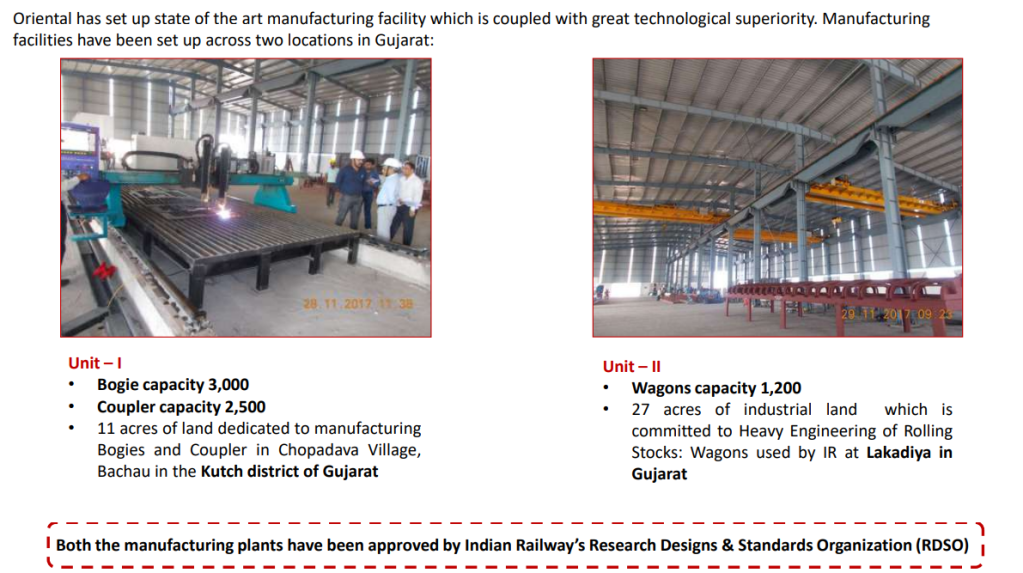

Oriental Rail Infra

Key Investment thesis –> Providing Infra to Railway sector. Govt focus and orders landing up fast to Railway vendors. Oriental rail Infra is prime contender for seats and birth for new coaches. Apart from that New wagons orders also flowing

Oriental Rail Infrastructure Limited (ORIL) (formerly know as Oriental Veneer Products Limited) is engaged in manufacturing and supply of rail products predominantly for Indian Railways(IR). It manufactures Seats and Berths, Chairs, Lavatory doors etc. for all types of passenger coaches. It also manufactures Heavy Engineering equipment’s like Railway Rolling Stock, a diverse range of products which includes Wagons, Bogie, Coupler & Draft Gears through its wholly owned subsidiary Oriental Foundry Private Limited (OFPL).

Manufacturing Facility for Silicon Foam, Seats and Berth, Rexine, Compreg Board, PU Foam used for Seats & Berths, Recron used for Seats & Berths

Only Listed player in Seats & Berths in Organised sector

RDSO Certified and preferred vendor

1000+ employee strength

This Wagon capacity has been increased to 2400 wagons in Sep2023

Preferential shares allotment and warrants issued at 169 Rs (approx 200cr raised)

Order Book and strength

Company has a strong order book of more than 1200cr

Strong promoter background

3 decade old company

Big clients

Fundamental Ratios, Cash, EBITDA, PAT

Sales and profit 7x and 10x approximately in last 9 years

ROCE and ROE >12 %

Debt to equity is okayish at ~1, Pledging is 0%

Promoter has good skin in game at ~55% shareholding and big players entered recently including Mukul Agarwal

Triggers

Macro Trends :

Amid rising demand for coal freight and an aggressive push towards diversifying its freight basket, IR is planning to buy 1,00,000 more Wagons over the next three financial years Under the National Rail Plan(NRP), Centre wants to significantly increase the national transporter’s freight numbers, along with its modal freight share to 45 per cent by 2030. As per GOI estimates, consolidated demand for freight will be over 6,300 Million Tons (MT) by 2026 and 8,220 MT by 2031 Having ferried 1,418 MT in this fiscal, the national transporter would need to account for over 3,600 MT in 2031 to meet its NRP targets.

Company has worked on

Backward integration, Capacity Expansion, High Value Products and Client Diversification

Technicals

Technical chart in 10th Aug24

Risks

Working capital intensive nature of operations

Operating Cash flows are not good. Working capital days, Cash conversion cycle, ROCE, ROE needs to improve

Strong dependency on big customer IR

Margins are fluctuating in past based on execution and delivery. Not easy to predict bad or good quarters for company business

Susceptibility of profitability to volatility in raw material prices – ORIL’s product mix mainly includes seats, berths, compreg boards wherein the major raw materials are wood, rexene, cloth, foams, recron and various other solvents. Major raw material is supplied inhouse like company manufactures rexene and foam useful in manufacturing of seats. Other raw material consumed for manufacturing of seats includes veneer, which is formed from timber and company procures timber from local market. Its profitability is susceptible to fluctuations in the prices of wood as it serves as the main raw material for manufacturing of veneers, particle boards, plywood and compreg boards. For wagons, bogies and coupler body, major raw material is steel or scrap of steel which is procured from local market whose prices are highly volatile in nature. However, the company has a price variation clause inbuilt for key raw material, i.e., steel and wheels if procured from Indian Railways, thus reducing the price volatility to that extant

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

For a long time, most people agreed that if you wanted to start a tech company, the “default” place to do it was Bengaluru. It had everything that young startups wanted—a vibrant city, access to tech talent, VCs, and even great weather. For over a decade, some of the most notable startups emerged from Bengaluru. Everyone believed this was an advantage, i.e., the ecosystem made these companies stronger, resilient, and more innovative.

