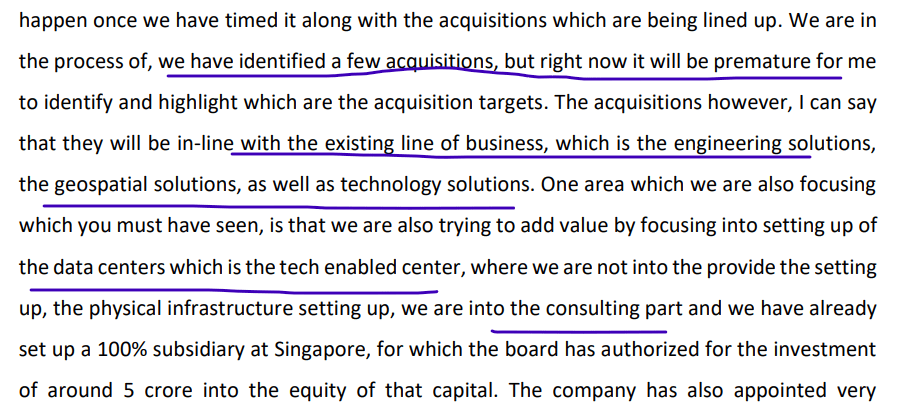

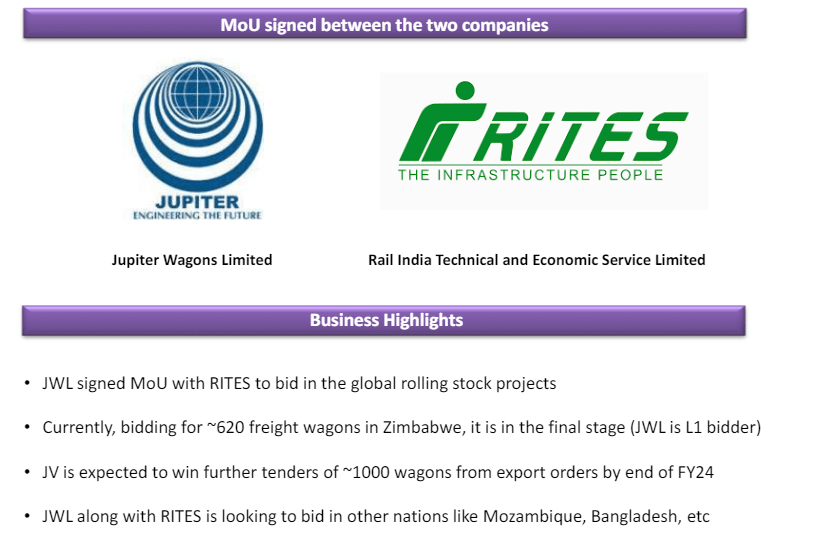

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Axiscades Technologies Limited

Key Investment thesis –> Company focus on Aerospace, Defense, Semiconductor, Electronic system verticals and gearing up for FY26, FY27

Business

AXISCADES is a leading, end to end technology and engineering solutions provider aiding creation of innovative, sustainable and safer products worldwide. AXISCADES is headquartered in Bangalore with subsidiaries in USA, UK, Canada, Germany, India and China; and offices in Germany, France, Denmark, USA and Canada. AXISCADES has a diverse team of over 3,100 professionals working across 20 locations across North America, Europe, UK and Asia-Pacific, striving to reduce the program risk and time to market.

The company offers Product Engineering Solutions across Embedded Software and Hardware, Digitization and Automation, Mechanical Engineering, System Integration, Test Solutions, Manufacturing Engineering, Technical Publications, and Aftermarket Solutions. The solutions comprehensive portfolio covers the complete product development lifecycle from concept evaluation to manufacturing support and certification for Fortune 500 Companies in the Aerospace, Defense, Heavy Engineering, Automotive, Energy and Semiconductor industries.

Company Portfolio

Current serving Major Industries

Aerospace

Heavy Engineering

Products engineering

Products and Solutions for Defense

AIP and Energy

Semiconductors

Awards

Received 3rd consecutive Diamond supplier award from Bombardier for 2022. This recognition is a testament to our unwavering commitment to excellence, innovation, and delivering with the highest standards of quality.

Opportunities :

Unique positioning with deep domain capabilities ranging across competencies, with respect to – Electronics Products, Engineering Services and Defence

Growth driven by leveraging Digital ER&D and Defence

ER&D Services – A large and underpenetrated market with a Global TAM of ~$1 Tn

Strong Defence-Tech Play with leadership in Radar, Sonar and Electronic Warfare systems

Revenue Breakup

FY24 revenue breakup

Q1Fy25 revenues breakup

Q2Fy25 revenues breakup

Fundamental Ratios, Cash, EBITDA, PAT, SHP

Stable OPM, Stable tax, Quarterly YOY growth in sales and PAT, Borrowing reducing

DE ~0.4 , Free cash flow is good , Pledge is Nil, ROCE < 15 and ROE<10%

Promoter has sufficient skin in game, Cash flows are good, Cash conversion cycle is elongated

Triggers

Macro Trends :

Recent Triggers in last 1 year or so

Appointment of Chairman Mr. Abidali

Appointed Mr. Abidali Neemuchwala as Chairman of the Board and Non-Executive Director at AXISCADES. With a distinguished career spanning over three decades in the technology industry, he has earned enviable reputation for his expertise in aligning organizations, driving business results, and consistently leading transformational initiatives.

Strategic partnerships and Opening Engineering design center

Signed a strategic partnership with with Cantier, a Singapore-based powerhouse in Manufacturing Execution Systems (MES), with a specialization in Industry 4.0 integration to create a synergy that promises to elevate precision, efficiency, and innovation in the manufacturing sector.

Inaugurated Engineering Design Centre in Saltney, UK to serve the long-term requirements of the Aerospace Industry and various promising opportunities in the region.

Signed a strategic partnership with KANZEN Institute Asia-Pacific Pvt Ltd (KIAP), for new age Industry IIoT, Digital Automation and MES 4.0 implementation for delivering enhanced value to our Global customers.

Mergers and Acquisitionsand QIP

Completed the acquisition of add solution GmbH which will strengthen our service offerings and bring opportunities to deliver enhanced value to our combined global client base. . This will provide us with a strategic foothold in the automotive space, with significant offshoring opportunities and access to marquee global automotive OEMs.

The board has also approved the acquisition of EPCOGEN., a niche service provider in Energy space, specializing in engineering design and solutions. This proposed acquisition will strengthen our presence in energy vertical, provide access to Middle East and North American Energy markets

QIP in Jan2024 at 657Rs/share — The Company successfully concluded the Equity Raise of INR 220 Crores in January 2024, with marquee Institutional Investors subscribing to the issue. This will strengthen the balance sheet and improve profitability, Reduction in Net Borrowings by 60% from INR 214 crores to INR 85 crores, which will significantly reduce Finance Cost

Deal Wins

Deal win with Aerospace OEM with TCV of $ 18 Mn in the areas of in-service repair and manufacturing support

Design and prototype wins in several defense programs, such as HISAR, next generation ERP for combat aircrafts, Intel based SBC, DEAL satellite terminal design, DF for Naval program, adding to the production order pipeline

Digital Team ramped to 75+ FTEs with deep competencies in automation, AI/ML and robotics, with complete digital project execution capabilities

Acquisition of add-solutions GmbH and EPCOGEN, opens new vistas in Automotive and Energy Space, adding strategic logos and competencies

Q4FY24 updates

Revenue from new customer logos grows to Rs.69 crores, a growth of 5 Times over the previous year

Deal win with Aerospace OEM with TCV of $ 18 Mn in the areas of in-service repair and manufacturing support

Defense Production Revenues in Mistral triples from Rs.39 crores to Rs.112 crores, with Rs.272 crores in executable production orders

Commencement of delayed delivery of Man Portable Counter Drone System (MPCDS) to the Indian Army, with significant addressable

market in Indian Defense and Global Markets

Design and prototype wins in several defense programs, such as HISAR, next generation ERP for combat aircrafts, Intel based SBC, DEAL satellite terminal design, DF for Naval program, adding to the production order pipeline

Digital Team ramped to 75+ FTEs with deep competencies in automation, AI/ML and robotics, with complete digital project execution capabilities

Advanced level discussions with leading helicopter manufacturer for engineering and design support

New opportunities in counter drone system over next 5 years are highly promising with addressable market more than INR 3,000 Cr. 40 Nos of one of a kind Man Portable Counter Drone System (MPCDS) cleared for dispatch to the Indian Army. Balance 60 Nos under production.

Onboarded world’s largest phone and consumer electronic manufacturer as a customer with clear glide path on engagements into FY25

Order book at 30th Ap24 — 749Cr

Q1FY25 updates

Mistral Solutions received order of ₹90 crores from BEL for supplying Radar Processing Systems

Ramp up in aerospace with European OEM focused on production and plant migration efforts

Ramp up in high end cybersecurity solutioning with UK automotive manufacturer.

