Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Oriental Rail Infra

Key Investment thesis –> Providing Infra to Railway sector. Govt focus and orders landing up fast to Railway vendors. Oriental rail Infra is prime contender for seats and birth for new coaches. Apart from that New wagons orders also flowing

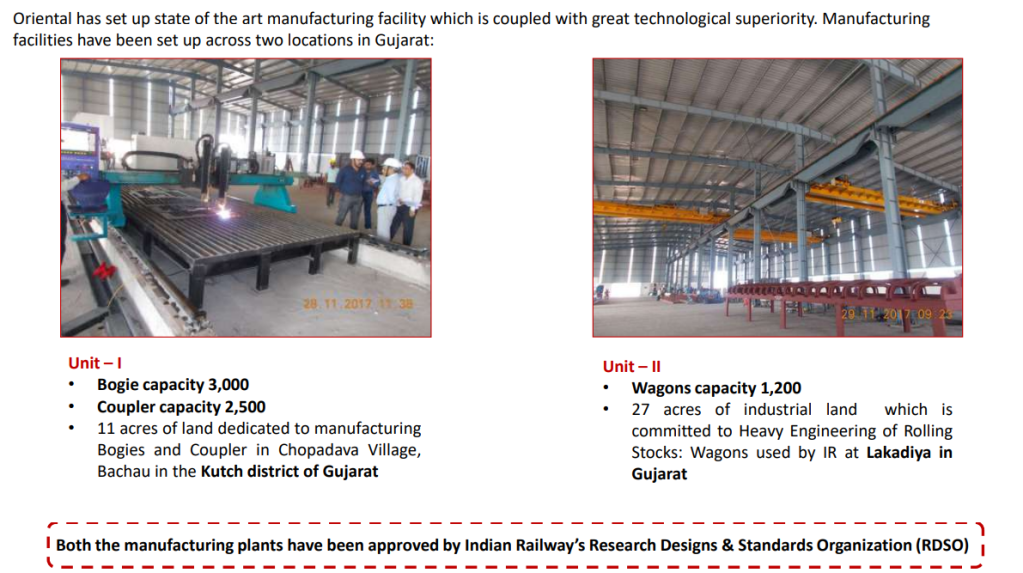

Oriental Rail Infrastructure Limited (ORIL) (formerly know as Oriental Veneer Products Limited) is engaged in manufacturing and supply of rail products predominantly for Indian Railways(IR). It manufactures Seats and Berths, Chairs, Lavatory doors etc. for all types of passenger coaches. It also manufactures Heavy Engineering equipment’s like Railway Rolling Stock, a diverse range of products which includes Wagons, Bogie, Coupler & Draft Gears through its wholly owned subsidiary Oriental Foundry Private Limited (OFPL).

Manufacturing Facility for Silicon Foam, Seats and Berth, Rexine, Compreg Board, PU Foam used for Seats & Berths, Recron used for Seats & Berths

Only Listed player in Seats & Berths in Organised sector

RDSO Certified and preferred vendor

1000+ employee strength

This Wagon capacity has been increased to 2400 wagons in Sep2023

Preferential shares allotment and warrants issued at 169 Rs (approx 200cr raised)

Order Book and strength

Company has a strong order book of more than 1200cr

Strong promoter background

3 decade old company

Big clients

Fundamental Ratios, Cash, EBITDA, PAT

Sales and profit 7x and 10x approximately in last 9 years

ROCE and ROE >12 %

Debt to equity is okayish at ~1, Pledging is 0%

Promoter has good skin in game at ~55% shareholding and big players entered recently including Mukul Agarwal

Triggers

Macro Trends :

Amid rising demand for coal freight and an aggressive push towards diversifying its freight basket, IR is planning to buy 1,00,000 more Wagons over the next three financial years Under the National Rail Plan(NRP), Centre wants to significantly increase the national transporter’s freight numbers, along with its modal freight share to 45 per cent by 2030. As per GOI estimates, consolidated demand for freight will be over 6,300 Million Tons (MT) by 2026 and 8,220 MT by 2031 Having ferried 1,418 MT in this fiscal, the national transporter would need to account for over 3,600 MT in 2031 to meet its NRP targets.