But of late… we aren’t so sure about that. Even though most people in Bengaluru believe that they are doing exciting, innovative work, it’s the startups from another city…

Valiant communications Disclosure –holding from below levels , one of my bets that hit 10x still a good potential for 3x-5x from these levels Target –> 50x from Valiant communications

You decide your own risk, reward

Not a recommedation to buy sell

RECENT RESULTS – Highest Sales, PAT

Key updates captured from Company presentation

Valiant had entered into agreement(s) with its business partner Tejas Networks Limited to present their joint bids before the Gujarat Energy Transmission Corporation Limited (GETCO) for two different projects, wherein, Tejas has acted as a lead bidder in both the projects.

For Project #1, the GETCO has issued the Letter of Intent (LOI) to Tejas, being the lead bidder. Valiant isexpected to receive the corresponding confirmed order of exceeding 3,400 lacs from Tejas in the ongoing quarter.

For Project #2, Valiant with its business partner Tejas, are L1 bidders. This Project is to be issued under the “Make-in-India” initiative with a business opportunity for Valiant exceeding 3,200 lacs. The outcome is awaited.

Quantum-safe features in Valiant’s cyber-security products and solutions are under development and commercial role out is expected within the calendar year 2024.

The operating profit margins has been improved in the light of: Expected better product-mix; Earlier years supplies are entering in AMC phase now, resulting a top-up revenue for services; New cuƫng-edge hardware technology driven products are being offered.

VCL-NAS and Data Storage Servers: Valiant has introduced India’s first, Made in India ransomware resistant, OnSite, Off-Site and Off-Line Data Storage and NAS (Network-AƩached Storage) Servers with a current capacity of 1.2 Petabyte (i.e. 1,200 Terabytes). Valiant’s VCL-NAS is an essential component of the modern networked computing environment including data center applications. VCL-NAS comes equipped with incremental upgrades using AES 256 encryption and upgrading to Quantum-Safe technology. It allows the protection of stored data against natural disasters, man-made disasters and acts of war – including EMP (electromagnetic pulse). Off-Site VCL-NAS and Data Storage Servers are used for Disaster Recovery ensuring that critical data is still accessible and can be restored. Off-Site backups are used for Data Redundancy to provide redundancy, reducing the risk of data loss due to hardware failures, human error, or software issues on the primary server. VCL-NAS and Data Storage Servers can also be used for Geographic Diversity to restore data in geographically distant locations, overcoming the risk of natural disaster, acts of war including EMP aƩacks. Another key feature of VCL-NAS and Data Storage Servers including providing Air-Gap Security. Data stored offline, is immune to online threats such as hacking, malware, and ransomware. Grid Automation and Grid Islanding solution: Our Company has also introduced its Grid Automation and Grid Islanding solution

Copied key contents which I liked from AGM transcript.

Disclosure : I am holding it from very low levels, Not added/not sold recently

we have consolidated our existing business in satellite communication for defence applications, we are also diversifying into two different areas and the results we expect to see in two years from now in a big way.

So, and we are very confident that both these initiatives will put the company in a different orbit. From 2026 -27 onwards, we expect to see the results. And from 2027 onwards, the three years from now, there will be a quantum jump. we expect the company to establish itself as the top five companies in the country in the space of defence

First diversification that we are doing is the software defined radios. It’s a big, huge market globally. But if you come to very specific to India alone itself, it’s around $11 billion market globally. But coming to India in the Indian Defence market alone, it’s, it’s around, it’s around $300 million leaving the civilian commercial market only Indian defence market per annum. That is $300 million is per annum

we would be number two, I mean, if I’m not wrong, in that space of SDR’s with SCI compliance and that covers various spectrum like HF, VHF, UHF, L band, Satcom, SDR. There are various frequency bands and various versions of them for like portable versions, handheld versions with vehicle borne aircrafts, helicopters, shipborne submarines

C4ISR is the basic backbone of any, you know, any defence service, which includes command, control, communication, computing, intelligence, surveillance and reconnaissance

We are planning to complete a range of products by this year, financially and itself, but we expect to see a good revenue and all from 26, 27 onwards. By 2027, we should have, we consolidated as a serious player in that segment in India. And these products will also have possibility to expand in the global market.

second diversification is in the space sector where there the government of India has started opening up the sector very seriously and they want to see that private sector enters BLO, build, launch and operate kind of services. So in all the both upstream as downstream and midstream services in satellite space will be open to the private sector either through partnership with public sector or, government. Public private partnership or private sector alone government of India is looking at something like $50 billion in the next eight to nine years

we are well positioned to expand our presence in the space sector by getting into two areas.

One is ground station as a service like it includes satellite operation Centre, mission control Centre and also receiving the data and images from the satellites. Their station is supposed to receive the signals from satellites and then distribute that to the customers.

And the second part is the assembly, integration and testing of the satellites themselves. There up to satellite weight of say 1000 kgs max. We should be able to do it in house. So we are establishing a facility in ECT electronic city in Hyderabad. It is near airport. It’s about four acres of land. The construction is going on and we should be able to complete that facility in all respects by this year end. So there two things

Orders we have around 287 crores worth of orders on hand right now. there are a lot of other things in pipeline railways now, we are well established. We are expecting another 60 crores order, approximately, and maybe in a month or two and followed up by another tender coming up. They are coming up for I think maybe 12,000 terminals. So that will be a public tender. NSIL, we are doing, I mean, we have an order for around 27,600 or so

Five-kilowatt HF system we have already delivered and that has only been delivered to Indian Navy, government of India through bath electronics, installed and commissioned. So, there’s a good requirement in that space. And right now, A, we have the product in hand and we are ready for that. So, whenever the RFP comes, we are. That will be a big opportunity. Maybe few hundred crores.