Onboarded an EPC major from Middle East as our customer with long term contract

Completed second tranche of delivery of Man Portable Counter Drone System (MPCDS) to the Indian Army

Expenses hit in past Q3/Q4 Fy24

Increase in finance cost due to debt funding for Mistral acquisition . In Q2 FY24, the material cost has increased due to increase in production orders in Mistral and increase in employee expenses on account of annual increments and investments in building competencies in Embedded and Digital for future growth

Q2FY25 Update

Defence revenues grew by a healthy 73% QoQ, with Defence production revenues surging by 84% QoQ, bolstered by a significant order backlog set for execution in fiscal years 2025 & 2026. With a healthy pipeline and focused approach, over the next 12-18 months, we aim the defence revenue to reach around 60% of the overall company’s revenue

Management commentary With latest focus areas

Unmanned combat, we are having anti-drone, drones, and drone controllers

Foreign OEMs, we have a three-pronged, that is, weapon package, submarine, and avionics. preferred offset partner for the weapon system, weapon package

new programs, all our missile programs, one is the largest missile program in India, another is an upgrade of the existing missile program, another is ground system for key programs

Product focus : particular product direct RF. Then there is, of course, our product X-band radar, which is primarily used in the submarine and marine systems.

Airbus, we have major programs running in India. C295, MRTT, Multi Role Transportation Tanker, which is going to be 330 based, And AVEX, of course, 319 based.

Tying with AgniKul, having an MOU with them, and approaching the ISRO, ISRO and other space agencies for two major things, NGLV, New Generation Launch Vehicle, and Bharatiya Space Station. So we want to add value to them significantly, and there could be opportunities in 3D additive manufacturing, and designing of certain subsystem blocks, etcetera. Then there is also chances for electronics-based algorithms and advanced systems, and for the guidance and navigation, that product we’ll be able to make. The third one is AI-based anomaly detection in the launching

Capturing some discussions from Dec24 confcall

C2P strategy, that is, chip to product. That is Mistral’s non-defense activity, or our group’s non-defense activity., we are shifting the center of gravity of C2P to US. Basically it will be driven out of US. We’ll have a small team there and driving the offshore team here. That’s the strategy

We are a very, very good RF in RF. We consider we are among the best in India for RF. RF and RF activities. Second is probably we are one of the best in handling mixed signals. We can handle analog, digital, RF, everything together. That is one of our forte. Third is sensor fusion. We can handle multiple sensor. Sensor fusion comes very, very handy when you deal with multiple sensor in a new AI environment, in new robotics or auto-driven and those kinds of things. We are extremely good in both. Then we are very good in ruggedization. We are especially because we are very defense focused. We can ruggedize any product and do that. And finally that we are very good in the chip, chip level, post-silicon, whatever it is, validation, verification, and take the chip to the product and then product to the customers

Continuous Hiring of Talent

Orders winning, Expansion in Middle east and Outlook for different segments by Management

Added this latest development on 17Jun25

INDRA SIGNS AGREEMENT WITH AXISCADES TO BOOST PRODUCTION OF CUTTING-EDGE SYSTEMS IN INDIA

Indra, a European-based global leader in defense, aerospace, and strategic systems, and AXISCADES a prominent technology solutions provider in defense, aerospace and strategic electronics, are proud to announce a strategic alliance.

Indra is keen to acquire defense-related products and services from AXISCADES, which will be delivered through AXISCADES’ comprehensive design, development, production, and supply chain center.

Both companies are actively exploring joint product development for the Indian and global markets, potentially adapting existing Indra products or creating new ones specifically tailored to meet customer needs.

TechnicalChart

Technical chart on 15-dec24

Technical chart on 29-dec24

Risks

Highly competitive industry

Acquisitions dont play out as anticipated

Customer concentration risk – On a consolidated basis, ~26% of ACTL’s revenues in FY23 were from its top two clients (35% in FY22).

Slowdown in Europe impacting automotive revenues

Heavy Engineering vertical remains a drag for few more qtrs although optimization work going on

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Impact Of Data Localisation Laws The Indian government’s push for data localisation, under policies like the Digital Personal Data Protection Act, has accelerated the establishment of data centres. Global players such as AWS, Microsoft, and Google are investing heavily to comply with these regulations, while Indian companies like Jio and Yotta Infrastructure are scaling up their capacities.

Green Data Centres On The Rise Sustainability is a key focus for Indian data centres in 2025. Operators are investing in renewable energy sources like solar and wind to power facilities, with states such as Rajasthan and Gujarat leading in renewable energy adoption. Innovative cooling technologies, including liquid cooling and the use of natural resources for temperature management, are becoming standard practices to enhance energy efficiency.

Edge Computing And Regional Growth India’s shift towards edge computing is transforming data centre architecture. With the rollout of 5G and the proliferation of IoT devices, smaller edge data centres are being established closer to users in Tier 2 and Tier 3 cities.

Expansion Of Colocation And Hyperscale Facilities By 2025, colocation and hyperscale data centres will dominate the Indian market. Colocation facilities, which allow multiple organizations to share infrastructure, are becoming the preferred choice for startups and small businesses due to cost efficiency. On the other hand, hyperscale data centres, built to support massive data volumes for global giants like Amazon and Google, are rapidly expanding to cater to India’s growing digital needs.

Advances In Security And Automation With increasing cyber threats, Indian data centres are integrating advanced security measures such as Zero Trust Architecture, AI-powered threat detection, and biometric access controls. Automation is playing a vital role in optimizing operations. AI systems are managing energy consumption, predicting maintenance needs, and ensuring seamless uptime, reducing operational costs while improving efficiency.

Government Support And Policy Initiatives The Indian government’s initiatives, such as the National Policy on Software Products and state-level incentives, are creating a favourable ecosystem for data centre growth. Many states are offering subsidies on land, power tariffs, and taxes to attract data centre investments.

Opportunities In Tier 2 And Tier 3 Cities As data consumption grows beyond urban centres, data centre operators are expanding into Tier 2 and Tier 3 cities. These locations offer lower operational costs, ample land availability, and growing demand for digital services, making them attractive for future investments.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Jash Engineering

Key Investment thesis –> Increasing Demand of Water Intake Systems, Water and Waste Water Pumping Stations and Treatment Plants, Storm Water Pumping Stations, Water Transmission Lines, Consistent Business and Order book

Jash engineering is dedicated to offering varied products for use in Water and Wastewater Pumping Stations and Treatment Plants, Storm Water Pumping Stations, Water Transmission Lines, Desalination, Power, Steel, Cement, Paper & Pulp, Petrochemicals, Chemicals, Fertilizers and other process plants. Headquartered in Indore – India, Jash has six well-integrated state-of-art manufacturing facilities, four in India and one each in the USA & UK. Global presence with bases in India / USA / Austria / Hong Kong / UK

Employees > 1075, Countries served 45+, Manufacturing units 6, Capacity utilization 70% approx

Company has many accolades, and technical collaborations

Joint Venture with Invent , Germany to manufacture their range of aeration and mixing equipment.

Technical & Financial collaboration with Schuette, Germany for Bulk solids valves

Technical Collaboration with Invent, Germany for Disc Filter

Technical collaboration with Rehart, Germany for Archimedes screw pumps & hydro power generation.

Technical collaboration with Weco Armaturen, Germany to offer its range of Valves in Asian market

Business Segments and Revenue Contribution and Products

Domestic 40%, Exports 60%

Water control gates –60% (FY24) 49%(Q1Fy25)

Valves -15% FY24, 13% Q1FY25

Screening equipment 15% FY24, 31% Q1FY25

Hydropower and pumping solutions 10% FY24, 7% Q1FY25

Clientele

Strengths :

Long standing relationships with domestic marquee customers.

Efficient business model

Strong project execution capabilities

Diversified geographical presence in India and world

Strong Technical Qualification to bid for new projects

Highly experienced Management Team

Fundamental Ratios, Cash, EBITDA, PAT

ROCE>25% and ROE> 22%, DE ~0.23 , Free cash flow is good , Pledge is Nil

Net Profit went 67X+ in 10 Years, Consistent Dividend Payout

Consistent Profit growth, sales growth, ROE over 3 years, 5 years, 10 Years

Triggers

Expanding presence and Acquisitions

Acquired Waterfront Fluid Controls Ltd, UK in 2023.

WATERFRONT UK PLANT & OFFICE INAUGURATION After successful acquisition of Waterfront Fluid Controls Ltd, UK, the company has taken manufacturing plant on lease which is adjoining shed to the present Waterfront’s shed. This plant was commissioned on 31st May 2024.

A new plant for manufacturing process equipment is under construction in Chennai. This plant will be commissioned in December 2024/Feb25. This facility is being built at an approximate cost of Rs. 20 crores and this will start contributing to improvement in revenue from April 2025 onwards. This facility at its peak production capacity will contribute up-to Rs. 100 Cr to company revenue.

