ENGINE

BE FINANCIALLY INDEPENDENT

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Key Investment thesis –> Increasing Demand of Water Intake Systems, Water and Waste Water Pumping Stations and Treatment Plants, Storm Water Pumping Stations, Water Transmission Lines, Consistent Business and Order book

Read Pick1, Pick2, Pick3, Pick4, Pick5, Pick6, Pick7, Pick8, Pick9, Pick10, Pick11, Pick12, Pick13, Pick14, Pick15, Pick16, Pick17, Pick18, Pick19, Pick20, Pick21, Pick22, Pick23

Jash engineering is dedicated to offering varied products for use in Water and Wastewater Pumping Stations and Treatment Plants, Storm Water Pumping Stations, Water Transmission Lines, Desalination, Power, Steel, Cement, Paper & Pulp, Petrochemicals, Chemicals, Fertilizers and other process plants.

Headquartered in Indore – India, Jash has six well-integrated state-of-art manufacturing facilities, four in India and one each in the USA & UK. Global presence with bases in India / USA / Austria / Hong Kong / UK

Employees > 1075, Countries served 45+, Manufacturing units 6, Capacity utilization 70% approx

Company has many accolades, and technical collaborations

Joint Venture with Invent , Germany to manufacture their range of aeration and mixing equipment.

Technical & Financial collaboration with Schuette, Germany for Bulk solids valves

Technical Collaboration with Invent, Germany for Disc Filter

Technical collaboration with Rehart, Germany for Archimedes screw pumps & hydro power generation.

Technical collaboration with Weco Armaturen, Germany to offer its range of Valves in Asian market

Domestic 40%, Exports 60%

Water control gates –60% (FY24) 49%(Q1Fy25)

Valves -15% FY24, 13% Q1FY25

Screening equipment 15% FY24, 31% Q1FY25

Hydropower and pumping solutions 10% FY24, 7% Q1FY25

Strengths :

Fundamental Ratios, Cash, EBITDA, PAT

ROCE>25% and ROE> 22%, DE ~0.23 , Free cash flow is good , Pledge is Nil

Net Profit went 67X+ in 10 Years, Consistent Dividend Payout

Consistent Profit growth, sales growth, ROE over 3 years, 5 years, 10 Years

Expanding presence and Acquisitions

Acquired Waterfront Fluid Controls Ltd, UK in 2023.

WATERFRONT UK PLANT & OFFICE INAUGURATION

After successful acquisition of Waterfront Fluid Controls Ltd, UK, the company has taken manufacturing plant on lease which is adjoining shed to the present Waterfront’s shed. This plant was commissioned on 31st May 2024.

A new plant for manufacturing process equipment is under construction in Chennai. This plant will be commissioned in December 2024/Feb25. This facility is being built at an approximate cost of Rs. 20 crores and this will start contributing to improvement in revenue from April 2025 onwards. This facility at its peak production capacity will contribute up-to Rs. 100 Cr to company revenue.

A new land has been acquired for expansion of Unit 4 (Fabricated Products Plant), SEZ Unit. This new plant of ~ 55000 sq. ft. will be commissioned in FY 2025-26. Manufacture Stainless steel products for the growing export market. The construction of this plant will start in October 2024 and the plant will be commissioned by year end 2025. This plant will be constructed at a tentative cost of Rs 22-23 crores inclusive of land and at its peak production capacity will contribute up-to Rs. 100 Cr to company revenue.