we want to work on satellite payloads also which is again state of the art kind of development work. Subsystems for satellites. These are highly manpower intensive kind of work. So, the manpower expenses in R and D will grow a lot significantly in the next three to four years because we are investing heavily in R and D in those software, different radios and satellite subsystems right now. We have five projects sanctioned by Minister of defence government of India and five is the maximum they can give to any company. So, and we got five out of this. Two contracts are signed. One is in the final stage of contract signing. Maybe this month, June they will sign another one, maybe in June end or July. So enough. There are two major projects we have signed wherein once we complete the development, we’ll be the only vendor for those requirements. And those projects are having high potential because we’ll be the single vendor and those projects are having huge requirement from Indian army

Government of India is giving a grant for those projects, investing in that. And they are investing in their time and effort to do the trials, conduct the field trials for these projects. So earlier we have to understand the requirements, develop the product without anything, no cost, no commitment basis, go after them to conduct trials and accept that. Now it has come from them. They are given the specs, they have given the requirements, they are giving the grant and they are saying once it is completed, they will buy from us. So, it is like a phenomenal change in the outlook from the government of India. And in terms of making India and self-reliant, I think they mean business

Receivables Receivables we have, because we did 38 crores in the last quarter. I mean there is some, it appears to be more, but we have already received close to 39 crores from those 68 crores. And in that again around eleven crores is towards installation commissioning which will come over a period of time as we complete the installation of the equipment and all crores, another remaining eleven crores we should be receiving in June or July. So, there is absolutely no, as you could see, there are no bad debts at all for the company and they are, if they are there also, they are minuscule, 0.001% something like that. Because all receivables are from government of India or government of India undertakings.

IMax opportunity we may do some two and a half crores or so next year. Then following year maybe, we may even go up to ten crores, then 15 crores. But we are confident that we will reach 100 crores by 2030. So that’s not a very ambitious target because of the market here is around $11 billion and we are importing about $7 billion every year in medical equipment. That sector, which is about $7 billion, is the import itself around 60,000 crores or more they are importing. There is a huge potential there that is also expected to go to $50 billion by 2030. we are very well positioned in that because our expertise in electronics and engineering and mechanical, everything is very helpful in making world class equipment. We are not compromising on quality or anything. We are trying to build artificial intelligence into that. We want to make this equipment IOT enabled and benchmarked against the best in the world. So, there is no doubt that we will do well in image. It’s only a matter of time. So, But the break-even may happen. Maybe if not this year, next year definitely it will break even and get into cash profit. We’ll make profits in 25, 26 for sure. And after that the growth will be exponential. So, the I max would be a very, very significant

we are positioned in a place called AP MedTech zone where the world class facilities are created for complete testing and certification. It’s world class, it is recognized by WHO also. So, our facility is coming up in that 300 acre or something kind of a thing, where there is incubation centre, the test labs, certification labs, and many companies also have already started operations about four or five years back, and they’re doing extremely well. So, in that we have chosen space where two, three areas we have identified.

One is the respiratory area, like. Like ventilators and C Pap, BiPap and things like that. Then we are selected. Endoscopy is one of the areas And of course, to start with a low, low-end side, we have taken surgical staplers where it is certified. And then we, as I briefed you earlier, we got a contract for supply, 25,000 numbers per month from another OEM company. So, we’re on the right track. And then the final, we also want to, as I rightly, as I told you earlier, we want to develop something called hospital at home kind of equipment, which will be very useful for in times like Covid or for elders or for communities. So where in a budget of, say, ten lakhs, you can have everything that a hospital can provide. In an ICU, which is a small, it’s an equipment which will be carried on a cart or something like that, which will monitor all vitals. It will supply oxygen, it will have ventilator, it will have infusion pump to infuse injections and all. It will monitor all the vitals. They will be communicated to the doctor. Essential medicines will be made available there. Simple. Some small blood tests also can be done. So basically, it is like everything that you can ask for in an ICU, kind of things will be made available. Any nurse can handle that. And as the vitals are monitored remotely and doctor can be. Will receive alerts and then he can give guidance and then nurse can attend to that

are we able to develop any new products now which will help us be ahead of the competition for the next three, four years and enjoy similar margins? Dr Abburi Vidyasagar- Actually we are continuing that initiative in developing intellectual property. The fundamental focus of the company is on innovation. Always it’s an innovation driven company, though we give very lot of importance to customer service and operational excellence, which are also required to make our company profitable. But the core is innovation only even today.

we have already started working on software, different radios with SCA compliance for Indian as well as global market in defence communication. That is going to be. I mean, there will not be many companies in that anyway. Okay, I don’t say zero competition. There will be competition, but there will be limited competition. Similarly, the ground terminals I am talking about in KU band, cultivating Gaga band, which is again, very few companies will be there. I mean, the satellite terminals I am talking about, which are portable, mobile, you know, airborne, those versions which can be mounted in aircraft or a helicopter, those satellite terminals, again, very few companies will be there

Avantel AGM 2025

we have taken up five projects, 5 projects from the Ministry of Defence under the scheme of iDEX Indian Defence Challenges. So, the projects are mostly related to satellite communication. In fact, all the five projects are related to satellite communication. And the first one is sat phone based on geostationary satellite. The second one was again Convoy Management based on satellite. Both are for Indian Army. The third one is the receiver for receiving video through satellite, again for Indian Army. Port and 5th projects are for the requirements of Indian Navy, which is mostly based on Satcom on the move, the communication on the move for both land-based platforms as well as for the airborne applications. So, all five out of the five project, the 5th project contract was signed recently, but the fourth projects were signed quite some time back about six months back and the development work is going on very well

we have come for rights issue which is that near Vijayawada about an hour from the airport of Vijayawada, it’s on the highway. So that we would like to use for you know, making antennas which like HF antennas which are very huge and in terms of occupy a lot of space, 5 kilowatt HF antennas, one kilowatt HF antennas and then other types of antennas use it in military applications as well as sat com ground station antennas for say 7.3 meters, 9.3 meters, even 11 meters satellite (Not Clear) antennas can be manufactured there.

we are meeting all the requirements in terms of production as well as design, development of various products for MSS, particularly MSS mobile satellite services and UHF, SATCOM and UHF LOS radios, HFSDRs and HF one kilowatt systems and the real time training information systems, fishing transponders for boats from the Department of Fisheries through NSL.