A new land has been acquired for expansion of Unit 4 (Fabricated Products Plant), SEZ Unit. This new plant of ~ 55000 sq. ft. will be commissioned in FY 2025-26. Manufacture Stainless steel products for the growing export market. The construction of this plant will start in October 2024 and the plant will be commissioned by year end 2025. This plant will be constructed at a tentative cost of Rs 22-23 crores inclusive of land and at its peak production capacity will contribute up-to Rs. 100 Cr to company revenue.

Good execution and order book and Consistent new orders

946 cr order book on 1st sep24, 74cr orders in pipeline, negotiation

FY25 guidance ~675cr

New Product developments

First Vortex Grit Mechanism with Grit Classifier For 26 MLD STP Jhansi, UP Jal Nigam

Combined Screening & Grit Removal System-1MLD (PTU) for Enviro-Infra, Bareilly, UP

First set of Bladder Vessel 9 m3 x 3, 1 m3 x 3 supplied to Varanasi WSP Project

3 Wheel Sealed Version Disc Filter for 6 MLD capacity for Delhi Jal Board

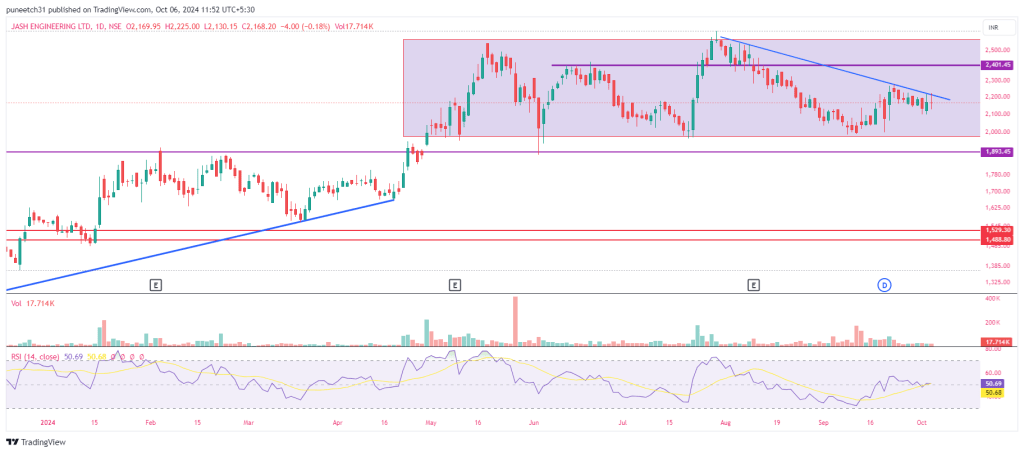

Technical chart on 6 Oct 24

Risks

Large working capital requirement, cash conversion cycle is bit high Trade receivables and Inventory on higher side Rising raw material and commodity costs Increase in competitive bids for procuring the projects

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Likhitha Infra Limited (LIL)

Key Investment thesis –> Increasing Demand of Gas pipeline Infra, City Gas distribution and National Gas policy 2030, Expanding Geographically, Consistent Business and Order book

LIL was incorporated in 1998 and is engaged in the business of pipeline laying providing comprehensive erection, testing, and commissioning of Oil and Gas pipelines, city gas distribution projects, tankage and operations and maintenance services. It is based in Hyderabad, Telangana.

Company has two (02) Joint Ventures viz., CPM-Likhitha Consortium, India and Likhitha Hak Arabia Contracting Company, Kingdom of Saudi Arabia. In addition, Company held 60% equity share capital in Likhitha Hak Arabia Contracting Company, and consequently, now it became a subsidiary of the Company

Has successfully laid over 1500 km of steel pipelines and over 1500 km of MDPE of oil & gas pipelines in the past years. Additionally, the company is laying approximately 1000 km of oil & gas pipelines for the ongoing projects Executed the First Trans-National cross-country pipeline of South-East Asia connecting India to Nepal in the year 2019, for the supply of petroleum products

Strong presence in more than 20 states and 2 Union Territories in India.

Business Segments:

a) City Gas Distribution Projects: This Involves laying of steel and MDPE pipelines for consumers across domestic, commercial and industrial sector, creating a network of pipelines along with associated facilities, Last Mile Connections, CNG Stations b) Cross Country Pipeline Projects: Laying of Cross Country Pipeline projects along with piping, civil, electrical, instrumentation and other associated works c) Operation & Maintenance Services: O&M services include providing skilled manpower, executing emergency repairs, overhauling, scheduled maintenance activities and operation of the network d) Tankage: Construction of fuel depots including storage tanks, Combined Station Works, mechanical, instrumentation, electrical, civil works, F&G system, and other associated facilities

Strengths :

Long standing relationships with domestic marquee customers.

Efficient business model

Strong project execution capabilities

Diversified geographical presence in India

Strong Technical Qualification to bid for new projects

Strong promoter holding showing skin in game

Strong Order Book 1500cr in Jun24

Highly experienced Management Team

Credit ratings –>Long term facilities A/Stable and Short term facilities A1

ROCE>30% and ROE> 20%, DE ~Nil , Free cash flow is good , Pledge is Nil

Stable OPM, Net Profit went 33X+ in 10 Years, Consistent Dividend Payout

Consistent Profit growth, sales growth, ROE over 3 years, 5 years, 10 Years

Promoter has sufficient skin in game at 70% shareholding

YouTube link

Triggers

Macro Trends :

India has set a target of increasing the share of natural gas in the overall energy mix to 15% from present 6.7%.

As per the Government policies, PNGRB has increased the number of Geographical Areas (GAs) to 228 comprising of 402 districts spread over 27 States and Union Territories, covering 70% of Indian population and 53% of its area. These recent Government initiatives have provided lucrative opportunities for Oil & Gas infrastructure service providers

Recent policy moves, including a wide-scale rollout of CNG and the expansion of gas infrastructure including LNG terminals, long-distance transmission pipelines and city gas distribution networks, will help drive 30bnm³ of gas demand growth over the next decade through fuel switching away from coal and oil. A recent switch to CNG from coal in India’s brick industry is encouraging greater gas use.

India is set to dominate the number of trunk/ transmission pipeline projects that are expected to start operations in Asia during 2024-2028, contributing about 43% (62 projects) of the region’s total projects count by 2028. The transmission pipeline length of 29,800 kms is expected to be added, says GlobalData, a leading data and analytics company.

The gas pipeline infrastructure has been seeing intense development activity. The Government of India has set a target to reach 34,500 km by 2024-25 end from 22, 335 km as on January, 2023. Furthermore, plans to connect states with the trunk natural gas pipeline network by 2027 are gathering momentum.

In terms of investments, the Petroleum and Natural Gas Ministry said about ` 41,000 crore ($4.95 billion) are expected from companies to build natural gas pipeline infrastructure in the northeastern states and northern federal territories of Kashmir and Ladakh. The thrust on natural gas and government policy initiatives are in line with India’s global commitments to boost the use of cleaner fuels and cut carbon emissions with the ultimate goal of achieving net zero carbon emissions by 2070.

Expanding presence

In line with growth strategy, Company has entered new markets such as the Kingdom of Saudi Arabia and the United Arab Emirates, where we see substantial opportunities in the oil and gas infrastructure sector. The company has been exploring growth opportunities beyond India. We have formed a joint venture firm in Saudi Arabia and have opened a branch office in Abu Dhabi, UAE to explore business prospects in the Middle East markets which promise long-term growth for pipeline infrastructure development.

The Indian government’s continued emphasis on expanding the oil and gas transportation network and promoting city gas distribution projects provides us with a steady stream of contracts.

India’s energy consumption is on the rise, with the country consuming 19.9 million metric tonnes of petroleum products and 5.51 BCM of natural gas during FY 2023-24. As the world’s third-largest consumer of energy, India’s demand for natural gas is expected to grow fivefold by 2047, in line with the nation’s vision of becoming a developed nation by its centennial year

Good execution and order book and Consistent new orders

Technical chart on 21st Sep24

Risks

Large working capital requirement, cash conversion cycle is bit high Trade receivables and Inventory on higher side Any change in CGD policy Rising raw material and commodity costs The Company is deriving significant portion of orders from major Oil & Gas distribution companies inducing a client concentration risk Increase in competitive bids for procuring the projects

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

A dark store is a small warehousing urban distribution centre exclusively for online shopping with an area ranging between 3,000 to 8,000 sq ft located close to densely packed residential areas to meet quick delivery requirements, Srinivas N, Managing Director, Industrial and Logistics, Savills India said.

Dark stores stock a variety of products and operate around the clock. This enables quick access to inventory, reduces transportation costs, has a quick turn-around time, and improves last-mile delivery capabilities.

However, unlike warehousing, dark stores maintain a limited inventory, often with products having a shelf life of less than 24 hours. In contrast, warehouses store a wide variety of materials in bulk quantities, without the same time constraints on product freshness or expiration.

“The current requirements from quick commerce necessitate dark store spaces of 5,000 square feet or larger. The evolution of quick commerce has managed to establish a firm foothold in the market, which indicates a likely increase in the number of these larger stores moving forward,” Abhishek Bhutani, Managing Director, Ahmedabad and Logistics & Industrials, Cushman & Wakefield said.