Company has worked on

Backward integration, Capacity Expansion, High Value Products and Client Diversification

Technicals

Technical chart in 10th Aug24

Risks

Working capital intensive nature of operations

Operating Cash flows are not good. Working capital days, Cash conversion cycle, ROCE, ROE needs to improve

Strong dependency on big customer IR

Margins are fluctuating in past based on execution and delivery. Not easy to predict bad or good quarters for company business

Susceptibility of profitability to volatility in raw material prices – ORIL’s product mix mainly includes seats, berths, compreg boards wherein the major raw materials are wood, rexene, cloth, foams, recron and various other solvents. Major raw material is supplied inhouse like company manufactures rexene and foam useful in manufacturing of seats. Other raw material consumed for manufacturing of seats includes veneer, which is formed from timber and company procures timber from local market. Its profitability is susceptible to fluctuations in the prices of wood as it serves as the main raw material for manufacturing of veneers, particle boards, plywood and compreg boards. For wagons, bogies and coupler body, major raw material is steel or scrap of steel which is procured from local market whose prices are highly volatile in nature. However, the company has a price variation clause inbuilt for key raw material, i.e., steel and wheels if procured from Indian Railways, thus reducing the price volatility to that extant

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Jaykay Enterprises

Key Investment thesis –> Defense and aerospace sector venture in precision manufacturing with big customerssupported by designing, development, manufacturing, and testing of advanced composite engineering products made or composed of fibre glass, glass mat, plastic, resins etc.with applications in defence/aerospace/ logistics & electrical industries. Company also developing good capabilities in Additive manufacturing and software systems to support above venture

Jaykay Enterprises Limited (JKE), part of J K Organisation and part of the 139 years old diversified JK conglomerate. JKE initially engaged in the business of manufacturing nylon and acrylic fibers and later went into Registrar and Share Transfer Agent activities.

Presently, the Company has diversified itself into Additive Manufacturing systems,Proto typing, powder metallurgy, large scale Digital manufacturing, Reverse Engineering, Plant modelling, In the area of defense & Aerospace we focus on areas of engineering products across various industry verticals, software designing and development, manufacturing of parts and accessories used in defence and aerospace sector, our work includes composite applications, Under water mines ,machining for aerospace sector.

Product segments

The Company has consolidated its business focus into specific dedicated opportunities. a) Defence & Aerospace; b) Digital Manufacturing & Advanced Systems c) Software &Services d) Real Estate & Hospitality. The Company is operating business of manufacturing of precision turned components and all type of engineering goods for the defence, aerospace and other allied industries including Manufacturing,trade and deal in all kinds of products related to Defence and Aerospace and Additive manufacturing and Technical Consultancy Services, 3D Scanning,Reverse engineering ,Plant Modelling, design, develop and market software products for 3D and activities through its subsidiaries, Joint Venture, partnerships and associates.

Management Pedigree

Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited and scion of one of the best-known business families of India. He is the cofounder & has served as Managing Director of JK Technosoft Ltd (‘JKT’) and leads the company’s global operations together with the Board &Management Team. He has invaluable experience within JK Organization companies, handling various aspects of J K businesses, managing business units and operations as well as spearheading successful national and international expansion programs. He has rich experience in the manufacturing & IT services industry and multi-dimensional expertise in basic & core sector industries such as – textiles, synthetic fibres, cement and chemical processing, both in continuous as well as discrete manufacturing, Mr. Singhania has deep insights in Software Development Life Cycle (SDLC), Project Management, Strategic Planning, Business Development, Thought Leadership. Mr. Singhania spearhead in Carving new business opportunities and managing strategic investments in Defence & Aerospace, Digital Manufacturing (3D & Processing), Digital Transformation through acquisitions. He is an alumnus of IMD Business School.