The growth again using CAGR growth. So for example, in 2021, the sales was 77 crores and now 24-25 it is 248 crores either kind of almost it’s more than it’s about 3 times 300%. If you look at the profit, it was 15 crores in 2021 and now it is 24-25 which has come to about close to 60 crores, 59.56 crores see this is about almost four times Ok, the 400% something like. So this kind of increase you, I would like to caution you will not be there for next couple of years in 25-26 and 26-27, which it will be more stable and from 27-28 again, you can expect a steep growth. If a couple of opportunities from say 4 to 5 opportunities, 5 opportunities are there, which are likely to take us to the next level of growth to say sound 50 crores turnover supposed to be aimed to reach by 2030 to reach that kind of from say sound 50 again, 300% again over a period of four years. So that is possible from if we can convert two out of five to six opportunities that we are working on, which will get us good numbers in terms of both sales as well as the profit

l. Coming to IMAX, so as I told you in the last meeting, this medical equipment requires certification, Ok. The certification process will quite elaborate and go through and has to go through many levels of testing particularly things like those noninvasive ventilators and then you know CPAP patient monitoring systems. Those things have to go through a lot of processes that for certification. But the total money, if you to put them in the right perspective the startups with one single product also I have to remain investing at least 5 to $10 million. And all the money that we have invested here is close to $4 million, not even 4 million rather than 4 million. And if we have around 5 products in place and the certification process will be completed for all these products by September for sure. I mean some of them we got already and some of them by June this month end, some of them July end one more and August one more and September. So in the next three months we are getting all the certifications. Plus we have to build a facility with a clean room and other things. The kind of world class facility built and out of 30 crores close to 22 crores has gone for fixed assets. There’s nothing that and you can assume that eight crores have gone for product development. So basically we laid the strong foundation for IMAX to go forward and if any of the shareholders are very, very, I mean worried about this, then the promotes can take over if required. So, but thing is the medical industry, the projections are from $12 billion in 23-24, they are expected to reach $50 billion by 2030. That is the kind of growth they are expecting in IMAX

. I’ll come to the first point that and he also was asked about unsecured loans and all that CDB. There are two reasons for which the shares have been sold. One is to subscribe to the rights issue number 1. number 2 is Laxmi Foundation. I have donated quite some time back the 45,00,000 shares and obviously that donated means I want to sell the shares and invest in the trust for building the hospital, which we already have a hospital in leisure premises and we want to go for our own building for the hospital, much bigger hospital, maybe around 200 bed hospital, multi-specialty hospital. So we have to, I mean, I’m going to not stop here. I’m going to maybe donate more, another 45,00,000 shares or maybe another 45,00,000 shares, maybe another 90,00,000 shares for every next 3-4 years. So that’s and I think that’s my privilege to donate. And then once we donate, they have to be sold to be able to invest in the foundation activities. So I think that’s obvious and I hope shareholders understand that point. Regarding these loans unsecured loans because the company because suddenly the lot of projects were implemented and obviously the receivables have to come from government PSUs and where there were delays, there were delays in receivables. So instead of rushing to the bank. So whatever money I wanted to got to invest in rights, I have invested as unsecured loans here because it is the easiest route for me to fund immediately.

e SDR market is around 3000 crores every year for the last, so many last 7-8 years is buying from different services is about SDR business for military segment alone is that much so and obviously it’s not something that you can do overnight, then everybody could have done it, you know, So for Avantel also, it takes time to do as per software communication architecture, SCA 4.1 specifications and kind of stringent requirements that army and the navy are asking for, including Air Force that shows that the kind of intellectual property that is involved in development of SDRs and Avantel’s capability number one is we are already supplying HFSDRs 1 kilowatt HFSDRs is being supplied to Indian Navy and the shipyards. So our competency and capability is already proven. We have delivered. We are already demonstrated and trials have completed for UHF SDR and UHF sat com SDR to Indian Navy in trials on ships. So there also it’s not on the board drawing board. It’s proven. And 3rd, as you can see, we are selected by Deal Dehradun as against competition from Bell L&T and other major players. So we are short, we became L1 and we are technically qualified. So and those radios are meant for Indian Air Force, Ok, so airborne SDRS for which we have been we got the received the contract also they gave us two years, but I am sure we will develop much before that. Ok. That’s a four channel radio now. Right now they are being imported. This is an import. Two companies were there and we are L1 and some company L2 both of us shared the order, other one is Coral yeah. So that that’s about the SDR capability and development and the big numbers. Defence Services in the next maybe one year. So we are participated in the RFI and if definitely qualification criteria we have to see how much turnover and all that individually or through conversion we will bid for that. That’s big number. So in that the product that is required for that is in am advanced stage and definitely we will meet the requirements. We have given the complaints for all the requirements and it’s that development is going on now, right now at ECT facility in Hyderabad, Ok, when that is 12,000, you can, I don’t know it will be 3000 crores or by 10,000 crores. It depends upon the kind of estimate they have for this product. But definitely I’m sure it will be around maybe 3000 crores or even more, Ok. So that’s the kind of segment we are positioning ourselves and there are entry barriers. There is not something that everybody can by investing money they can develop the product unless the import and obviously imported the equipment are at least 100% more expensive than what is developed by Bharat Electronics. Not even a lender in Bharat Electronics is giving it a competitive price when compared to imports. Dr. Ajit may correct me if I’m wrong. So this is about the SDR part about win profile radar. Yes, we have the technology. We already delivered sharp and two more tenders are coming. One tender is expected this year. One tender is already come. We have already participated in the bid and it may be opened anytime, maybe in the next couple of months. And the next one, the RFP for us may come in the next 2-3 months and we are very confident that we will be there, one for Indian Air Force, One for ISTRAC