Where are dark stores usually located?

A 2021 study by JLL showed that in the e-commerce sector, about 10-15 percent of total kilometres travelled in urban areas contributed to 47 percent of total transportation costs.

This brought dark stores closer to the dense residential areas to ensure efficient and timely delivery. However, real estate costs in urban locations cannot meet retail rental expectations. Therefore, dark stores are usually located in smaller commercial building basements, parking spaces, and defunct facilities in the bylanes or alleyways.

Additionally, these stores are not visited by customers. So, low-cost space is most functional for a dark store.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Aeroflex Industries

Key Investment thesis –> Increasing Demand of HVAC system, Large Scale Industrialization, Modernization in Agriculture and Demand from new edge industries like Aerospace, Satellite, Solar and Robotics

Company is one of the leading Indian manufacturers of metallic flexible flow solutions made with stainless steel used for controlled flow of all forms of substances including Solid, Liquid, and Gas. Incorporated in 1993, co. is part of Sat Industries Limited.

Product Profile: Braided hoses, unbraided hoses, solar hoses, gas hoses, vacuum hoses, braiding, interlock hoses, hose assemblies, lancing hose assemblies, jacketed hose assemblies, exhaust connectors, exhaust gas recirculation (EGR) tubes, expansion bellows, compensators, and related end fittings.

Exports to 89 countries across Asia, Americas, Europe and Africa, through a diversified go-tomarket model

Scalable and Customized flexible flow solution products

Current serving Major Industries

Steel & Metal

Oil & Gas

Chemicals

Sea Port Terminal Handling

Paper & Pulp

Pharmaceutical

Strengths :

Extensive Promoter experience

Employee strength -500+

The company has 2500+ SKUs

Strategically Located Near JNPT Port

80+ machine lines

72+ Products across various stages of Research and Development

14 Qualified R&D Team

NABL Accredited Lab

ISO 9001:2015, ISO 45001:2018 and ISO 14001:2015 certified;

Adherence to global standards

Revenue Breakup

Fundamental Ratios, Cash, EBITDA, PAT

ROCE asnd ROE> 20%, DE ~Nil , Free cash flow is good , Pledge is Nil

Stable OPM, Net Profit went 8X+

Promoter has skin in game + Big Shark Ashish Kacholia holding 3.6%

Triggers

Macro Trends :

▪ Global market for SS flexible hose has grown at a CAGR of 8.2% to value at approximately USD 3.3 Bn in 2022 ▪ Traditionally, the demand for Flexible Flow Solutions made with Stainless Steel Corrugation was largely driven by the industrial sector – manufacturing plants and manufacturing products from chemicals to paper ▪ Between FY’18-9M FY23, over 1,840 projects (brownfield and greenfield) were completed in the manufacturing ▪ With Flexible Flow Solutions made with Stainless Steel Corrugation application being universal, this large base is believed to have supported a strong demand for the product ▪ Given the increasing preference for Flexible Flow Solutions made with Stainless Steel Corrugation in place of rubber / PTFE / polymer hoses, the demand for the former from the industrial sector would be stable

Company has worked on Capacity Expansion, value added products

Expanding our presence to:

Electric Mobility

Fire Sprinklers

Solar

Robotics

Semiconductors

Aerospace and Satellite

Management commentary in Q1Fy25 results

Increasing margins possibilities, Increasing orders from assemblies, Focus on value added offerings, possible inorganic Way of expansion, Acquisition

Technicals

Technical chart on 8th Sep24

Risks

PE is bit high in short term

Large working capital requirement, cash conversion cycle is bit high

Exposure to volatile raw material price

Acquisitions dont play as anticipated

Demand dont originate as anticipated

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Servotech Power

Key Investment thesis –> Developing EV charging Infra and Delivering Solar Rooftop solutions across India. Key Business wins for EV charging Infra, Association with key businesses B2B

SPSL is in the business of high-end solar products and EV chargers. It develops ultra -fast DC chargers and Home AC chargers, and has installed over 2400 EV chargers in collaboration with oil marketing companies

Product Profile: a) EV Charger: Electric Vehicle Charging Station, AC Charger, DC Charger b) Solar Products: Solar Inverter, Solar Panels, Solar Batteries, ServPort, SMU c) Power & Backup: Battery, Servo Stabilizer, etc. d) LEDs: Domestic LED, Commercial LED e) Oxygen Concentrator: Oxygen Concentrator 5L and Oxygen Concentrator 10L f) UVC: UV-C Handheld Disinfection Lamp – 6W, Portable UV-C Disinfection Lamp – 36W (Sensor Equipped), Portable UV-C Disinfection Lamp – 38W, UV-C Disinfection RoboTruk – 150W, UV-C Sterilization Bag, UV-C LED Sterilization Box with 10W Wifi Charger, UV Sterilization Box with Charger, UV-C Car Intelligent Sanitizer, Car Air Sanitizer, UV Air Purifier, FAR UV-C Digital Sanitizer

Covered the thesis here in quick 12 min Video

Well-equipped 2 manufacturing facilities spanning over 80,000 sq. ft. and 1,44,000 sq. ft. respectively in Sonipat, Haryana

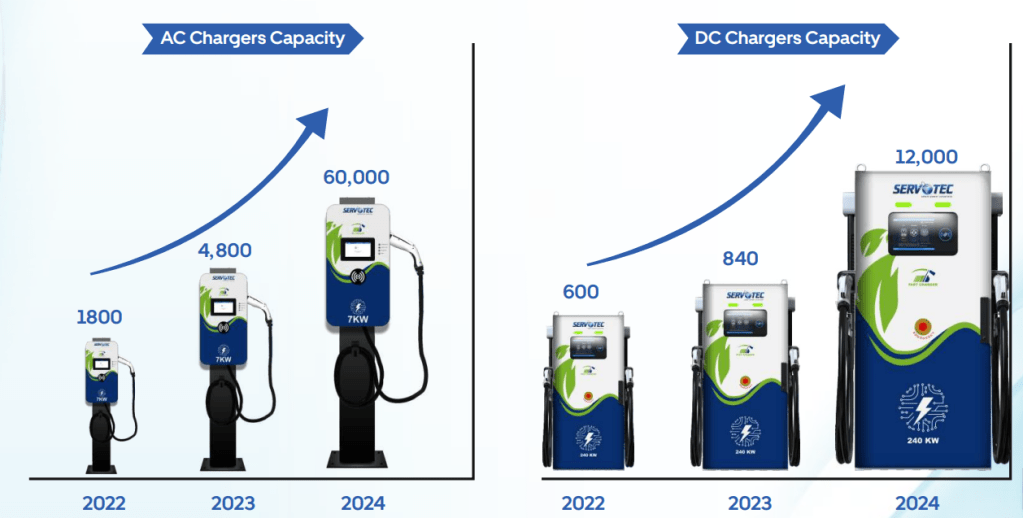

Capacity to manufacture 30,000 AC EV Chargers and 12,000 DC EV chargers annually

The company is majorly into B2B operations and having Marquee clientele comprising of BPCL, IOCL, HPCL, Nayara Energy, UPNEDA and others

Employee strength -500+

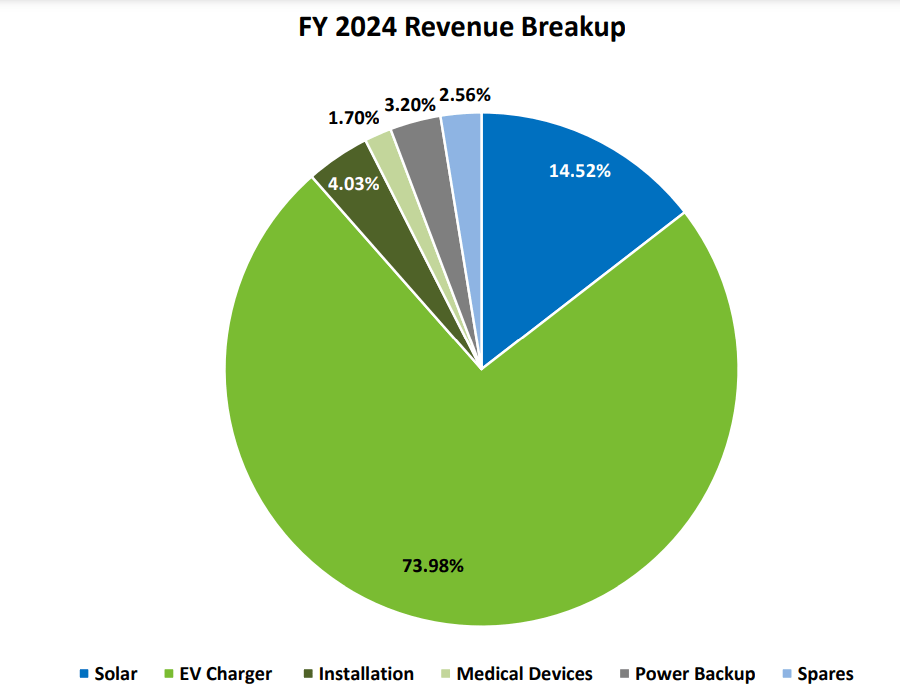

Revenue Breakup

Range of EV AC AND DC chargers

DC chargers have amazing features on fast port, advanced connectivity and user friendliness