SWOT

Fundamental Ratios, Cash, EBITDA, PAT

Sales and profit catching up in last 2 years

ROCE and ROE <10 %

Debt to equity is under control 0.35, Pledging is 0%

Promoter has good skin in game at ~56% shareholding and stake is increasing while Public stake is decreasing

Triggers

Macro Trends :

INDUSTRY OUTLOOK Defense & Aerospace Sector outlook is very positive owing to huge requirements from the domestic market. The A&D market in India is estimated to reach around US$ 70 bilion by 2030. With a focus on indigenization by GOI the sourcing from within the country will increase many fold resulting in great opportunities for companies in this sector. The additive manufacturing market in India is increasing slowly but surely. The GOI has already come up with a policy. The early entrants will have an advantage over others. The application of this technology globally has entrenched Defense & Aerospace, Health care and oil & Gas Sector. Digital manufacturing will lead the global manufacturing sector in a decades time

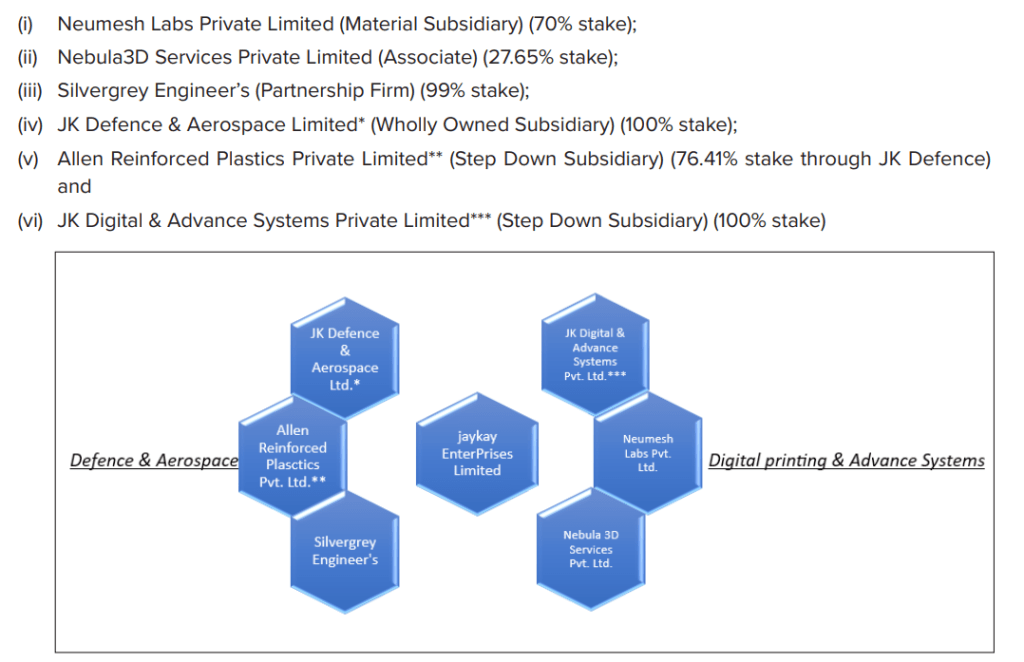

Joint Ventures And subsidiaries

JKE had entered into a strategic partnership with the global leaders in 3D Metal design and printing market. JKE had signed a Joint Venture and Shareholders Agreement with M/s Additive 3D Pte Ltd(A3D) an affiliate to M/s EOS Singapore Pte Ltd and consequent upon which a JointVenture (JV) company had been incorporated in the name of M/s Neumesh Labs Private Limited (‘Neumesh’) on 01st January, 2021, with shareholding of JKE and A3d respectively is 70% and 30% in said JV Company, inter alia, in the business of the 3D printing technology in India.