Somebody’s talking about 100 crores less or something kind of order. This 100 plus crores of orders will come this year itself and other things like ground stations and all that. One good news is we have a good collaboration with Safran France, the one of the best companies in France, in aerospace, not only in France, in the Europe itself and maybe in the world. So they are, we are collaborating with them for all the ground station 360° coverage, full motion antennas for satellite data reception,

we have already tied up with one company in Med Tech industry for Health Kiosk and we will be doing the contract manufacturing for them. And also we can also sell directly also. It is a very good product. It’s called help pod. It’s like an ATM for healthcare. There are many, many parameters automatically measured. Maybe it’ll take 15 minutes maximum, Max that is otherwise all together, actual measurement time is 5 minutes. So that health part like an ATM Kiosk and we have some requirements. It can be proliferated both. In fact, there’s a potential in military also for that along with our home care product which can be moved into ambulances, army vehicles, trucks and health centers everywhere. It can be fixed along with the H pod. H pod and our health home care unit together. It will be like a mini hospital during diagnostics and service. So both are very good products and the home care product when it comes, it integrates multiple technology. It will have x-ray, ultrasound scan, patient monitor, ventilator. It will have everything that you can ask for to like in whatever is there for the best possible treatment in hospital. So that’s our product and HPOD is the product from Satyendra Goyal who is from Chicago, USA.

They have developed it and they want us to partner. We have signed an MOU also and that is another great opportunity. And in Imax when, when we when we start producing, after the certificate get, start get going, the growth rates will not be 10-15%, but they could be 40-50% year on year or even more 100% or something like that. So once it starts with some 4-5 crores this year, afterwards it could be 30 crores, then it could be 60 to 75 and then hundred. That’s the kind of potential that is there in that area in highlights

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

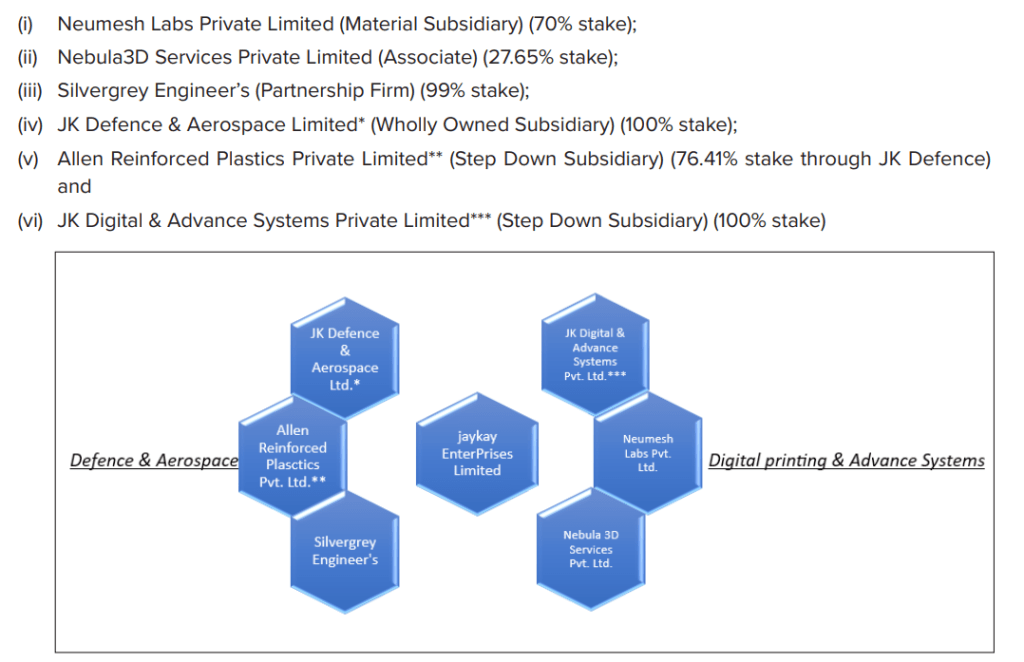

Jaykay Enterprises

Key Investment thesis –> Defense and aerospace sector venture in precision manufacturing with big customerssupported by designing, development, manufacturing, and testing of advanced composite engineering products made or composed of fibre glass, glass mat, plastic, resins etc.with applications in defence/aerospace/ logistics & electrical industries. Company also developing good capabilities in Additive manufacturing and software systems to support above venture

Jaykay Enterprises Limited (JKE), part of J K Organisation and part of the 139 years old diversified JK conglomerate. JKE initially engaged in the business of manufacturing nylon and acrylic fibers and later went into Registrar and Share Transfer Agent activities.

Presently, the Company has diversified itself into Additive Manufacturing systems,Proto typing, powder metallurgy, large scale Digital manufacturing, Reverse Engineering, Plant modelling, In the area of defense & Aerospace we focus on areas of engineering products across various industry verticals, software designing and development, manufacturing of parts and accessories used in defence and aerospace sector, our work includes composite applications, Under water mines ,machining for aerospace sector.

Product segments

The Company has consolidated its business focus into specific dedicated opportunities. a) Defence & Aerospace; b) Digital Manufacturing & Advanced Systems c) Software &Services d) Real Estate & Hospitality. The Company is operating business of manufacturing of precision turned components and all type of engineering goods for the defence, aerospace and other allied industries including Manufacturing,trade and deal in all kinds of products related to Defence and Aerospace and Additive manufacturing and Technical Consultancy Services, 3D Scanning,Reverse engineering ,Plant Modelling, design, develop and market software products for 3D and activities through its subsidiaries, Joint Venture, partnerships and associates.