Range of Solar solutions

Solar panels, Solar Inverters, Solar Batteries

ESS : Energy storage system (Major tailwinds may appear here)

Solar Street light (too much commodity)

Solar charge controller

EV CHARGER Components

Another interesting solution is Servport

Fundamental Ratios, Cash, EBITDA, PAT

ROCE and ROE > 10%, Pledging 0%, Debt to equity under control

High TTM PE and PB ratio

12X Sales and 12X PAT in 10 Years, Stable EBITDA numbers, Improving NPM

Promoter has good skin in game at ~60% shareholding, FII holding 5% approx

Cash conversion cycle have improved in recent years

Triggers

Macro Trends :

Developing EV charging Infra and Solar Rooftop solutions Infra across India

Journey and recent forays

Government subsidies & policies promoting local manufacturing of EV Components and sustainable energy resources

Growing need for carbon neutral has increased the demand forsustainable energy solution

Increasing demand for EV charging stations with healthy traction in order pipeline in addition to a sizable order backlog. Govt. allocate subsidies of INR 800 Cr to set up 22,000 fast chargers at various fuel pumps across India. The government has sanctioned 2,877 such charging stations across 68 cities in 25 states and UTs. In addition, 1,576 charging stations on nine expressways and 16 highways have also been sanctioned.

Projections indicate that fast-charging stations will witness a CAGR of over 40% by 2025.

New additions in budget 2024 like Pumped Storage Policy and exemption of customs duty on lithium will incentivize renewable energy integration and adoption

Rising urbanization and awareness of climate change have led to increase in demand for cost-efficient products

PM Suryodaya Yojana to solarize 1 Cr Households. 50 solar parks with an aggregate capacity of 37.49 GW have been approved in India

Company has worked on Capacity Expansion

Preferential shares allotment and warrants issued at 83 Rs (approx raised 74cr)

Backward integration efforts for key components (control set and power module) are on track, with the control set already being manufactured in India.

Solar Segment:

Regular monthly sales of ₹8-10 crores in the solar segment, targeting a total of ₹100-150 crores annually.

Plans to expand presence in 20-21 states within two months to leverage government schemes for household electricity.

International Expansion:

Export business is expected to grow, with previous year’s revenue at approximately ₹40 crores and positive momentum for future exports.

Attending international exhibitions and establishing a dedicated export team.

Patents; Innovation and Leadership

51% Growth in the Dealer & Distributor Network

Hired 128+ employees in Q1

Coninuous order wins from Major OEM’s —Current order book stands at approximately 8,000-8,500 pieces of DC chargers, indicating strong demand.

Order win from BPCL worth ₹120 Crs for the supply of 1,800 DC EV chargers

Order win from IOCL and other EV Charger OEM’s worth ₹111 Crs for the supply of 1,400 DC EV chargers

Order win from BPCL for the supply of 2,649 AC EV chargers

Order win from HPCL and other EV charger OEM’s worth ₹102 Crs for the supply of 1,500 DC EV chargers

Signed a contract with Adani Total Energies E-Mobility Ltd. (ATEL) for the supply of AC EV chargers

SPSL will be responsible for manufacturing, supplying and Installing AC EV Chargers at different Airports and other said locations

Collaborated with an international company to enhance its in-house components manufacturing.

SPSL will be constructing a cutting-edge manufacturing facility focused on the production of Power Modules, Control Circuits, and PLCs. The new plant will have an initial annual production capacity of 24,000 power modules & will ramp up its production capacity to 2.4 lakh power modules annually

Solar energy storage

Servotech Secures Order of around 1.2 MW Solar Energy Storage and Grid Connected Systems from Rural Development Department and UPNEDA. Servotech will be responsible for installing multiple 75kW solar-based energy storage systems, designed to provide reliable and uninterrupted power supply across Uttar Pradesh. Additionally, the company will also be designing, manufacturing, supplying, erecting, testing and commissioning 20 kW and 40 kW grid-connected solar power systems, contributing to the state’s renewable energy goals. This order will prove to be essential for overcoming geographical and infrastructural challenges in areas of Uttar Pradesh by enabling a broader reach of sustainable energy solutions and ensuring the penetration of renewable energy into the grid.

Creating new subsidiary “Servotech Sports and Entertainment Pvt. Ltd.”

Servotech aims to capitalize on the sporting fervor, its immense popularity, and global appeal to strengthen its brand presence and connect with a wider audience base. This strategic alignment presents an exciting opportunity for Servotech to extend its reach beyond its industry boundaries and tap into new avenues of success and engagement, establishing itself as not just a leader in the EV charging and solar energy sectors, but also as a prominent player in the sports industry.

Technicals

Technical chart on 21st Aug24

Risks

Consistent Equity dilution, consistent increase in borrowing and Negative cash flows poses risk to company business growth

PE is high and any 2 bad qtrs can screw the returns profile from the current levels

Large capital working requirements is another thing to watch out for

Highly competitive industry both in Solar and EV industry

Delay in projects due to Govt policies or Land acquisition issues

Components import is another risk

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

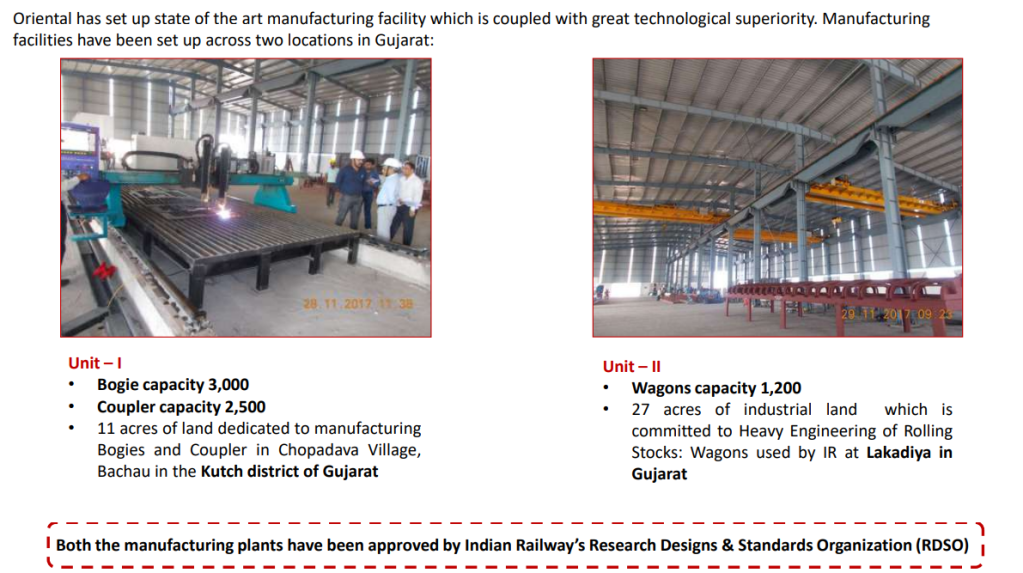

Oriental Rail Infra

Key Investment thesis –> Providing Infra to Railway sector. Govt focus and orders landing up fast to Railway vendors. Oriental rail Infra is prime contender for seats and birth for new coaches. Apart from that New wagons orders also flowing

Oriental Rail Infrastructure Limited (ORIL) (formerly know as Oriental Veneer Products Limited) is engaged in manufacturing and supply of rail products predominantly for Indian Railways(IR). It manufactures Seats and Berths, Chairs, Lavatory doors etc. for all types of passenger coaches. It also manufactures Heavy Engineering equipment’s like Railway Rolling Stock, a diverse range of products which includes Wagons, Bogie, Coupler & Draft Gears through its wholly owned subsidiary Oriental Foundry Private Limited (OFPL).

Manufacturing Facility for Silicon Foam, Seats and Berth, Rexine, Compreg Board, PU Foam used for Seats & Berths, Recron used for Seats & Berths

Only Listed player in Seats & Berths in Organised sector

RDSO Certified and preferred vendor

1000+ employee strength

This Wagon capacity has been increased to 2400 wagons in Sep2023

Preferential shares allotment and warrants issued at 169 Rs (approx 200cr raised)

Order Book and strength

Company has a strong order book of more than 1200cr

Strong promoter background

3 decade old company

Big clients

Fundamental Ratios, Cash, EBITDA, PAT

Sales and profit 7x and 10x approximately in last 9 years

ROCE and ROE >12 %

Debt to equity is okayish at ~1, Pledging is 0%

Promoter has good skin in game at ~55% shareholding and big players entered recently including Mukul Agarwal

Triggers

Macro Trends :

Amid rising demand for coal freight and an aggressive push towards diversifying its freight basket, IR is planning to buy 1,00,000 more Wagons over the next three financial years Under the National Rail Plan(NRP), Centre wants to significantly increase the national transporter’s freight numbers, along with its modal freight share to 45 per cent by 2030. As per GOI estimates, consolidated demand for freight will be over 6,300 Million Tons (MT) by 2026 and 8,220 MT by 2031 Having ferried 1,418 MT in this fiscal, the national transporter would need to account for over 3,600 MT in 2031 to meet its NRP targets.