Neumesh Labs Private Limited

Neumesh Labs Private Limited (“Neumesh”) has established a Centre of Excellence (COE) in Bengaluru, the COE has state of the art EOS Software, Machines & Practices of cutting-edge 3D technology. Further Neumesh has developed a 3D printer JKPrint500, which was unveiled in IMTEX 23 Fair in Bengaluru. The product has received enthusiastic market response. Neumesh is also developing a lower price 3D printer which will be targeted at the mass market.

Neumesh, has also started its AM labs business. This is in line with various State Governments opening COE across engineering colleges and ITIs’. GOI in its 2023 budget announcement stated its intentions to establish COE’s across the country. Considering, huge numbers of COE’s that will be established, the demand for high quality polymer printers for training purposes will be high. Therefore, Jaykay Enterprises Limited along with its eco system partners have indigenously developed a polymer printer JK Print 300 and JKPM3 series, a Powder Management System which was unveiled in IMTEX 23 Fair in Bengaluru. The initial customer response has been encouraging. The JK Print 300 Printer is suitable for usage in prototyping, consumer goods, Automobile, and architecture for low volume production. The machine is ideal for usage in low volume production and training of students and technicians. The JK PM3 Powder Management System will optimize productivity and economics keeping in mind highest quality standards of parts produced by 3D metal printers. Neumesh, is working in tandem with the Governments Make in India program. Neumesh has started working on IAF prototyping projects and is looking closely at the MEA Oil & Gas market.

JK Defence & Aerospace Limited (“JK Defence”) and Allen Reinforced Plastics Private Limited (Allen)

JK Defence & Aerospace Limited (“JK Defence”) has acquired the 76.41% equity stake in Allen Reinforced Plastics Private Limited (Allen) which is engaged in the business of designing, development, manufacturing, and testing of advanced composite engineering products made or composed of fibre glass, glass mat, plastic, resins etc. applications in defence/aerospace/ logistics & electrical industries. Allen indigenously develops and supplies critical components to key defence projects in the country, such as BrahMos, Pinaka, SMILE, Akash missiles etc. to defence undertakings such as DRDO, ISRO, OFB, BHEL, BDL among others.

JK Defence stake in the step-down subsidiary i.e. Allen will increase from 76.41% to 92.92% after recent aquisition of shares through Rights issues

JK Defence & Aerospace Limited, Wholly Owned Subsidiary (“JKDAL”) of Jaykay Enterprises Limited, has been accorded an approval from the Office of the Commissioner for the Industrial Development and Director of Industries and Commerce, Government of Karnataka w.r.t. the investment proposal of JKDAL to establish a unit for manufacture of “Precision Turned Components and all types of Engineering Goods for the Defence, Aerospace and other Allied Industries including assembling in all kinds of products of Defence and Aerospace Equipments”. The approval includes allotment of 5 acres of land from KIADB at Devanahalli General Industrial Area (ITIR), Bangalore Rural District and necessary permission for water and power connections and associated NOC(s) from state industry authority. The unit will be eligible for incentives and concession as per applicable policy of the State.

Jaykay Enterprises Limited (“the Company”) has acquired 99% stake in Bangalore based partnership firm M/s. Silvergrey Engineers (SGE) inter-alia engaged in manufacturing and supply of parts and accessories to defence equipment manufacturing industry, catering to Customers including HAL, BEL, ISRO, Gas Turbine Research Establishment, Aeronautical Development Agency, Tata Advance Systems amongst others. SGE presently has manufacturing facilities located at Bengaluru

Representative image of 3D printers, digital manufacturing(not actual)

JK Digital & Advance Systems Private Limited

Incorporated on July 27, 2023, to provide digital and technical consultancy services, 3D scanning, and software engineering lab services. It aims to design, develop, and market software products for 3D applications and various industries.