Management Pedigree

Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited and scion of one of the best-known business families of India. He is the cofounder & has served as Managing Director of JK Technosoft Ltd (‘JKT’) and leads the company’s global operations together with the Board &Management Team. He has invaluable experience within JK Organization companies, handling various aspects of J K businesses, managing business units and operations as well as spearheading successful national and international expansion programs. He has rich experience in the manufacturing & IT services industry and multi-dimensional expertise in basic & core sector industries such as – textiles, synthetic fibres, cement and chemical processing, both in continuous as well as discrete manufacturing, Mr. Singhania has deep insights in Software Development Life Cycle (SDLC), Project Management, Strategic Planning, Business Development, Thought Leadership. Mr. Singhania spearhead in Carving new business opportunities and managing strategic investments in Defence & Aerospace, Digital Manufacturing (3D & Processing), Digital Transformation through acquisitions. He is an alumnus of IMD Business School.

SWOT

Fundamental Ratios, Cash, EBITDA, PAT

Sales and profit catching up in last 2 years

ROCE and ROE <10 %

Debt to equity is under control 0.35, Pledging is 0%

Promoter has good skin in game at ~56% shareholding and stake is increasing while Public stake is decreasing

Triggers

Macro Trends :

INDUSTRY OUTLOOK Defense & Aerospace Sector outlook is very positive owing to huge requirements from the domestic market. The A&D market in India is estimated to reach around US$ 70 bilion by 2030. With a focus on indigenization by GOI the sourcing from within the country will increase many fold resulting in great opportunities for companies in this sector. The additive manufacturing market in India is increasing slowly but surely. The GOI has already come up with a policy. The early entrants will have an advantage over others. The application of this technology globally has entrenched Defense & Aerospace, Health care and oil & Gas Sector. Digital manufacturing will lead the global manufacturing sector in a decades time

Joint Ventures And subsidiaries

JKE had entered into a strategic partnership with the global leaders in 3D Metal design and printing market. JKE had signed a Joint Venture and Shareholders Agreement with M/s Additive 3D Pte Ltd(A3D) an affiliate to M/s EOS Singapore Pte Ltd and consequent upon which a JointVenture (JV) company had been incorporated in the name of M/s Neumesh Labs Private Limited (‘Neumesh’) on 01st January, 2021, with shareholding of JKE and A3d respectively is 70% and 30% in said JV Company, inter alia, in the business of the 3D printing technology in India.

Neumesh Labs Private Limited

Neumesh Labs Private Limited (“Neumesh”) has established a Centre of Excellence (COE) in Bengaluru, the COE has state of the art EOS Software, Machines & Practices of cutting-edge 3D technology. Further Neumesh has developed a 3D printer JKPrint500, which was unveiled in IMTEX 23 Fair in Bengaluru. The product has received enthusiastic market response. Neumesh is also developing a lower price 3D printer which will be targeted at the mass market.

Neumesh, has also started its AM labs business. This is in line with various State Governments opening COE across engineering colleges and ITIs’. GOI in its 2023 budget announcement stated its intentions to establish COE’s across the country. Considering, huge numbers of COE’s that will be established, the demand for high quality polymer printers for training purposes will be high. Therefore, Jaykay Enterprises Limited along with its eco system partners have indigenously developed a polymer printer JK Print 300 and JKPM3 series, a Powder Management System which was unveiled in IMTEX 23 Fair in Bengaluru. The initial customer response has been encouraging. The JK Print 300 Printer is suitable for usage in prototyping, consumer goods, Automobile, and architecture for low volume production. The machine is ideal for usage in low volume production and training of students and technicians. The JK PM3 Powder Management System will optimize productivity and economics keeping in mind highest quality standards of parts produced by 3D metal printers. Neumesh, is working in tandem with the Governments Make in India program. Neumesh has started working on IAF prototyping projects and is looking closely at the MEA Oil & Gas market.

JK Defence & Aerospace Limited (“JK Defence”) and Allen Reinforced Plastics Private Limited (Allen)

JK Defence & Aerospace Limited (“JK Defence”) has acquired the 76.41% equity stake in Allen Reinforced Plastics Private Limited (Allen) which is engaged in the business of designing, development, manufacturing, and testing of advanced composite engineering products made or composed of fibre glass, glass mat, plastic, resins etc. applications in defence/aerospace/ logistics & electrical industries. Allen indigenously develops and supplies critical components to key defence projects in the country, such as BrahMos, Pinaka, SMILE, Akash missiles etc. to defence undertakings such as DRDO, ISRO, OFB, BHEL, BDL among others.

JK Defence stake in the step-down subsidiary i.e. Allen will increase from 76.41% to 92.92% after recent aquisition of shares through Rights issues

JK Defence & Aerospace Limited, Wholly Owned Subsidiary (“JKDAL”) of Jaykay Enterprises Limited, has been accorded an approval from the Office of the Commissioner for the Industrial Development and Director of Industries and Commerce, Government of Karnataka w.r.t. the investment proposal of JKDAL to establish a unit for manufacture of “Precision Turned Components and all types of Engineering Goods for the Defence, Aerospace and other Allied Industries including assembling in all kinds of products of Defence and Aerospace Equipments”. The approval includes allotment of 5 acres of land from KIADB at Devanahalli General Industrial Area (ITIR), Bangalore Rural District and necessary permission for water and power connections and associated NOC(s) from state industry authority. The unit will be eligible for incentives and concession as per applicable policy of the State.