Company has worked on

Backward integration, Capacity Expansion, High Value Products and Client Diversification

Technicals

Technical chart in 10th Aug24

Risks

Working capital intensive nature of operations

Operating Cash flows are not good. Working capital days, Cash conversion cycle, ROCE, ROE needs to improve

Strong dependency on big customer IR

Margins are fluctuating in past based on execution and delivery. Not easy to predict bad or good quarters for company business

Susceptibility of profitability to volatility in raw material prices – ORIL’s product mix mainly includes seats, berths, compreg boards wherein the major raw materials are wood, rexene, cloth, foams, recron and various other solvents. Major raw material is supplied inhouse like company manufactures rexene and foam useful in manufacturing of seats. Other raw material consumed for manufacturing of seats includes veneer, which is formed from timber and company procures timber from local market. Its profitability is susceptible to fluctuations in the prices of wood as it serves as the main raw material for manufacturing of veneers, particle boards, plywood and compreg boards. For wagons, bogies and coupler body, major raw material is steel or scrap of steel which is procured from local market whose prices are highly volatile in nature. However, the company has a price variation clause inbuilt for key raw material, i.e., steel and wheels if procured from Indian Railways, thus reducing the price volatility to that extant

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Jaykay Enterprises

Key Investment thesis –> Defense and aerospace sector venture in precision manufacturing with big customerssupported by designing, development, manufacturing, and testing of advanced composite engineering products made or composed of fibre glass, glass mat, plastic, resins etc.with applications in defence/aerospace/ logistics & electrical industries. Company also developing good capabilities in Additive manufacturing and software systems to support above venture

Jaykay Enterprises Limited (JKE), part of J K Organisation and part of the 139 years old diversified JK conglomerate. JKE initially engaged in the business of manufacturing nylon and acrylic fibers and later went into Registrar and Share Transfer Agent activities.

Presently, the Company has diversified itself into Additive Manufacturing systems,Proto typing, powder metallurgy, large scale Digital manufacturing, Reverse Engineering, Plant modelling, In the area of defense & Aerospace we focus on areas of engineering products across various industry verticals, software designing and development, manufacturing of parts and accessories used in defence and aerospace sector, our work includes composite applications, Under water mines ,machining for aerospace sector.

Product segments

The Company has consolidated its business focus into specific dedicated opportunities. a) Defence & Aerospace; b) Digital Manufacturing & Advanced Systems c) Software &Services d) Real Estate & Hospitality. The Company is operating business of manufacturing of precision turned components and all type of engineering goods for the defence, aerospace and other allied industries including Manufacturing,trade and deal in all kinds of products related to Defence and Aerospace and Additive manufacturing and Technical Consultancy Services, 3D Scanning,Reverse engineering ,Plant Modelling, design, develop and market software products for 3D and activities through its subsidiaries, Joint Venture, partnerships and associates.

Management Pedigree

Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited and scion of one of the best-known business families of India. He is the cofounder & has served as Managing Director of JK Technosoft Ltd (‘JKT’) and leads the company’s global operations together with the Board &Management Team. He has invaluable experience within JK Organization companies, handling various aspects of J K businesses, managing business units and operations as well as spearheading successful national and international expansion programs. He has rich experience in the manufacturing & IT services industry and multi-dimensional expertise in basic & core sector industries such as – textiles, synthetic fibres, cement and chemical processing, both in continuous as well as discrete manufacturing, Mr. Singhania has deep insights in Software Development Life Cycle (SDLC), Project Management, Strategic Planning, Business Development, Thought Leadership. Mr. Singhania spearhead in Carving new business opportunities and managing strategic investments in Defence & Aerospace, Digital Manufacturing (3D & Processing), Digital Transformation through acquisitions. He is an alumnus of IMD Business School.

SWOT

Fundamental Ratios, Cash, EBITDA, PAT

Sales and profit catching up in last 2 years

ROCE and ROE <10 %

Debt to equity is under control 0.35, Pledging is 0%

Promoter has good skin in game at ~56% shareholding and stake is increasing while Public stake is decreasing

Triggers

Macro Trends :

INDUSTRY OUTLOOK Defense & Aerospace Sector outlook is very positive owing to huge requirements from the domestic market. The A&D market in India is estimated to reach around US$ 70 bilion by 2030. With a focus on indigenization by GOI the sourcing from within the country will increase many fold resulting in great opportunities for companies in this sector. The additive manufacturing market in India is increasing slowly but surely. The GOI has already come up with a policy. The early entrants will have an advantage over others. The application of this technology globally has entrenched Defense & Aerospace, Health care and oil & Gas Sector. Digital manufacturing will lead the global manufacturing sector in a decades time

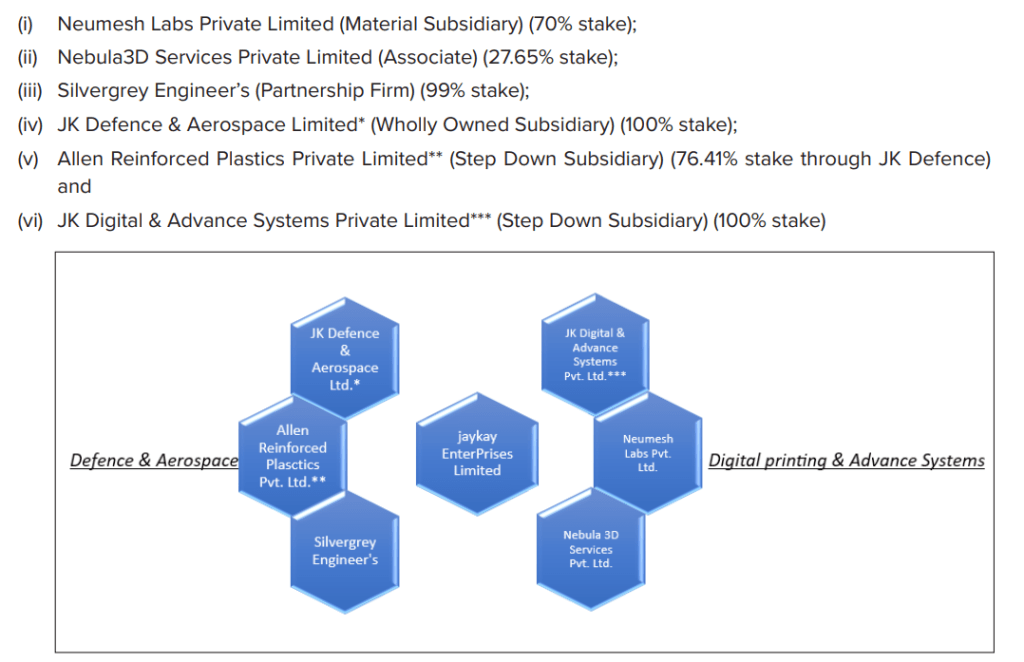

Joint Ventures And subsidiaries

JKE had entered into a strategic partnership with the global leaders in 3D Metal design and printing market. JKE had signed a Joint Venture and Shareholders Agreement with M/s Additive 3D Pte Ltd(A3D) an affiliate to M/s EOS Singapore Pte Ltd and consequent upon which a JointVenture (JV) company had been incorporated in the name of M/s Neumesh Labs Private Limited (‘Neumesh’) on 01st January, 2021, with shareholding of JKE and A3d respectively is 70% and 30% in said JV Company, inter alia, in the business of the 3D printing technology in India.

Neumesh Labs Private Limited

Neumesh Labs Private Limited (“Neumesh”) has established a Centre of Excellence (COE) in Bengaluru, the COE has state of the art EOS Software, Machines & Practices of cutting-edge 3D technology. Further Neumesh has developed a 3D printer JKPrint500, which was unveiled in IMTEX 23 Fair in Bengaluru. The product has received enthusiastic market response. Neumesh is also developing a lower price 3D printer which will be targeted at the mass market.

Neumesh, has also started its AM labs business. This is in line with various State Governments opening COE across engineering colleges and ITIs’. GOI in its 2023 budget announcement stated its intentions to establish COE’s across the country. Considering, huge numbers of COE’s that will be established, the demand for high quality polymer printers for training purposes will be high. Therefore, Jaykay Enterprises Limited along with its eco system partners have indigenously developed a polymer printer JK Print 300 and JKPM3 series, a Powder Management System which was unveiled in IMTEX 23 Fair in Bengaluru. The initial customer response has been encouraging. The JK Print 300 Printer is suitable for usage in prototyping, consumer goods, Automobile, and architecture for low volume production. The machine is ideal for usage in low volume production and training of students and technicians. The JK PM3 Powder Management System will optimize productivity and economics keeping in mind highest quality standards of parts produced by 3D metal printers. Neumesh, is working in tandem with the Governments Make in India program. Neumesh has started working on IAF prototyping projects and is looking closely at the MEA Oil & Gas market.