Current Event

Company Share price has been adjusted for upcoming rights issue at 25Rs on 19th July24

Quarterly results have shown improvement –7th Aug24

12 acre Land parcel applied in lucknow

Details of recent triggers

Neumesh Labs Private Limited (Material Subsidiary) signs Memorandum of Understanding (“MoU”) with Agnikul Cosmos Private Limited Neumesh Labs Private Limited, material subsidiary of the company entered into a MoU with Agnikul Cosmos Private Limited, a Chennai headquartered Space-tech start-up Company on August 9, 2023. The MoU includes supply and maintenance of Metal Printer, Part Printing and Supply of Metal Powder. • Joint Venture with Phillips Machine Tools India Private Limited The Company had entered into a Joint Venture with Phillips Machine Tools India Private Limited, a subsidiary of Phillips Corporation, USA, to form and constitute a Limited Liability Partnership (LLP) under the name and style of JK Phillips LLP pursuant to the Limited Liability Partnership Agreement dated December 20, 2023. The LLP has been formed on December 28, 2023 to carry out the business of trading and distribution of Advance systems which includes CNC machines, lathes, hydraulic press, 3D printers, moulding machines and accessories originally produced by Phillips and other manufacturing/ trading activities including after-sales services. • Tripartite Agreement to manufacture Medical Implants executed between JK Digital & Advanced Systems Private Limited, EOS Electro Optical Systems India Private Limited and Meril Innovations Private Limited During the year, JK Digital & Advanced Systems Private Limited a WoS of the Company had completed the execution of a Tripartite Manufacturing Agreement on January 19, 2024 with Meril Innovations Private Limited, Gujarat (Meril Life Sciences), a leading MedTech Solutions Company, for production of Medical Devices/Implants through 3D Printing along with its technology Partner EOS, Chennai a WoS of EOS GmBH of Germany. The Agreement provides for JK Digital to Install, operate specified 3D Printers assisted by EOS, for manufacturing of Orthopedic Implants at Meril Life Sciences premises in Gujarat. • Merger of Business of Silvergrey Engineers into the Company In line with the approval of Board of Directors of the Company accorded on May 29, 2023 the Company had executed Dissolution cum Retirement Deed with Ujala Merchants and Traders Limited (UMTL) dated February 3, 2024, where in UMTL agreed to retire from the from the partnership of Silvergrey Engineers w.e.f. January 31, 2024, resulting the Company acquired the balance 1% stake in Silvergrey Engineers, pursuant to which the Company, will carry on the business of manufacturing of precision turned components and all type of engineering goods for the defence, aerospace and other allied industries as a division/segment of the Company. • Approval of Land Parcel to JK Defence & Aerospace Limited (WoS) in Bangalore Rural District JK Defence & Aerospace Limited WoS of the Company, had been accorded an approval from the Office of the Commissioner for the Industrial Development and Director of Industries and Commerce, Government of Karnataka on March 13, 2024 w.r.t. the investment proposal to establish a unit for manufacture of “Precision Turned Components and all types of Engineering Goods for the Defence, Aerospace and other Allied Industries including assembling in all kinds of products of Defence and Aerospace Equipments’’

The approval includes allotment of 5 acres of land from KIADB at Devanahalli General Industrial Area (ITIR), Bangalore Rural District and necessary permission for water and power connections and associated NOC(s) from state industry authority. The unit will be eligible for incentives and concession as per applicable policy of the State

Opportunity Size

Recently India has made 3D printed Semi cryogenic engine

Additive manufacturing expected to grow at more than 20% CAGR and coupled with defense and aerospace sector growth, oppportunity seems big enough

Technicals

Technical chart in 27 Jul24 (after Rights issue adjustment)

Technicals on 6-Jul-24 –ALD presentation

Technicals on 18-Jun-24

Risks

Operating Cash flows are not good. Working capital days, Cash conversion cycle, ROCE, ROE not upto the mark –outcome is high valuation which is typical characteristics for a turnaround company–Things look really bad before they turn decent, and then good and then turn very good.

Chances of turning very good?? We need to see –1 out of 100 companies turnaround succuessfully—rest of the companies bites the dust

Other income is high and skewing PAT

New business division of defense dont take off as anticipated

Dependency on limited customers for new contracts and

Competition from domestic and foreign players

There are related party loans to subsidiaries which may be susceptible to waivers

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.