Jaykay Enterprises Limited (“the Company”) has acquired 99% stake in Bangalore based partnership firm M/s. Silvergrey Engineers (SGE) inter-alia engaged in manufacturing and supply of parts and accessories to defence equipment manufacturing industry, catering to Customers including HAL, BEL, ISRO, Gas Turbine Research Establishment, Aeronautical Development Agency, Tata Advance Systems amongst others. SGE presently has manufacturing facilities located at Bengaluru

Representative image of 3D printers, digital manufacturing(not actual)

JK Digital & Advance Systems Private Limited

Incorporated on July 27, 2023, to provide digital and technical consultancy services, 3D scanning, and software engineering lab services. It aims to design, develop, and market software products for 3D applications and various industries.

Current Event

Company Share price has been adjusted for upcoming rights issue at 25Rs on 19th July24

Quarterly results have shown improvement –7th Aug24

12 acre Land parcel applied in lucknow

Details of recent triggers

Neumesh Labs Private Limited (Material Subsidiary) signs Memorandum of Understanding (“MoU”) with Agnikul Cosmos Private Limited Neumesh Labs Private Limited, material subsidiary of the company entered into a MoU with Agnikul Cosmos Private Limited, a Chennai headquartered Space-tech start-up Company on August 9, 2023. The MoU includes supply and maintenance of Metal Printer, Part Printing and Supply of Metal Powder. • Joint Venture with Phillips Machine Tools India Private Limited The Company had entered into a Joint Venture with Phillips Machine Tools India Private Limited, a subsidiary of Phillips Corporation, USA, to form and constitute a Limited Liability Partnership (LLP) under the name and style of JK Phillips LLP pursuant to the Limited Liability Partnership Agreement dated December 20, 2023. The LLP has been formed on December 28, 2023 to carry out the business of trading and distribution of Advance systems which includes CNC machines, lathes, hydraulic press, 3D printers, moulding machines and accessories originally produced by Phillips and other manufacturing/ trading activities including after-sales services. • Tripartite Agreement to manufacture Medical Implants executed between JK Digital & Advanced Systems Private Limited, EOS Electro Optical Systems India Private Limited and Meril Innovations Private Limited During the year, JK Digital & Advanced Systems Private Limited a WoS of the Company had completed the execution of a Tripartite Manufacturing Agreement on January 19, 2024 with Meril Innovations Private Limited, Gujarat (Meril Life Sciences), a leading MedTech Solutions Company, for production of Medical Devices/Implants through 3D Printing along with its technology Partner EOS, Chennai a WoS of EOS GmBH of Germany. The Agreement provides for JK Digital to Install, operate specified 3D Printers assisted by EOS, for manufacturing of Orthopedic Implants at Meril Life Sciences premises in Gujarat. • Merger of Business of Silvergrey Engineers into the Company In line with the approval of Board of Directors of the Company accorded on May 29, 2023 the Company had executed Dissolution cum Retirement Deed with Ujala Merchants and Traders Limited (UMTL) dated February 3, 2024, where in UMTL agreed to retire from the from the partnership of Silvergrey Engineers w.e.f. January 31, 2024, resulting the Company acquired the balance 1% stake in Silvergrey Engineers, pursuant to which the Company, will carry on the business of manufacturing of precision turned components and all type of engineering goods for the defence, aerospace and other allied industries as a division/segment of the Company. • Approval of Land Parcel to JK Defence & Aerospace Limited (WoS) in Bangalore Rural District JK Defence & Aerospace Limited WoS of the Company, had been accorded an approval from the Office of the Commissioner for the Industrial Development and Director of Industries and Commerce, Government of Karnataka on March 13, 2024 w.r.t. the investment proposal to establish a unit for manufacture of “Precision Turned Components and all types of Engineering Goods for the Defence, Aerospace and other Allied Industries including assembling in all kinds of products of Defence and Aerospace Equipments’’

The approval includes allotment of 5 acres of land from KIADB at Devanahalli General Industrial Area (ITIR), Bangalore Rural District and necessary permission for water and power connections and associated NOC(s) from state industry authority. The unit will be eligible for incentives and concession as per applicable policy of the State

Opportunity Size

Recently India has made 3D printed Semi cryogenic engine

Additive manufacturing expected to grow at more than 20% CAGR and coupled with defense and aerospace sector growth, oppportunity seems big enough

Technicals

Technical chart in 27 Jul24 (after Rights issue adjustment)

Technicals on 6-Jul-24 –ALD presentation

Technicals on 18-Jun-24

Risks

Operating Cash flows are not good. Working capital days, Cash conversion cycle, ROCE, ROE not upto the mark –outcome is high valuation which is typical characteristics for a turnaround company–Things look really bad before they turn decent, and then good and then turn very good.

Chances of turning very good?? We need to see –1 out of 100 companies turnaround succuessfully—rest of the companies bites the dust

Other income is high and skewing PAT

New business division of defense dont take off as anticipated

Dependency on limited customers for new contracts and

Competition from domestic and foreign players

There are related party loans to subsidiaries which may be susceptible to waivers

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Zaggle Prepaid Ocean Services

Key Investment thesis –> Differentiated SaaS-based fintech platform with Strong network effect offering Comprehensive suite of products for a large & growing addressable market. Company has amazing cross selling and Up-selling opportunities across domains.

Zaggle builds financial solutions and products to manage the business expenses of corporates, SMEs, & Startups through automated and innovative workflows. Headquartered at Hyderabad, it is at an intersection of of SaaS (Software as a service) and Fintech. With 273+ employees, the company has 50 Mn+ co-branded prepaid cards.

Products Zaggle Zoyer: accounts management services Zaggle Save: Help employees save tax with Save’s flexible employee benefit plans Zaggle Propel: all-in-one solution for employee rewards, and channel partner incentives.