JK Defence & Aerospace Limited (“JK Defence”) and Allen Reinforced Plastics Private Limited (Allen)

JK Defence & Aerospace Limited (“JK Defence”) has acquired the 76.41% equity stake in Allen Reinforced Plastics Private Limited (Allen) which is engaged in the business of designing, development, manufacturing, and testing of advanced composite engineering products made or composed of fibre glass, glass mat, plastic, resins etc. applications in defence/aerospace/ logistics & electrical industries. Allen indigenously develops and supplies critical components to key defence projects in the country, such as BrahMos, Pinaka, SMILE, Akash missiles etc. to defence undertakings such as DRDO, ISRO, OFB, BHEL, BDL among others.

JK Defence stake in the step-down subsidiary i.e. Allen will increase from 76.41% to 92.92% after recent aquisition of shares through Rights issues

JK Defence & Aerospace Limited, Wholly Owned Subsidiary (“JKDAL”) of Jaykay Enterprises Limited, has been accorded an approval from the Office of the Commissioner for the Industrial Development and Director of Industries and Commerce, Government of Karnataka w.r.t. the investment proposal of JKDAL to establish a unit for manufacture of “Precision Turned Components and all types of Engineering Goods for the Defence, Aerospace and other Allied Industries including assembling in all kinds of products of Defence and Aerospace Equipments”. The approval includes allotment of 5 acres of land from KIADB at Devanahalli General Industrial Area (ITIR), Bangalore Rural District and necessary permission for water and power connections and associated NOC(s) from state industry authority. The unit will be eligible for incentives and concession as per applicable policy of the State.

Jaykay Enterprises Limited (“the Company”) has acquired 99% stake in Bangalore based partnership firm M/s. Silvergrey Engineers (SGE) inter-alia engaged in manufacturing and supply of parts and accessories to defence equipment manufacturing industry, catering to Customers including HAL, BEL, ISRO, Gas Turbine Research Establishment, Aeronautical Development Agency, Tata Advance Systems amongst others. SGE presently has manufacturing facilities located at Bengaluru

Representative image of 3D printers, digital manufacturing(not actual)

JK Digital & Advance Systems Private Limited

Incorporated on July 27, 2023, to provide digital and technical consultancy services, 3D scanning, and software engineering lab services. It aims to design, develop, and market software products for 3D applications and various industries.

Current Event

Company Share price has been adjusted for upcoming rights issue at 25Rs on 19th July24

Quarterly results have shown improvement –7th Aug24

12 acre Land parcel applied in lucknow

Details of recent triggers

Neumesh Labs Private Limited (Material Subsidiary) signs Memorandum of Understanding (“MoU”) with Agnikul Cosmos Private Limited Neumesh Labs Private Limited, material subsidiary of the company entered into a MoU with Agnikul Cosmos Private Limited, a Chennai headquartered Space-tech start-up Company on August 9, 2023. The MoU includes supply and maintenance of Metal Printer, Part Printing and Supply of Metal Powder. • Joint Venture with Phillips Machine Tools India Private Limited The Company had entered into a Joint Venture with Phillips Machine Tools India Private Limited, a subsidiary of Phillips Corporation, USA, to form and constitute a Limited Liability Partnership (LLP) under the name and style of JK Phillips LLP pursuant to the Limited Liability Partnership Agreement dated December 20, 2023. The LLP has been formed on December 28, 2023 to carry out the business of trading and distribution of Advance systems which includes CNC machines, lathes, hydraulic press, 3D printers, moulding machines and accessories originally produced by Phillips and other manufacturing/ trading activities including after-sales services. • Tripartite Agreement to manufacture Medical Implants executed between JK Digital & Advanced Systems Private Limited, EOS Electro Optical Systems India Private Limited and Meril Innovations Private Limited During the year, JK Digital & Advanced Systems Private Limited a WoS of the Company had completed the execution of a Tripartite Manufacturing Agreement on January 19, 2024 with Meril Innovations Private Limited, Gujarat (Meril Life Sciences), a leading MedTech Solutions Company, for production of Medical Devices/Implants through 3D Printing along with its technology Partner EOS, Chennai a WoS of EOS GmBH of Germany. The Agreement provides for JK Digital to Install, operate specified 3D Printers assisted by EOS, for manufacturing of Orthopedic Implants at Meril Life Sciences premises in Gujarat. • Merger of Business of Silvergrey Engineers into the Company In line with the approval of Board of Directors of the Company accorded on May 29, 2023 the Company had executed Dissolution cum Retirement Deed with Ujala Merchants and Traders Limited (UMTL) dated February 3, 2024, where in UMTL agreed to retire from the from the partnership of Silvergrey Engineers w.e.f. January 31, 2024, resulting the Company acquired the balance 1% stake in Silvergrey Engineers, pursuant to which the Company, will carry on the business of manufacturing of precision turned components and all type of engineering goods for the defence, aerospace and other allied industries as a division/segment of the Company. • Approval of Land Parcel to JK Defence & Aerospace Limited (WoS) in Bangalore Rural District JK Defence & Aerospace Limited WoS of the Company, had been accorded an approval from the Office of the Commissioner for the Industrial Development and Director of Industries and Commerce, Government of Karnataka on March 13, 2024 w.r.t. the investment proposal to establish a unit for manufacture of “Precision Turned Components and all types of Engineering Goods for the Defence, Aerospace and other Allied Industries including assembling in all kinds of products of Defence and Aerospace Equipments’’

The approval includes allotment of 5 acres of land from KIADB at Devanahalli General Industrial Area (ITIR), Bangalore Rural District and necessary permission for water and power connections and associated NOC(s) from state industry authority. The unit will be eligible for incentives and concession as per applicable policy of the State

Opportunity Size

Recently India has made 3D printed Semi cryogenic engine

Additive manufacturing expected to grow at more than 20% CAGR and coupled with defense and aerospace sector growth, oppportunity seems big enough

Technicals

Technical chart in 27 Jul24 (after Rights issue adjustment)

Technicals on 6-Jul-24 –ALD presentation

Technicals on 18-Jun-24

Risks

Operating Cash flows are not good. Working capital days, Cash conversion cycle, ROCE, ROE not upto the mark –outcome is high valuation which is typical characteristics for a turnaround company–Things look really bad before they turn decent, and then good and then turn very good.

Chances of turning very good?? We need to see –1 out of 100 companies turnaround succuessfully—rest of the companies bites the dust

Other income is high and skewing PAT

New business division of defense dont take off as anticipated

Dependency on limited customers for new contracts and

Competition from domestic and foreign players

There are related party loans to subsidiaries which may be susceptible to waivers

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Zaggle Prepaid Ocean Services

Key Investment thesis –> Differentiated SaaS-based fintech platform with Strong network effect offering Comprehensive suite of products for a large & growing addressable market. Company has amazing cross selling and Up-selling opportunities across domains.

Zaggle builds financial solutions and products to manage the business expenses of corporates, SMEs, & Startups through automated and innovative workflows. Headquartered at Hyderabad, it is at an intersection of of SaaS (Software as a service) and Fintech. With 273+ employees, the company has 50 Mn+ co-branded prepaid cards.

Products Zaggle Zoyer: accounts management services Zaggle Save: Help employees save tax with Save’s flexible employee benefit plans Zaggle Propel: all-in-one solution for employee rewards, and channel partner incentives.

Stats in accounts/users and Revenue streams

Share in Prepaid Cards market –16%+, Transaction volume wise ~13%

Strength of company

#1 issuer of prepaid cards

Multilingual interface

In-house developed technology with strong network effect

Customizable products

Diversified customer relationships across sectors along with preferred banking and merchant partnerships

Low churn rate of customer (<2%), long term relationships

Seasoned management team and board

Awards

Company has received an award for “Best Spend Management System“ and “Best Cards Initiative for Zaggle ZatiX“ at 11th Edition Payments Industry Awards by KamiKaze B2B.

Company has received an award for “FinTech Brand of the Year“ at 4th Edition Festival of FinTech Conclave Awards 2024 in association with BW Businessworld.

Company has received an award for “Pride of Telangana “ Achiever” Start up Category 2024” by Round Table India and Ratnadeep.

Company has received an award for “Excellence in Innovation Business Spend Management Software India 2023” in the Global Banking and Finance Review Awards 2023.