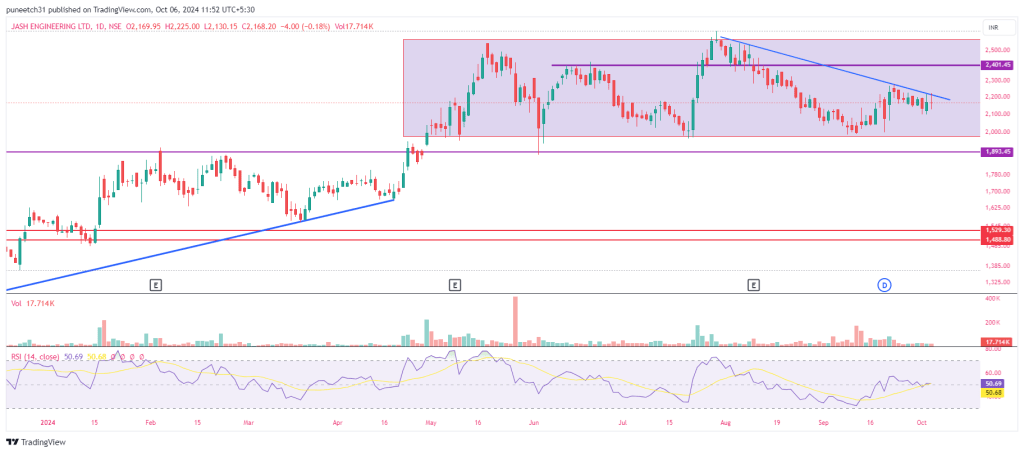

Good execution and order book and Consistent new orders

946 cr order book on 1st sep24, 74cr orders in pipeline, negotiation

FY25 guidance ~675cr

New Product developments

First Vortex Grit Mechanism with Grit Classifier For 26 MLD STP Jhansi, UP Jal Nigam

Combined Screening & Grit Removal System-1MLD (PTU) for Enviro-Infra, Bareilly, UP

First set of Bladder Vessel 9 m3 x 3, 1 m3 x 3 supplied to Varanasi WSP Project

3 Wheel Sealed Version Disc Filter for 6 MLD capacity for Delhi Jal Board

| Large working capital requirement, cash conversion cycle is bit high Trade receivables and Inventory on higher side Rising raw material and commodity costs Increase in competitive bids for procuring the projects |

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

Key Investment thesis –> Increasing Demand of Gas pipeline Infra, City Gas distribution and National Gas policy 2030, Expanding Geographically, Consistent Business and Order book

Read Pick1, Pick2, Pick3, Pick4, Pick5, Pick6, Pick7, Pick8, Pick9, Pick10, Pick11, Pick12, Pick13, Pick14, Pick15, Pick16, Pick17, Pick18, Pick19, Pick20, Pick21, Pick22

LIL was incorporated in 1998 and is engaged in the business of pipeline laying providing comprehensive erection, testing, and commissioning of Oil and Gas pipelines, city gas distribution projects, tankage and operations and maintenance services. It is based in Hyderabad, Telangana.

Company has two (02) Joint Ventures viz., CPM-Likhitha Consortium, India and Likhitha Hak Arabia Contracting Company, Kingdom of Saudi Arabia. In addition, Company held 60% equity share capital in Likhitha Hak Arabia Contracting Company, and consequently, now it became a subsidiary of the Company

Has successfully laid over 1500 km of steel pipelines and over 1500 km of MDPE of oil & gas pipelines in the past years. Additionally, the company is laying approximately 1000 km of oil & gas pipelines for the ongoing projects

Executed the First Trans-National cross-country pipeline of South-East Asia connecting India to Nepal in the year 2019, for the supply of petroleum products

Strong presence in more than 20 states and 2 Union Territories in India.

Business Segments:

a) City Gas Distribution Projects:

This Involves laying of steel and MDPE pipelines for consumers across domestic, commercial and industrial sector, creating a network of pipelines along with associated facilities, Last Mile Connections, CNG Stations

b) Cross Country Pipeline Projects:

Laying of Cross Country Pipeline projects along with piping, civil, electrical, instrumentation and other associated works

c) Operation & Maintenance Services:

O&M services include providing skilled manpower, executing emergency repairs, overhauling, scheduled maintenance activities and operation of the network

d) Tankage:

Construction of fuel depots including storage tanks, Combined Station Works, mechanical, instrumentation, electrical, civil works, F&G system, and other associated facilities

Strengths :

Clientele

GAIL, GGL, ONGC, HPCL, IOCL, IHB, Numaligarh Refinery, IOAGPL, TGPL, IGL, etc.