Stats in accounts/users and Revenue streams

Share in Prepaid Cards market –16%+, Transaction volume wise ~13%

Strength of company

#1 issuer of prepaid cards

Multilingual interface

In-house developed technology with strong network effect

Customizable products

Diversified customer relationships across sectors along with preferred banking and merchant partnerships

Low churn rate of customer (<2%), long term relationships

Seasoned management team and board

Awards

Company has received an award for “Best Spend Management System“ and “Best Cards Initiative for Zaggle ZatiX“ at 11th Edition Payments Industry Awards by KamiKaze B2B.

Company has received an award for “FinTech Brand of the Year“ at 4th Edition Festival of FinTech Conclave Awards 2024 in association with BW Businessworld.

Company has received an award for “Pride of Telangana “ Achiever” Start up Category 2024” by Round Table India and Ratnadeep.

Company has received an award for “Excellence in Innovation Business Spend Management Software India 2023” in the Global Banking and Finance Review Awards 2023.

Fundamental Ratios, Cash, EBITDA, PAT

Amazing Sales and Profit growth of 11x in 5 Years

ROCE and ROE close to 15%

Debt to equity is under control and close to Nil

Pledging is 0%, Promoter has good skin in game at ~44% shareholding

Though FII, DII decreased stake in last 2 qtrs but still stake held by FII, DII + HNI is big, Public holding only ~20% stake . Big Shark Ashish Kacholia has increased stake over few quarters towards 4%+ shareholding

Triggers

Macro Trends :

Moving towards Digital payments ; Increasing scope of Prepaid cards ; New companies coming up

PREPAID CARDS Growth till 2027 expected to be in range of 30-40% CAGR

Management Guidance and commentary

We doubled our revenue over the last 3 years and are poised to double our revenue over the next 2 years through organic growth. Our expectation of revenue growth for this fiscal year is to the tune of 45%-55%. We are focused on garnering more market share and making significant investments in technology, specifically building deeper AI capabilities to cater to the massive demand for Spend management solutions. We intend to pursue inorganic growth opportunities through mergers and acquisitions. Additionally, we plan to expand geographically into the US markets as part of our growth strategy.

New Vertical

In Q1FY24, Zaggle introduced corporate credit cards and vendor management platform – Zoyer.

Launch of credit cards as a product in FY24 . The monthly volume of transactions for credit cards exceeded the monthly volume of transactions for prepaid card

Zaggle Zatix – our analytics platform launched this FY & offered by Banks as bundled solution of Corporate Credit Cards + SaaS.

New contracts in Last 1 year

In Q1FY24, company entered into contract with BOB Financial Solutions Limited for implementing commercial card Onboarding & value-added services platform and launch of the Zaggle Yes Bank Corporate Credit Card, powered by Zaggle Zatix – a spend analytics platform that allows corporates to streamline business and employee expenses, budget better and negotiate favorable supplier terms.

Zaggle Save (Expense Management platform & Employee benefits)

Employees of Hero Motocorp Limited.

Lifestyle International Private Limited

Quess corp limited

Bennett, Coleman & Co. Ltd.

ARCADIS CONSULTING INDIA PRIVATE LIMITED

Wipro Limited

Benetton India Pvt. Ltd.

Emcure Pharmaceuticals Limited

Europ Assistance India Pvt. Ltd.

Axis bank limited

Expleo Solutions Limited

Yokohama India Private Limited

Eversub India Private Limited (Subway)

Contract with Torrent gas for 2 years , approx 200cr business for Implementing Close Loop Fleet Program

Agreements with ecosystemplayers in varied domains like Domestic card, corporate cards, forex cards, Travel, Cross border payments

Agreement with VISA -In Oct,23, company has entered into a growth agreement with VISA. This alliance is in support of the issuance of Forex CoBrand Cards. Visa will pay the launch bonus for supporting the launch of Forex Cobrand Cards. and will also pay incentives on Forex transactions basis spend commitments. Zaggle can leverage existing Corporate base to sell forex cards to employees of the Corporate client, and it can be tightly coupled with Zaggle expense management solution. The deal size is ~$20 Mn for next 5 years.

Company has entered into an agreement with Skydo Technologies Private Limited. This is to enable facilatate cross border payments for Zaggle corporate customers

Zaggle is contracted to provide services to Bank whereby Zaggle’s accounts payable software & expense management software and the Axis bank Corporate Credit Cards are bundled and jointly offered to Zaggle corporate customers to drive card spends & greater usage of the software

Zaggle & EaseMyTrip will leverage its Existing Corporate base to sell Integrated Travel & Expense Management Solutions to Corporate Clients.

Zaggle & Riya Travel will leverage its Existing & New Corporate base to sell Integrated Travel & Expense Management Solutions to Corporate Clients.

Zaggle is contracted to be a Co-brand partner with Nishi Forex who is an Authorised Dealer II for forex card to carry out activities such as Sales and Distribution, Marketing and Campaigning bundled with Zaggle expense management to drive card spends & greater usage of the software. Subject to RBI approval the product launch will be done in due course.

Strategic alliances and partnerships with PSU

Opportunity Size

Zaggle Propel itself Can hit potentially 3000cr in revenue with overall revenue may hit 5000cr by 2030. Net profit margin may remain between 4-7%. Company may see profits of 250-350cr if opportunity size is grabbed. With an Eps of 19-25 and PE of 40-60 –Future Price Range oscillates between estimated 750-1500. Getting such a business at 100-150 Rs price point could be super deal (dont know if we get that price)

Peer analysis

Technicals on 6-Jul-24

Risks

Operating Cash flows are not good. That needs to be monitored closely

Working capital days, Cash conversion cycle is also expanding

Business is heavily titlted towards H2 of FY

Other income will go down once cash from IPO is Utilised

Lot of investment is being done in Zoyer for product enhancement and building of Zatix, an analytics platform. If products fails to takeoff, then a good amount will be written off from assets

Increased Regulatory Compliance poses many risks for Fintech companies

High valuations in short term is another risk though runway seems long for company growth