Fundamental Ratios, Cash, EBITDA, PAT

Amazing Sales and Profit growth of 11x in 5 Years

ROCE and ROE close to 15%

Debt to equity is under control and close to Nil

Pledging is 0%, Promoter has good skin in game at ~44% shareholding

Though FII, DII decreased stake in last 2 qtrs but still stake held by FII, DII + HNI is big, Public holding only ~20% stake . Big Shark Ashish Kacholia has increased stake over few quarters towards 4%+ shareholding

Triggers

Macro Trends :

Moving towards Digital payments ; Increasing scope of Prepaid cards ; New companies coming up

PREPAID CARDS Growth till 2027 expected to be in range of 30-40% CAGR

Management Guidance and commentary

We doubled our revenue over the last 3 years and are poised to double our revenue over the next 2 years through organic growth. Our expectation of revenue growth for this fiscal year is to the tune of 45%-55%. We are focused on garnering more market share and making significant investments in technology, specifically building deeper AI capabilities to cater to the massive demand for Spend management solutions. We intend to pursue inorganic growth opportunities through mergers and acquisitions. Additionally, we plan to expand geographically into the US markets as part of our growth strategy.

New Vertical

In Q1FY24, Zaggle introduced corporate credit cards and vendor management platform – Zoyer.

Launch of credit cards as a product in FY24 . The monthly volume of transactions for credit cards exceeded the monthly volume of transactions for prepaid card

Zaggle Zatix – our analytics platform launched this FY & offered by Banks as bundled solution of Corporate Credit Cards + SaaS.

New contracts in Last 1 year

In Q1FY24, company entered into contract with BOB Financial Solutions Limited for implementing commercial card Onboarding & value-added services platform and launch of the Zaggle Yes Bank Corporate Credit Card, powered by Zaggle Zatix – a spend analytics platform that allows corporates to streamline business and employee expenses, budget better and negotiate favorable supplier terms.

Zaggle Save (Expense Management platform & Employee benefits)

Employees of Hero Motocorp Limited.

Lifestyle International Private Limited

Quess corp limited

Bennett, Coleman & Co. Ltd.

ARCADIS CONSULTING INDIA PRIVATE LIMITED

Wipro Limited

Benetton India Pvt. Ltd.

Emcure Pharmaceuticals Limited

Europ Assistance India Pvt. Ltd.

Axis bank limited

Expleo Solutions Limited

Yokohama India Private Limited

Eversub India Private Limited (Subway)

Contract with Torrent gas for 2 years , approx 200cr business for Implementing Close Loop Fleet Program

Agreements with ecosystemplayers in varied domains like Domestic card, corporate cards, forex cards, Travel, Cross border payments

Agreement with VISA -In Oct,23, company has entered into a growth agreement with VISA. This alliance is in support of the issuance of Forex CoBrand Cards. Visa will pay the launch bonus for supporting the launch of Forex Cobrand Cards. and will also pay incentives on Forex transactions basis spend commitments. Zaggle can leverage existing Corporate base to sell forex cards to employees of the Corporate client, and it can be tightly coupled with Zaggle expense management solution. The deal size is ~$20 Mn for next 5 years.

Company has entered into an agreement with Skydo Technologies Private Limited. This is to enable facilatate cross border payments for Zaggle corporate customers

Zaggle is contracted to provide services to Bank whereby Zaggle’s accounts payable software & expense management software and the Axis bank Corporate Credit Cards are bundled and jointly offered to Zaggle corporate customers to drive card spends & greater usage of the software

Zaggle & EaseMyTrip will leverage its Existing Corporate base to sell Integrated Travel & Expense Management Solutions to Corporate Clients.

Zaggle & Riya Travel will leverage its Existing & New Corporate base to sell Integrated Travel & Expense Management Solutions to Corporate Clients.

Zaggle is contracted to be a Co-brand partner with Nishi Forex who is an Authorised Dealer II for forex card to carry out activities such as Sales and Distribution, Marketing and Campaigning bundled with Zaggle expense management to drive card spends & greater usage of the software. Subject to RBI approval the product launch will be done in due course.

Strategic alliances and partnerships with PSU

Opportunity Size

Zaggle Propel itself Can hit potentially 3000cr in revenue with overall revenue may hit 5000cr by 2030. Net profit margin may remain between 4-7%. Company may see profits of 250-350cr if opportunity size is grabbed. With an Eps of 19-25 and PE of 40-60 –Future Price Range oscillates between estimated 750-1500. Getting such a business at 100-150 Rs price point could be super deal (dont know if we get that price)

Peer analysis

Technicals on 6-Jul-24

Risks

Operating Cash flows are not good. That needs to be monitored closely

Working capital days, Cash conversion cycle is also expanding

Business is heavily titlted towards H2 of FY

Other income will go down once cash from IPO is Utilised

Lot of investment is being done in Zoyer for product enhancement and building of Zatix, an analytics platform. If products fails to takeoff, then a good amount will be written off from assets

Increased Regulatory Compliance poses many risks for Fintech companies

High valuations in short term is another risk though runway seems long for company growth

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Allied Digital Services (ADSL)

Key Investment thesis –> Smart city contracts and infrastructure solutions

ADSL global IT Consulting and Services provider and Systems integrator offering infrastructure solutions and services to clients across 70 countries. It designs, develops, and deploys digital solutions and delivers end-to-end IT infrastructure services including, End user IT Support, IT asset life cycle, enterprise applications and integrated solutions

CMMi Level 3, SOC2 certified, ISO 9001, 27001 & 20000 – Highest standard for IT Service Management Tools

Customers, Global Presence and RevenueMix

Increasing clients. Deals from big clients

Fundamental Ratios, Cash, EBITDA, PAT

Stable Ebitda, Pat margins. Debt to Equity under control. ROCE is on uptrend in medium term

Working capital days and cash conversion cycle have been improving

ADSL when i first published the report

ADSL NOW

Triggers

Securing new projects of Smart city

Securing of prestigious contracts, exemplified by projects like the Ayodhya Smart City and Taloja Smart City.

In February 2024, ADSL received a Letter of Intent for the Taloja Smart Industrial City Solution contract in Navi Mumbai. This groundbreaking initiative will unfold over an 18- month implementation phase, followed by a 60-month Operations and Maintenance period. The project’s scope involves establishing an Integrated Command & Control Centre (ICCC) at both the Corporation’s Head office and the Industrial Township. The ICCC software will seamlessly integrate with a Cloud-based Data Center/Disaster Recovery system. Furthermore, the project encompasses the deployment of a cutting edge CCTV-based Surveillance System to bolster security and monitoring capabilities. In January 2024, was selected as a Master System Integrator (MSI) for the Integration of CCTV Surveillance with Existing ITMS Control Room for the Ayodhya Smart City Project. This project entails the establishment of a multi-location CCTV surveillance system. The capital expenditure (CAPEX) and implementation phase is anticipated to last three months, followed by a five-year operational and maintenance (O&M) phase.

Completed 12 smart city projects with 2 new wins.

Expecting an opportunity size of Rs. 50,000 crore in the smart city projects in the next 5 years.

Seeing traction in the smart city space with upcoming tenders.

Future Outlook,Targeting Acquisitions and exploring fields like

Eyeing opportunities in Cybersecurity and Cloud arena for potential acquisitions.

Focused on improving margins in O&M contracts and government projects.

Expecting better traction in IT business with growing interest in European and APAC markets.

Revenue Plan

Plans to reach INR1,000 crores in revenue over the next 2-3 years with a focus on improving margins

Order book outstanding at Rs. 1,600 crore, with execution period of around three years (Nov23)

Digital Desk (formerly ADiTaaS):

Rebranded to ‘Digital Desk’ with enhanced features in AI, conversational AI, and generative AI.

Seeing traction with 100+ customers globally.

Leadership Augmentation

Allied Digital has added Mr. Ramanan Ramanathan as “Global Head Strategy – Growth, Innovation, Partnerships” to its Senior Leadership Team. Mr. Ramanathan, a seasoned strategist and growth consultant, has advised global entities and served as the Mission Director of the Atal Innovation Mission, where he established over 10,000 Tinkering Labs and 75 incubators.

In his new role, he will assist the company in its expansion by identifying new market opportunities, fostering innovation, and establishing strategic partnerships. Additionally, he will identify and evaluate potential partners to enhance business capabilities and achieve strategic objectives.

With a distinguished career at TCS and CMC Limited, he continues to shape innovation, entrepreneurship, and sustainable development across various sectors.

8th October 24

Allied Digital awarded Pune Safe City (FY 2024) Project for Total Contract Value of Rs. 430+ Crore

Key project highlights include: Comprehensive surveillance: Track 1 of the project shall cover O&M of the existing cameras for a period of 6 years and Track 2 shall cover Implementation of new infrastructure over 12 months followed by 5 years of O&M.

Advanced technology: The project will feature advanced Artificial Intelligence-enabled video analytics, an Automatic Number Plate Recognition (ANPR) system, Vehicle Over speed Detection System (VDS) a Facial Recognition System (FRS), Drones, and Mobile surveillance vans to ensure robust security and monitoring.

Upgraded infrastructure: The Command-and-Control Center at the Commissioner of Police office and supporting Data Center will be upgraded with implementation of additional capacity and installation of advanced software leading to improved efficiency and 24×7 real time monitoring. Additional viewing facilities will be established at various police stations and key government offices