ROCE>30% and ROE> 20%, DE ~Nil , Free cash flow is good , Pledge is Nil

Stable OPM, Net Profit went 33X+ in 10 Years, Consistent Dividend Payout

Consistent Profit growth, sales growth, ROE over 3 years, 5 years, 10 Years

Promoter has sufficient skin in game at 70% shareholding

Triggers

Macro Trends :

India has set a target of increasing the share of natural gas in the overall energy mix to 15% from present 6.7%.

As per the Government policies, PNGRB has increased the number of Geographical Areas (GAs) to 228 comprising of 402 districts spread over 27 States and Union Territories, covering 70% of Indian population and 53% of its area. These recent Government initiatives have provided lucrative opportunities for Oil & Gas infrastructure service providers

Recent policy moves, including a wide-scale rollout of CNG and the expansion of gas infrastructure including LNG terminals, long-distance transmission pipelines and city gas distribution networks, will help drive 30bnm³ of gas demand growth over the next decade through fuel switching away from coal and oil. A recent switch to CNG from coal in India’s brick industry is encouraging greater gas use.

India is set to dominate the number of trunk/ transmission pipeline projects that are expected to start operations in Asia during 2024-2028, contributing about 43% (62 projects) of the region’s total projects count by 2028. The transmission pipeline length of 29,800 kms is expected to be added, says GlobalData, a leading data and analytics company.

The gas pipeline infrastructure has been seeing intense development activity. The Government of India has set a target to reach 34,500 km by 2024-25 end from 22, 335 km as on January, 2023.

Furthermore, plans to connect states with the trunk natural gas pipeline network by 2027 are gathering

momentum.

In terms of investments, the Petroleum and Natural Gas Ministry said about ` 41,000 crore ($4.95 billion) are expected from companies to build natural gas pipeline infrastructure in the northeastern states and northern federal territories of Kashmir and Ladakh.

The thrust on natural gas and government policy initiatives are in line with India’s global commitments to boost the use of cleaner fuels and cut carbon emissions with the ultimate goal of achieving net zero carbon emissions by 2070.

Expanding presence

In line with growth strategy, Company has entered new markets such as the Kingdom of Saudi Arabia and the United Arab Emirates, where we see substantial opportunities in the oil and gas infrastructure sector. The company has been exploring growth opportunities beyond India. We have formed a joint venture firm in Saudi Arabia and have opened a branch office in Abu Dhabi, UAE to explore business prospects in the Middle East markets which promise long-term growth for pipeline infrastructure development.

The Indian government’s continued emphasis on expanding the oil and gas transportation network and promoting city gas distribution projects provides us with a steady stream of contracts.

India’s energy consumption is on the rise, with the country consuming 19.9 million metric tonnes of petroleum products and 5.51 BCM of natural gas during FY 2023-24. As the world’s third-largest consumer of energy, India’s demand for natural gas is expected to grow fivefold by 2047, in line with the nation’s vision of becoming a developed nation by its centennial year

Good execution and order book and Consistent new orders

| Large working capital requirement, cash conversion cycle is bit high Trade receivables and Inventory on higher side Any change in CGD policy Rising raw material and commodity costs The Company is deriving significant portion of orders from major Oil & Gas distribution companies inducing a client concentration risk Increase in competitive bids for procuring the projects |

Disclaimer – Analysis is NOT a BUY/SELL/HOLD Recommendation. It can be used for educational purposes. There can be lot of things which have been missed in analysis either due to lack of information or oversight etc.. Do your own diligence & contact your expert financial adviser before making any investment decision.

In case you have any questions/ queries, please feel free to reach me through Contact Form

Do spread the word among your peers, family members or anyone who can benefit from this blog and asked them to subscribe. But be selfish and take care of yourself first by subscribing before they do.

Enjoy the day and your life. Don’t forget, we are alone in this grand universe and may not get a chance to live again.